Lenders rely on detailed financial projections and business plans created by entrepreneurs to assess risk and repayment ability. According to the Small Business Association (SBA), it’s the “foundation of your business.” So if you're serious about getting funding, this is the place to start.

A strong business plan can help you secure the funding to grow it. If you're applying for a business loan, banks, credit unions, and SBA lenders want to see a clear, organized, and realistic plan before they'll consider approval.

Here, I'll show you how to write a business plan for a loan that gives lenders confidence. I'll give you step-by-step tips, guidance on what lenders expect, and an editable template to plug your details into.

Download our Lender-Ready Business Plan Template:

Types of Business Plans: Traditional vs. Lean Startup

Before you start writing, you should know which type of business plan fits your situation. Most business plans fall into one of two categories: traditional or lean startup.

Traditional business plan. This is the format most lenders expect. It's detailed, typically 15 to 25 pages, and covers all the key elements of your business, from your executive summary to financial projections. If you're applying for a bank loan, SBA loan, or any formal business financing, a traditional plan is the way to go.

Lean startup plan. This is a shorter, high-level version (usually one or two pages). It summarizes only the most important parts of your strategy. A lean plan works well as an internal roadmap or for alternative lenders who don't require a full business plan.

Below, we'll focus on writing a strong business plan in the traditional format (the kind that gives lenders the detail and confidence they need to approve your loan application). The sections below walk through each part of that plan step by step.

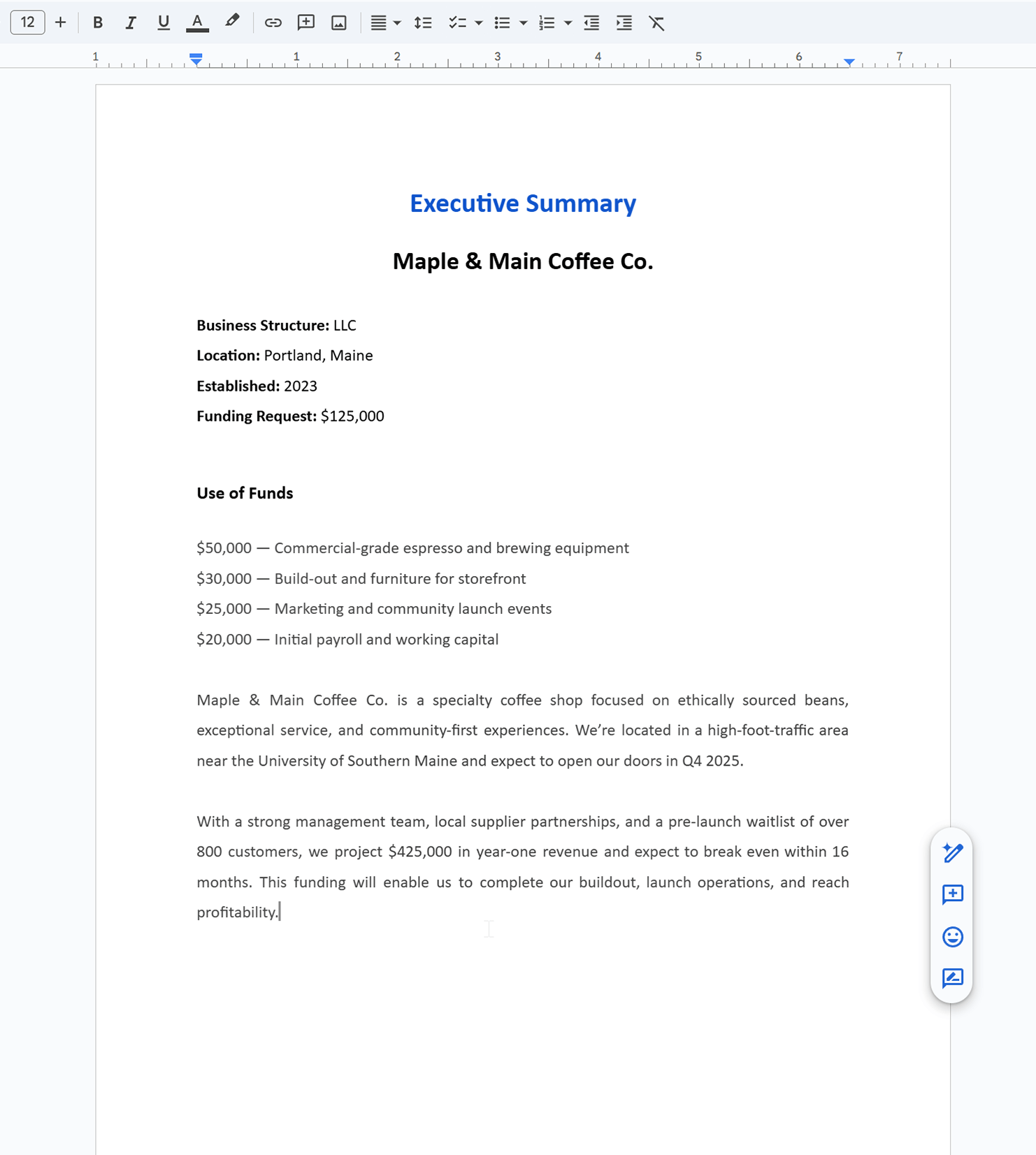

Executive Summary: Your Business in a Nutshell

The executive summary is the first thing lenders read, and often the only thing they remember. This section should quickly highlight what your business does, why it exists, how much funding you're requesting, and how you plan to use it.

Keep it short but specific. Focus on what matters to lenders: your business model, your goals, and how their money will help you reach them.

Lenders often want to see a confident, clear plan right up front. They expect the executive summary to explain what sets your business apart and why you're a good investment.

Key things to include are:

Business type and structure. Describe your company in one or two sentences. Are you a service-based LLC, a product-based C-corp, or something else?

Funding request and use of funds. Be direct. Example: "We are requesting $150,000 to purchase inventory, hire two employees, and expand our marketing reach."

Business goals. Share what this loan will help you achieve over the next 12–24 months.

Company Overview: Who You Are and Why You'll Succeed

The company overview, sometimes called the company description, sets the stage for your loan application. It gives lenders the context they need to trust that your business is viable and ready to grow.

Start with your legal structure. Are you a sole proprietorship, LLC, S-Corp, or partnership? Make this clear, and include your business location and the year you started. If your business is still in the startup phase, explain your launch timeline.

Share your mission statement. This should be a brief sentence or two explaining why your business exists. This information helps lenders connect with your purpose and understand your long-term focus.

Describe your business idea in plain language. What are you offering, and who are your customers? Be direct about the problem you solve and how your product or service delivers real value.

Show why you're different. Highlight your value proposition: what sets you apart from competitors? Ideas for what to highlight could include your pricing model, faster delivery, better customer service, or a niche product with high demand.

Together, these elements show lenders that you're prepared in addition to passionate.

Market Research and Competitive Analysis

Lenders want proof that you know your market and understand your customers. This section gives them confidence that there's real demand for your business and that you've done your homework.

Identify your target market. Who are your ideal target customers? Define their age, location, income level, or business type (whatever details help paint a clear picture). The more specific, the better.

Summarize your market research. Share trends that show your industry is growing or stable. Reference reliable sources, and back up your assumptions with real data when possible.

Break down your competitive analysis. List your main competitors and how you compare. What are they doing well? Where do you have an edge?

Give an overview of your marketing plan. How will you reach your customers? Mention channels like social media, paid ads, email marketing, or in-person events. Show that you have a strategy to get in front of your audience, and a plan to convert them.

One effective way to organize the competitive analysis is through a SWOT analysis: a simple framework that maps out your strengths (competitive advantages), weaknesses, opportunities, and threats. Lenders find this format clear and useful because it shows you've thought honestly about where your business stands and where the risks are.

Marketing and Sales Strategy

Lenders want to know what you sell and how you plan to sell it. This section outlines how you'll attract and retain customers, convert leads into sales, and keep revenue flowing.

Start by summarizing your marketing strategy. Explain which channels you'll use to reach your audience (think social media, paid ads, content marketing, or email campaigns). Be specific. If your audience spends time on Instagram or LinkedIn, say so.

Next, break down your sales plan. Describe how you'll move prospects through your funnel, from awareness to purchase. Mention any tools or systems you'll use, like a CRM, email automation, or follow-up process.

Talk about pricing, too. Show that your pricing aligns with your market, and explain how it supports your overall revenue goals.

Finally, outline any sales strategies you use to retain customers and encourage repeat business. Think loyalty programs, referral incentives, or upsells.

Offering up this information is how you can help lenders see the path between your marketing efforts and your projected revenue. It also shows them you've thought through how to launch and how you've planned how to grow.

Management Team and Operations

Even the best business idea needs strong people to bring it to life. This section shows lenders that you've got the right team and systems in place to execute your plan.

Start with your management team. Introduce the key players (your leadership team) running the business. Include their names, roles, and a summary of their experience. If anyone has worked in the same industry, grown a business before, or led successful teams, call that out.

Then, provide a simple organizational chart. It doesn't need to be fancy, just a visual that outlines who's responsible for what.

Next, describe your operational plan. Walk through how your business runs on a daily basis. What happens behind the scenes to fulfill orders, deliver services, or support customers? If you rely on suppliers, software, or contractors, mention them here.

Tie everything back to your business needs. For example, if part of your funding request includes hiring staff or upgrading systems, explain how those changes will improve operations and support growth.

Lenders often want to see that your business is an organized, well-run operation with a capable team behind it.

Products or Services Offered

This section lays out exactly what your business sells. Lenders often want to see that your product line and service offerings are clearly defined, competitive, and tied to customer needs.

Start by describing your core business model. Are you selling physical products, digital goods, or services? If necessary, break it down into categories.

Then, list your main offerings. Highlight key features and benefits for each one. Keep it simple but specific. Show that your products or services solve real problems and provide value.

If your offerings have a future roadmap (like new features, seasonal products, or additional services), include it. Lenders also want to understand your product lifecycle and how you plan to evolve your offerings over time. This information helps demonstrate long-term planning and growth potential.

Also, point out any competitive advantage you have. Maybe it's a proprietary product, lower price point, faster delivery, or niche market. Lenders want to know why customers will choose you over the competition.

Finally, explain how your products or services fit into your day-to-day operations. This overview ties your offerings back to your overall business strategy and funding needs.

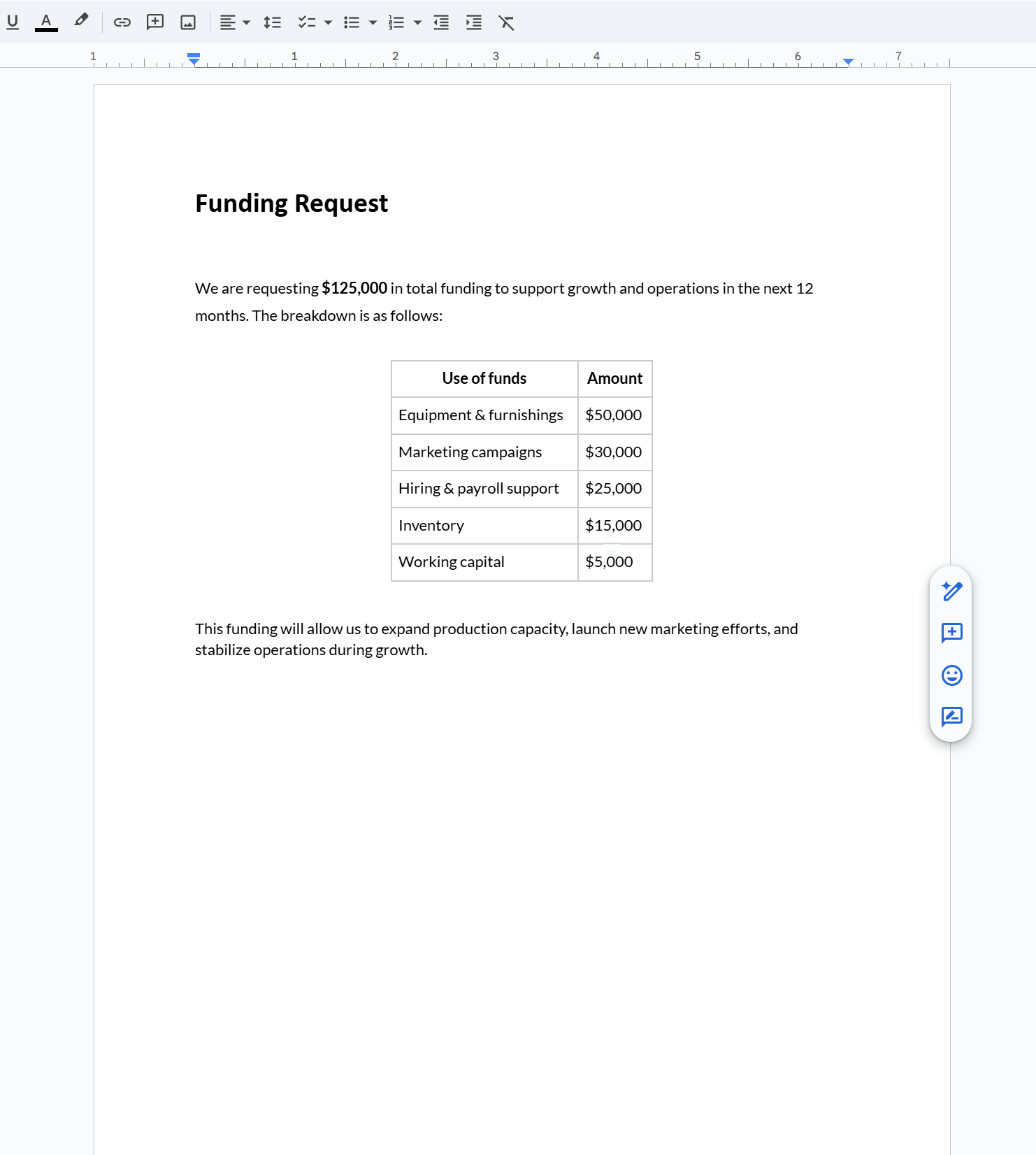

Funding Request: How Much and Why?

During this part of the process, you really need to get specific. Lenders need to know exactly how much funding you're asking for, what you'll do with it, and how it supports your business goals.

Start by stating your funding requirements in your loan application. Be direct and realistic. If you're asking for $100,000, say so.

Then break it down. Create a simple table or bulleted list that shows how the funds will be used (things like inventory, equipment, hiring, marketing, or buying real estate). If you plan to invest in growth or shore up cash flow, mention that too.

Be sure to explain how this funding will impact your business. Connect each expense to a clear outcome: more customers, higher revenue, better efficiency. By providing a greater understanding of your funding needs, you'll help lenders see that you're not just spending, you're building.

Also, touch on your credit score and financial position. If your score is strong or improving, say so. Lenders want to know you're financially responsible and likely to repay. In 2025, the SBA reported guaranteeing over 85,000 7(a) and 504 small business loans totaling $45 billion. Borrowers who present clear, well-supported funding requests are more likely to be among them.

Financial Plan: Projections and Repayment Confidence

Your financials are one of the most important parts of your business plan. Lenders often want to see that you've thought through your numbers, planned for growth, and built in room to repay the loan.

Start with your financial projections. Show three to five years of revenue forecasts, cost of goods sold, operating expenses, and net profit. Include both conservative and optimistic scenarios to demonstrate planning flexibility.

Include the core financial statements lenders expect:

Income statements. Show projected revenue and expenses.

Balance sheets. Outline your business's assets and liabilities over time.

Cash flow statements. Prove that you'll have enough liquidity to cover day-to-day operations and loan payments.

A break-even analysis is also worth including. This shows lenders the point at which your revenue covers all operating costs, which is a key indicator of your business's financial viability.

If your business is already operating, include historical financial data too. For startups, focus on forecasted numbers and explain your assumptions.

Appendix and Supporting Documents

Lenders want a written plan, plus the documentation to back it up. This section includes the supporting documents that show your business is real, legal, and ready to operate.

Here's what to include:

Legal documents. Business licenses, articles of incorporation, permits, and any contracts relevant to your operations.

Tax returns. At least two years of personal and business tax filings, if available.

Credit history. Personal and business credit reports give lenders insight into your financial reliability. If you like, you can pull your credit report in advance so you can address any issues before submitting your application.

Resumes. Backgrounds of the owners and leadership team, especially if you're in a regulated or technical industry.

Financial documents. Bank statements, profit and loss reports, or other statements not already included in your financial plan.

Providing these up front makes your loan application more complete and shows you're prepared. It also reduces back-and-forth delays (a big plus for busy lenders reviewing dozens of applications at once)

What Lenders Look For: The 5 C's of Credit

Understanding how lenders evaluate your application can make your business plan even stronger. Many lenders assess borrowers based on the 5 C's of credit: five characteristics that determine whether a small business loan gets approved:

Character. Lenders look at your personal and business credit history, education, and management experience. Your executive summary, company overview, and management team sections all speak to this.

Capacity. This is your ability to repay the loan. Lenders review your projected revenue, expenses, cash flow, and repayment plan. Your financial plan and funding request sections cover this directly.

Capital. How much of your own money have you invested in the business? Lenders use this to gauge your financial commitment. Your operational plan and financial statements should reflect this.

Conditions. This refers to the purpose of the loan and the current state of your market. Lenders often want to see product demand, industry trends, and a clear use of funds. Your market analysis, products and services, and marketing sections address these conditions.

Collateral. Some lenders require assets pledged against the loan (equipment, inventory, or real estate). If you have collateral, list it in your financial statements or appendix.

Aligning each section of your business plan with the 5 C's gives lenders exactly what they need to assess your viability as a borrower, making their decision easier.

Resources for Writing Your Business Plan

Writing a business plan on your own can feel like a big task, but small business owners have access to several free resources that can help:

SCORE. A nonprofit partner of the Small Business Administration, SCORE offers free mentoring from experienced business professionals who can review and refine your plan.

Small Business Development Centers (SBDCs). Your local SBDC provides free one-on-one business advising, including help with financial projections and loan applications.

SBA Learning Platform. The SBA offers free self-paced courses on business planning and access to local assistance programs across the country.

These resources are especially useful if you're writing a business plan for the first time or applying for an SBA loan.

Bonus: Drafting Your Plan With AI + CPA Oversight

Writing a solid business plan doesn't have to be overwhelming. AI tools can help you move faster by generating first drafts of key sections like your executive summary, financial information, or market analysis. You can use a business plan template and customize it with your own data, goals, and voice.

AI can also help organize your thoughts and catch gaps. For example, if your step-by-step funding breakdown doesn't align with your cash flow projections, the tool may flag that for review.

But don't rely on automation alone. Before submitting your plan to a lender, have it reviewed by a CPA or financial advisor. They can validate your numbers, flag risky assumptions, and offer insights to improve your good business plan even further.

It's also a smart way to make sure your plan meets any legal or tax requirements. Tools can get you most of the way there, and professional input gets you across the finish line.

Build Your Plan, Secure Your Loan

Writing a business plan might seem like extra work, but it's one of the most important steps in securing funding. A clear, lender-focused plan helps you stand out and shows that you're serious about growing your business.

Whether you're starting a new business or scaling a startup business, this is your chance to prove you're ready. Lenders want borrowers who can follow through. With the right approach, you can impress lenders with your business plan and get the capital you need.

Download your business plan template and start building your loan-ready strategy today. Clarify Capital is here to help you get funded.

Frequently Asked Questions

Here are answers to common questions business owners ask when preparing a loan-ready business plan.

Do I Need a Business Plan To Get a Loan?

Yes, many traditional lenders, including banks and those offering SBA loans, require a formal business plan. It helps them assess your company's potential and determine the viability of your funding request. Even if you're applying through alternative lenders, having a plan strengthens your application.

How Detailed Should Financial Projections Be?

Your projections should cover at least three years and include income statements, balance sheets, and cash flow forecasts. Be realistic. Lenders look for logical assumptions backed by market data. They also want to see that you've accounted for loan repayments in your forecasts.

What Documents Do Lenders Require for SBA Loans?

Along with your business plan, many lenders ask for supporting documents such as financial statements, tax returns, legal documents, and ownership details. Credit history is also important; both business and personal credit reports help lenders evaluate risk.

Can Startups Get Approved With No Revenue?

Yes, but it's harder. Lenders focus more on your business idea, management team, and personal credit when there's no operating history. Startups often need to offer collateral or apply through programs like microloans or SBA loans that are startup-friendly.

How Long Should a Business Plan Be for Lenders?

There's no strict page count, but many entrepreneurs submit plans that are 15 – 25 pages long, plus appendices. Focus on quality over quantity. Lenders care more about clear financials, a solid strategy, and strong leadership than extra fluff.

What Are the 5 C's of Credit for a Business Loan?

The 5 C's are character, capacity, capital, conditions, and collateral. Lenders use this framework to evaluate borrowers and decide whether to approve a loan. Your business plan should address each of these areas, from your credit history and management experience (character) to your financial projections and repayment ability (capacity). See the "What Lenders Look For" section above for a full breakdown.

What's the Difference Between a Traditional and Lean Startup Business Plan?

A traditional business plan is a detailed, multi-page document covering every aspect of your business. It's the format most lenders expect when you apply for a small business loan. A lean startup plan is a one- or two-page summary of only the most important elements. If you're applying for formal financing, a traditional plan is the safer choice. See the "Types of Business Plans" section above for more details.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts