Key Takeaways:

- 31% of small-business owners have applied for a loan within the past 2 years.

- Over 1 in 10 small-business owners who applied for a business loan in the past 2 years have been denied.

- Nearly 1 in 20 small-business owners have been scammed by a fraudulent lender.

- 3 in 5 small-business owners support the use of AI in the business lending process.

Who Is Applying for Business Loans?

Our study examined small business lending trends across various industries, including fintech, healthcare, and real estate. We also looked at upcoming loan application intentions among small business owners, including the influence of alternative lenders, commercial banks, and nonbank financial institutions.

There's been a lot of demand for small business loans: 57% of small-business owners have applied for one in the past, with 31% having done so within the past two years. Of those who applied in the last six months, most were working in manufacturing, health care, and construction sectors. These sectors often require access to lines of credit, especially to cover operating expenses and balance sheets.

Nearly 2 in 5 small-business owners told us they plan to apply for a business loan within the next two years. Those in manufacturing, retail, and construction were the most likely to plan to do so within the next six months. This reflects market trends showing an increasing need for cash flow management in these industries.

Why Are Small-Business Owners Applying for Loans?

Let's explore what drives small-business owners to seek financing from lending institutions and lenders.

Most borrowers indicated they needed loans to increase inventory, boost marketing efforts, and purchase new machinery. These motivations highlight how market size and industry-specific needs shape the lending landscape. For example:

- Construction companies may seek loans primarily to purchase new machinery for their operations.

- Health care sector businesses typically apply for financing to open additional locations.

- Informationtechnology firms commonly pursue loans to support their marketing campaigns.

- Manufacturing businesses often request financing to invest in new machinery.

- Professional services companies frequently seek loans to fund marketing initiatives.

- Retail establishments often apply for financing mainly to expand their inventory.

These motivations highlight how lending market dynamics are shaped by the priorities of small business owners, with an eye toward growth and innovation.

What Loans Are Small Business Owners Applying For?

Now, we'll look into common business lending sources and their appeal to different industries.

Small-business owners have been exploring alternative lending options and traditional banking. Traditional banks, credit unions, and even online lenders have all been part of the evolving lending process.

Based on the number of small-business loan applications, credit unions, and community development financial institutions have been the fastest-growing providers. Many small banks focus on underwriting loans that cater specifically to their communities, offering new opportunities for local entrepreneurs.

However, small banks may face challenges due to economic pressures stemming from events such as the pandemic. The Federal Reserve and FDIC continue to monitor the financial health of these institutions and their impact on small business credit availability.

Different industries showed clear preferences for specific lending resources, though. Here's a breakdown of which industries were most likely to apply for a loan using each of the following methods:

| Loan Application Provider | Industry Most Frequently Applying |

|---|---|

| Traditional bank | Professional services |

| Online lender | Construction |

| Credit union | Health care |

| Peer-to-peer lending platforms | Retail |

| Microloan providers | Manufacturing |

| Merchant cash advance providers | Construction |

| Community development funding | Construction |

| Invoice financing | Construction |

Small construction companies often need loans for working capital, equipment purchases, and project startup costs. It can be especially hard for them to secure financing due to irregular cash flow from long billing cycles and the need for expensive machinery. Meanwhile, the seasonal nature of construction work in many areas can mean income fluctuations that can make lenders hesitant (inconsistent cash flows and seasonal income fluctuations can impact loan repayment).

Despite the variety of options, 12% of small-business owners who applied for a loan in the past two years were denied. Community development funding, peer-to-peer lending platforms, and traditional banks were the loan providers most likely to have turned down these applicants.

What Do Small-Business Owners Look for in a Loan?

The following factors had the biggest influence on small-business owners' loan decisions and how they evaluate lenders.

When considering loans, borrowers prioritized low interest rates, favorable term loans, and repayment flexibility above all other factors. These are important to consider since they directly impact how much a loan will cost and how long it will take to pay off.

The Federal Reserve's policies, along with year-over-year economic trends, play a significant role in shaping these expectations.

Small-business owners have relied on various information sources to assess loans and lenders:

- Online reviews (69%)

- Comparison websites (48%)

- Friend recommendations (37%)

- Online forums (33%)

- Family recommendations (32%)

- Colleague recommendations (29%)

- Government resources (20%)

- Industry associations (18%)

- Social media (12%)

- Loan brokers (11%)

Reddit has become a popular place to look for honest product reviews on all sorts of things, so why not loans? You might find some buzz about business financing in the popular r/smallbusiness subreddit, for instance.

What Is the Loan Application Experience Like?

Next, we'll examine the hurdles small-business owners have faced in the loan process. We've also uncovered some common fraudulent lending practices targeting small-business owners.

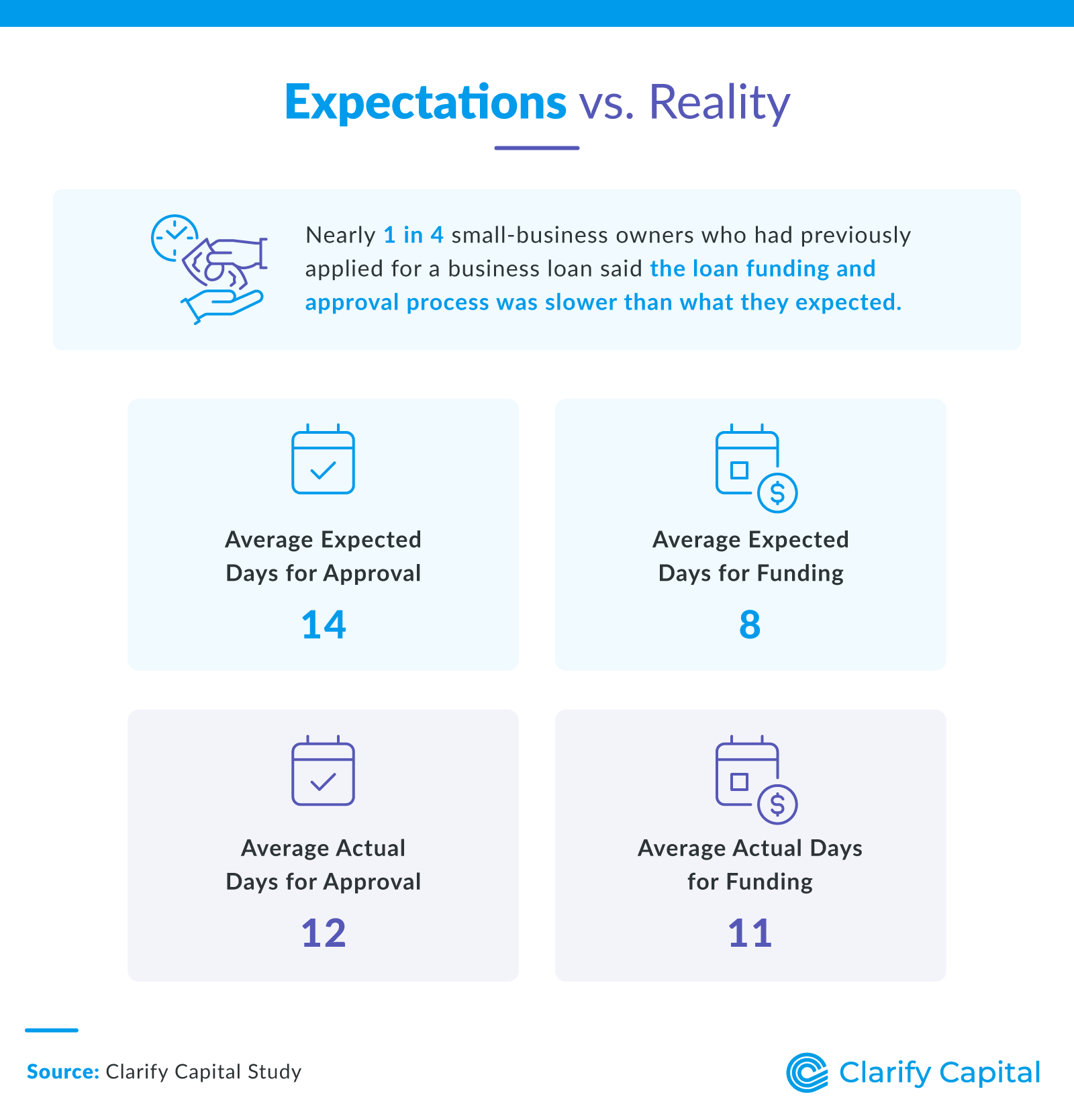

On average, loan approval happened two days faster than small businesses expected. But receiving the funding took longer than anticipated — 11 days on average, compared to the expected eight days. Timing can be a challenge in the loan approval process. Let's see what else has caused issues for small businesses.

High interest rates topped the list of small-business challenges in getting loans. The interest rate is a major loan factor, as it determines a loan's affordability and feasibility for many applicants. Complex paperwork was another major hurdle, and strict eligibility criteria rounded out the top three challenges. Business lending could definitely have been more user-friendly for our study participants.

Another challenge can be identifying business loan scammers. Watch out: Fraudulent lenders are on the rise, and they have scammed nearly 1 in 20 of the small-business owners who took our small-business lending survey.

The top red flag our respondents shared with us that often indicates a scam was high-pressure tactics, followed by demands for upfront fees. Always thoroughly vet your lenders and be wary of predatory lending offers that seem too good to be true.

How Could the Business Loan Experience Be Improved?

Artificial intelligence (AI) can streamline many aspects of the business lending process, and we found out just how small-business owners feel about it. We also got their overall suggestions for improving the lending process.

AI can streamline some financial services by crunching numbers, handling routine tasks, and sharpening lending decisions. Most small-business owners are fine with it when it comes to lending: 3 in 5 of the ones we surveyed said they're open to the concept of using AI in the business lending process. Specifically, they said they'd trust AI to handle fraud detection, credit scoring, and document verification.

Comfort levels with using AI in lending varied across industries, though, with manufacturing professionals being most likely to say it's ok. Here's the full breakdown:

- Manufacturing (83%)

- Information technology (73%)

- Health care (72%)

- Construction (61%)

- Retail (57%)

- Professional services (53%)

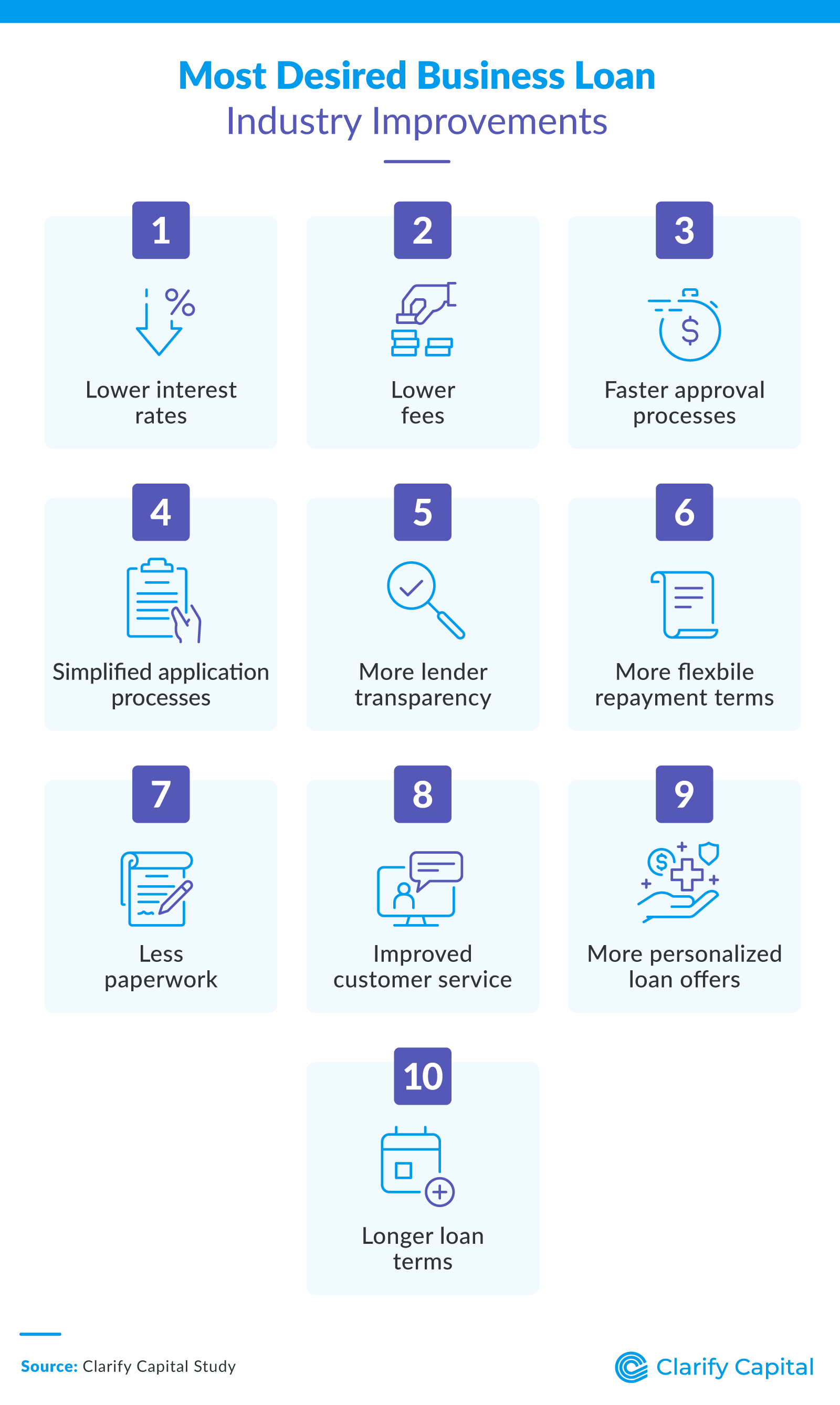

Lower interest rates topped the list of desired improvements across all industries, followed by lower fees and faster loan approval processes (who wouldn't want a fast business loan if they had the option?). The top improvements varied by industry. The most common suggestions (except for the most popular option, lower interest rates) are listed below:

| Industry | Most Desired Loan Industry Improvement |

|---|---|

| Construction | Simplified application process |

| Health care | Lower fees |

| Information technology | Simplified application process |

| Manufacturing | Faster approval processes |

| Professional services | Lower fees |

| Retail | More flexible repayment terms |

Securing Funding for Your Business

There's been a strong demand for business loans across industries, with many entrepreneurs seeking larger amounts than they're approved for. While high interest rates and complex paperwork have been a common barrier, technological solutions like using AI in the lending process may help to speed things up in a way that makes borrowers happy.

Alternative lending sources like credit unions and peer-to-peer platforms are also gaining popularity, offering new options for small-business financing to give businesses a better chance at getting the loans they need. Small-business owners' suggestions to improve the lending industry offer valuable insight for savvy lenders. Take it from us — a simple application process is the best way to start off a lending relationship on the right foot.

Methodology

We surveyed 517 small-business owners about their experiences securing loans for their businesses. Among them, 17% worked in retail, 15% worked in professional services, 10% worked in information, 6% worked in manufacturing, 6% worked in health care, 5% worked in construction, and the remaining 41% worked in other various industries.

About Clarify Capital

Clarify Capital specializes in fast, flexible financing to help small businesses thrive. With no-doc business loans and fast business loans up to $5 million, we provide entrepreneurs with financial solutions to help them grow from business owners to industry leaders.

Fair Use Statement

You may use this data for noncommercial purposes, but please include a link back to our original research.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts