If you've taken out a business loan (or you're thinking about it), you're probably wondering how it affects your taxes. Here's the short answer: the loan itself isn't taxable income, and principal repayments aren't deductible. But the interest you pay on that loan? That's typically a deductible business expense that can lower your tax bill.

I've spent over 15 years helping business owners sort through exactly this question. The tax implications of a business loan depend on the type of loan, how you use the funds, and whether you meet specific IRS requirements. The rules aren't complicated once you know what to look for, but getting them wrong could mean overpaying at tax filing time.

Below, I'll cover which business loan expenses are tax-deductible, how deductions work across different loan types, IRS rules that affect your interest deduction, and practical steps to claim what you're owed. Whether you're a sole proprietor with your first small business loan or managing multiple financing products, you'll find what you need to make smarter decisions about your business tax strategy.

Are Business Loans Considered Taxable Income?

When a lender deposits loan proceeds into your bank account, that money isn't taxable income. The IRS doesn't treat borrowed funds as earnings because you're obligated to pay them back. Your loan amount is a liability on your balance sheet, not revenue.

That distinction separates business loans from other forms of financing. Grants, prizes, and forgiven debt may count as taxable income. But standard loan proceeds from a term loan, line of credit, SBA loan, or merchant cash advance don't increase your income tax obligation.

When Financing Becomes Taxable

There's one important exception: loan forgiveness. If a lender cancels or forgives your debt, the IRS generally treats the forgiven amount as business income. The Paycheck Protection Program was a notable exception during the pandemic, but most forgiven business debt is taxable.

The takeaway is straightforward. As long as you're making loan payments on schedule, the principal you borrowed doesn't affect your tax bill. Your deductions come from the interest, fees, and other costs tied to the loan.

What Business Loan Expenses Are Tax Deductible?

Not every dollar you spend on a business loan reduces your taxable income. Here's what the IRS lets you write off.

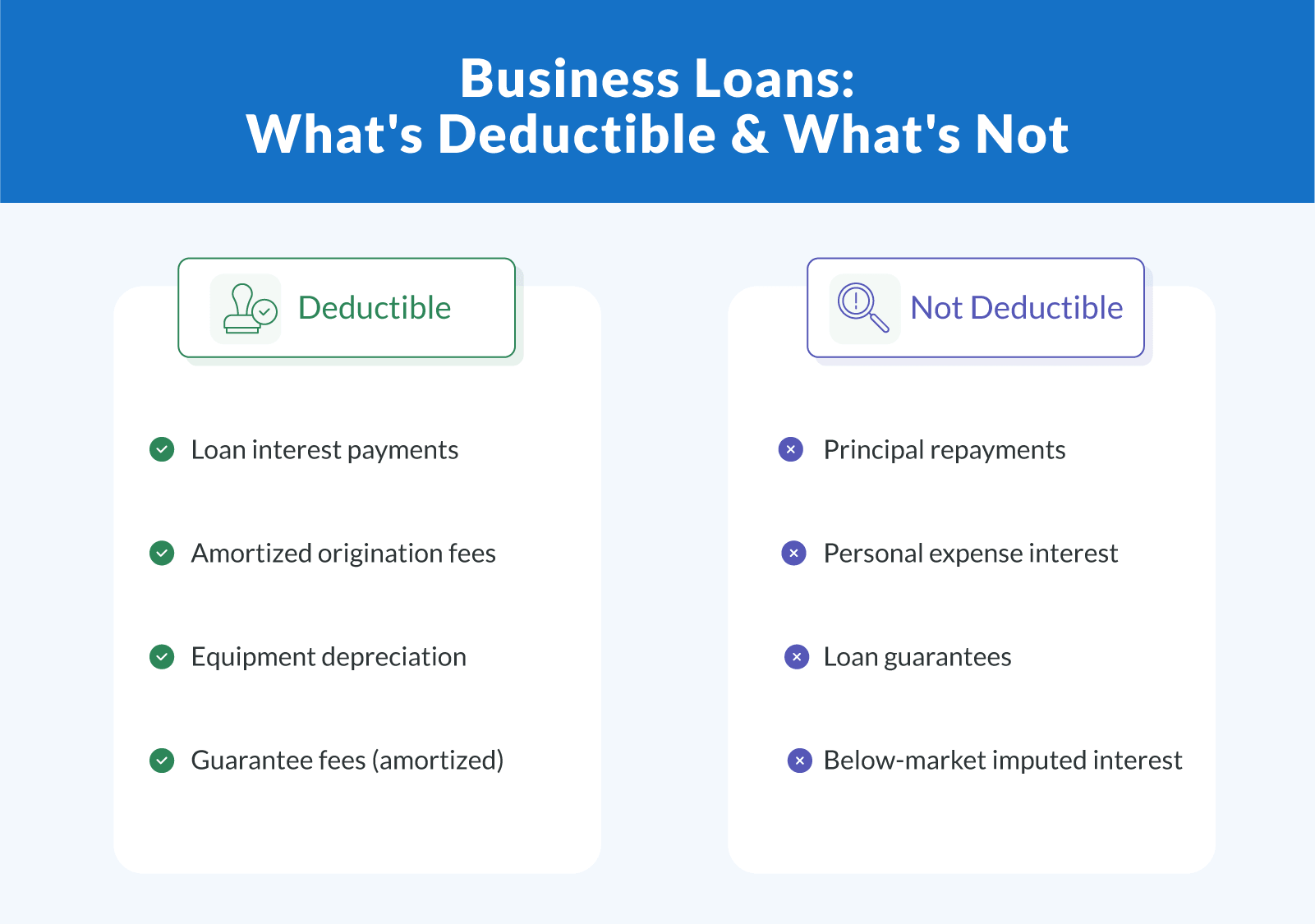

Loan Interest Payments

Business loan interest is generally tax-deductible as a business expense. The IRS requires you to meet three conditions for the interest deduction to apply:

Legally liable. You must be the borrower who's responsible for the debt.

Intent to repay. Both you and the lender must intend for the debt to be repaid.

True debtor-creditor relationship. The arrangement must be a legitimate loan, not a gift or informal agreement.

If you've borrowed money from a bank, credit union, or online lender for business purposes, you almost certainly meet all three. The interest you pay throughout the tax year qualifies as a deductible expense, reducing your taxable income dollar for dollar.

Your interest rate and repayment schedule affect how much you can deduct in a given year. Higher rates mean larger deductions (though you're still paying more overall). Only the interest portion of each installment is deductible; principal repayments are not.

Remember, though, that an interest deduction isn't the same as a tax credit. A deduction reduces your taxable income, while a credit directly reduces the taxes you owe. Business loan interest falls into the deduction category.

Origination Fees and Closing Costs

Many lenders charge up-front origination fees when you take out a business loan (typically 1% to 6% of the loan amount). These fees aren't immediately deductible in most cases. Instead, you must capitalize them and deduct the amortized cost over the repayment period.

For example, if you pay $3,000 in origination fees on a five-year term loan, you'd deduct $600 per year. Your loan agreement should detail these costs, and a CPA can help calculate the correct amortization schedule for your tax return.

Equipment Depreciation

Equipment financing offers tax benefits beyond the interest deduction. The IRS allows depreciation deductions for business assets, and Section 179 lets eligible taxpayers deduct the full purchase price of qualifying equipment in the tax year it's placed in service.

That means if you finance a $50,000 piece of equipment, you may be able to deduct both the loan interest and the equipment's cost through depreciation. Talk to your tax professional about which depreciation method makes the most sense for your business needs.

How Tax Deductions Work by Loan Type

Different types of business financing carry different tax rules. The deductibility of your interest payments and fees depends on how the loan is structured and how you use the funds.

| Type of loan | What's deductible | What's not deductible | Notes |

|---|---|---|---|

| Term loans | Interest payments, amortized origination fees | Principal repayment | Interest is deductible as you pay it over the payment schedule |

| SBA loans | Interest payments, guarantee fees (amortized) | Principal repayment | Lower interest rates mean smaller deductions, but better overall cost |

| Business lines of credit | Interest on amounts drawn | Principal repayment, unused credit fees (varies) | Only the interest on what you actually borrow is deductible |

| Equipment financing | Interest payments, equipment depreciation | Principal repayment | Section 179 may allow full deduction of equipment cost in year one |

| Merchant cash advances | Factor rate fees (consult a tax professional) | Repayment of advance principal | MCAs use factor rates, not interest; deductibility is complex |

| Business credit cards | Interest on business purchases | Interest on personal expenses | Keep business and personal spending on separate cards |

| Personal loans for business | Interest proportional to business use | Interest tied to personal expenses | You must document the percentage used for business purposes |

Term Loans

Term loans are the most straightforward option for tax deductions. You borrow a lump sum, repay it on a fixed payment schedule, and deduct the interest as a business expense. Whether you have a short-term loan (six to 24 months) or a longer repayment period (three to 10 years), the interest deduction works the same way.

Each monthly payment includes both principal and interest. Your lender should provide a breakdown on your periodic statements showing how much goes toward each. Only the interest portion is deductible.

SBA Loans

Small Business Administration loans often carry lower interest rates and longer terms, which means your annual interest deduction may be smaller per dollar borrowed. But SBA loans also come with guarantee fees paid to the Small Business Administration, and those fees are generally deductible when amortized over the life of the loan.

SBA loans are a strong option for borrowers who want predictable monthly payments with favorable terms. The interest you pay remains fully deductible as long as you use the loan proceeds for legitimate business purposes.

Business Lines of Credit

With a business line of credit, you only pay interest on the amount you draw, not the full credit limit. That makes your interest deduction variable from year to year, depending on your borrowing activity.

Lines of credit are popular for managing cash flow gaps and covering working capital needs. Interest deductibility works the same as other business loans: the funds must be used for business-related expenses.

Equipment Financing

Equipment financing combines two potential deductions: loan interest and depreciation. The interest payments are deductible like any other business loan, and the equipment itself can be depreciated on your tax return.

Section 179 allows qualifying businesses to deduct the full cost of eligible equipment in the tax year it's placed in service, rather than spreading the deduction over several years. Combined with interest deductions, this type of loan can deliver significant tax benefits for capital-intensive businesses.

Merchant Cash Advances

Merchant cash advances work differently from traditional business loans. Instead of charging an interest rate, providers use a factor rate (typically 1.08 to 1.45) to calculate the total repayment amount. Because the cost isn't structured as interest, the deductibility of those fees is less clear-cut.

Some tax professionals treat factor rate fees as a deductible business expense, while others handle them differently depending on how the advance is classified. If you've taken out a merchant cash advance, consult your CPA about the specific tax treatment for your situation.

Business Credit Cards

Interest on business credit card balances is deductible as long as the charges were for business expenses. The challenge is making sure personal expenses don't end up on your business card. Mixing the two makes it harder to substantiate your deductions and could create problems during an audit.

Keep a dedicated credit card for business purchases and maintain records of every transaction. Your card issuer will provide year-end statements showing how much interest you paid.

Personal Loans Used for Business

If you use a personal loan for business purposes, you can deduct the interest attributable to business use. The catch: you need clear documentation showing what percentage of the loan funded business-related expenses versus personal expenses.

For example, if you took out a $20,000 personal loan and used $15,000 for your business, 75% of the interest is deductible. Keep records of how you allocated the funds, because the IRS requires borrowers to prove the business use percentage.

IRS Rules That Affect Your Business Loan Tax Deduction

The IRS doesn't let all businesses deduct unlimited interest. Several rules affect how much you can write off and when.

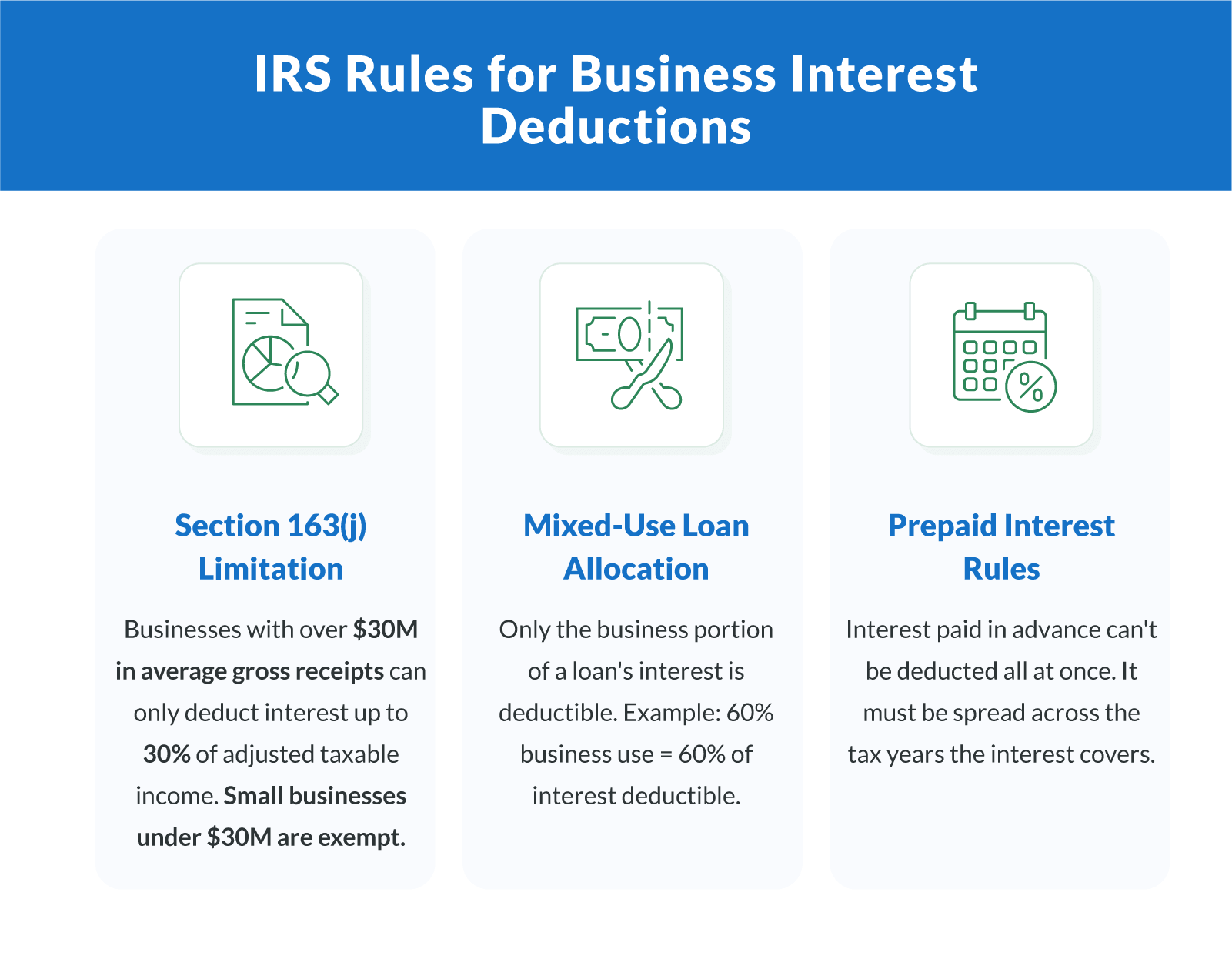

Section 163(j) Business Interest Limitation

Under Section 163(j) of the tax law, businesses with average annual gross receipts exceeding $30 million over the prior three tax years face a cap on interest deductions. The deductible amount is limited to the sum of:

Business interest income. Interest you earn from business activities (bank accounts, customer loans, investments).

30% of adjusted taxable income. Your business income before certain adjustments.

Floor plan financing interest. Applies mainly to auto dealerships and large equipment retailers.

Small business owners with gross receipts under $30 million are exempt from this limitation, meaning their business loan interest is fully deductible. If you exceed the threshold, any nondeductible interest can be carried forward to future tax years.

Real estate businesses and certain farming operations can elect out of the 163(j) limitation entirely, though specific trade-offs apply. IRS Form 8990 provides the calculation framework for taxpayers subject to these rules.

Mixed-Use Loans (Business and Personal)

If a loan serves both business and personal purposes, you can only deduct the interest that corresponds to business use. The IRS requires a reasonable allocation method, typically based on how you spent the loan proceeds.

This comes up most often with vehicle loans and home equity lines of credit. If you use your car 60% for business, 60% of the auto loan interest is deductible. Document your business use carefully, because the IRS can disallow deductions you can't substantiate.

Prepaid Interest Rules

If you pay interest in advance (for example, paying a full year of interest up front on a new loan), you can't deduct the entire amount in that tax year. The IRS requires you to allocate prepaid interest across the tax years it covers.

This prevents taxpayers from accelerating deductions by prepaying interest. Your interest deduction must match the period the interest actually applies to, regardless of when you wrote the check.

What You Can't Deduct

Understanding what doesn't qualify is just as important as knowing what does. Here are the business loan costs that won't reduce your tax bill:

Principal repayments. The money you borrowed isn't income, and paying it back isn't an expense. Principal payments simply reduce your liability.

Interest on personal expenses. If loan proceeds fund personal spending, that portion of the interest isn't a business expense, even if the loan is in your company's name.

Loan guarantees. Co-signing someone else's loan doesn't create deductible interest for you. You need to actually make interest payments on your own debt for the deduction to apply.

Imputed interest on below-market loans. If you borrow from a family member or related party at below-market interest rates, the IRS may assign "imputed interest" based on the applicable federal rate. The tax implications get complicated quickly; consult a tax professional if this applies to you.

How To Claim Business Loan Interest on Your Tax Return

The mechanics of claiming your interest deduction depend on your business structure. Here's where to report it:

Sole proprietors. Report business loan interest on Schedule C (Form 1040), Line 16.

Partnerships. Deduct interest on Form 1065 (U.S. Return of Partnership Income).

S corporations and C corporations. Report interest expense on Form 1120S or Form 1120.

LLCs. Follow the tax return rules for however your LLC is classified (sole proprietorship, partnership, or corporation).

Records You Should Keep

The IRS expects you to maintain documentation supporting every interest deduction you claim. At minimum, keep these records organized:

Loan agreements (including repayment schedules and interest rates)

Monthly or periodic statements showing principal and interest breakdowns

Payment confirmations for each installment

Records showing how loan proceeds were used for business purposes

Origination fee documentation and any amortization schedules

If you're ever audited, these records substantiate your debtor-creditor relationship and prove the eligibility of your deductions. Consider working with a CPA or tax professional who specializes in small business tax filing to make sure everything is handled correctly.

Should You Use a Loan or Equity To Fund Your Business?

This is a question I hear regularly, and the answer usually comes down to more than just taxes. But from a purely tax perspective, debt financing has a clear advantage: interest payments are deductible, while equity doesn't create any deduction at all.

When you bring in an equity investor or grow the fund from personal savings, there's nothing to write off. You don't pay interest, so there's no interest deduction. You might avoid the obligation of repayment, but you also miss out on a tool that can meaningfully reduce your tax bill each year.

That said, taxes shouldn't be the only factor. Consider how each option affects your cash flow, ownership, and long-term financial flexibility. A loan creates a fixed repayment obligation with monthly payments, while equity preserves cash flow but dilutes your control. Some business owners use a combination, and others tap into retirement plans or personal savings to avoid debt entirely.

The right choice depends on your specific financial situation, growth goals, and risk tolerance. A tax professional can help you model both scenarios so you're making a decision based on real numbers, not assumptions.

Ways To Maximize Your Business Loan Tax Benefits

A few smart moves can help you get the most out of your deductions:

Separate business and personal finances. Use a dedicated bank account and credit card for all business-related spending. Clean separation makes it easy to track deductible interest and substantiate your claims.

Time your financing strategically. If you expect higher business income next year, consider finalizing your loan late in the current tax year. You'll start accruing deductible interest immediately while aligning the larger deductions with the higher-income year.

Review origination fees for amortization opportunities. Don't overlook the deductibility of up-front loan fees. Even though they aren't fully deductible in year one, the annual amortization adds up over the repayment period.

Consider refinancing. Refinancing an existing loan at a lower interest rate reduces your total cost. While the annual deduction may shrink, you save more overall. Any remaining unamortized fees from the original loan may become deductible when you refinance.

Work with a tax professional. Tax law changes frequently, and the rules around business interest limitations, depreciation, and entity classification can get complex. A CPA who understands small business financing can identify deductions you might miss and keep you in compliance.

Smart Borrowing Starts With Understanding Your Tax Benefits

Knowing how your business loan affects your taxes puts you in a stronger position. Interest payments, origination fees, and equipment depreciation can all work in your favor when you track them properly and file correctly. The key is understanding which expenses qualify, maintaining clean records, and getting professional guidance when the rules aren't straightforward.

At Clarify Capital, we help small business owners find the right financing for their business needs, with fast funding and transparent terms. Whether you're looking for a term loan, a line of credit, or equipment financing, we can show you your options.

Ready to find the right loan for your business? Apply today for financing through Clarify Capital.

Frequently Asked Questions

I get a lot of questions from business owners about the tax side of borrowing. Here are the ones that come up most often.

Are Business Loans Tax Deductible?

The loan itself isn't deductible because it's not income or an expense. However, the interest you pay on a business loan is generally tax-deductible as a business expense, as long as you use the funds for business purposes and meet IRS requirements for deductibility.

Can You Write Off a Business Loan as an Expense?

You can't write off the loan principal or the loan payments themselves. But you can deduct interest payments, amortized origination fees, and (in the case of equipment financing) depreciation on the purchased asset. These deductions reduce your taxable income and lower your overall tax burden.

Is Business Loan Interest Deductible for Sole Proprietors?

Yes. Sole proprietors report business loan interest deductions on Schedule C of their tax return. The same eligibility rules apply: the loan must be for business purposes, and you must have a legitimate debtor-creditor relationship with the lender.

Should I Use a Loan or Equity for Tax Benefit?

From a tax perspective, loans offer a clear advantage because interest payments are deductible. Equity investments (whether from investors or personal savings) don't generate any tax deduction. However, loans require repayment, so consider your cash flow and overall financial picture before choosing.

What Is the $10,000 Auto Loan Tax Deduction?

For tax years 2025 to 2028, taxpayers can deduct up to $10,000 per year in qualified interest paid on loans for new, American-assembled passenger vehicles. This is a personal deduction, not specific to business loans. If you use a vehicle for business, you may also be able to deduct auto loan interest as a business expense based on the percentage of business use.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts