Not every small business has collateral to pledge for a loan. Plenty of owners who do have it would rather not put it on the line.

A no-collateral loan, which is also known as an unsecured, collateral-free, or non-collateral loan, uses other methods of qualifying you for the loan. These include your company's revenue, as well as your credit score and current cash flow.

Below, I'll cover how no-collateral loans work, what lenders look at, and how to use the funds once you have them.

| Loan type | Collateral? | How it works | Repayment | Best for |

|---|---|---|---|---|

| Short-term loan | No | Lump sum with a fixed repayment schedule | Fixed monthly payments over 6 to 36 months | One-time expenses and fast funding needs |

| Business line of credit | No | Revolving credit drawn from as needed | Monthly payments on the amount used | Ongoing cash flow gaps and flexible spending |

| Merchant cash advance | No | Advance based on future credit or debit card sales | Percentage of daily or weekly sales | Businesses with strong card volume and urgent needs |

| Invoice factoring | No traditional collateral | Sell unpaid invoices to a factoring company for an advance | Customer pays the factor directly | B2B businesses with outstanding invoices |

| SBA Microloan (up to $50K) | Sometimes waived | Government-backed loan through SBA-approved lenders | Fixed monthly payments | Smaller funding needs with longer repayment timelines |

| Equipment financing | Yes (the equipment itself) | Loan tied directly to the purchased equipment | Fixed monthly or quarterly payments | Businesses buying machinery, vehicles, or technology |

How No-Collateral Business Loans Work

Instead of using collateral to back your loan, lenders evaluate your business. They typically look at your monthly revenue, your personal credit history and score, how long you've been in business, and your last six months of bank statements. Below, I explain the basics of no-collateral business loans so that you can feel confident picking one for your business.

Short-Term Business Loans

Short-term business loans allow you to borrow up to $5 million, with six to 36-month terms that include both weekly and monthly payment options. You can pay these loans back in installments over several months. Interest rates for these types of loans start at 6% for qualified businesses.

Business Lines of Credit

A business line of credit is a revolving source of funds to support your business. You only pay interest on the money that you borrow. Clarify offers lines of credit up to $5 million with APRs starting at 6% for qualified borrowers. The term length for lines of credit offered by Clarify is six to 36 months.

Merchant Cash Advances

Merchant cash advances (MCAs) allow you to borrow money against future sales. MCAs use a factor rate instead of an APR, often ranging from 1.08 to 1.45. For example, if a business borrows $50,000, it may be required to pay the lender 15% of each day's credit card sales until the balance is repaid.

Collateral-Free Alternatives (and One Exception)

SBA loans, SBA Microloans, and equipment financing are also worth mentioning. These financing options don't clearly fit into the "unsecured" category, but they're useful alternatives for businesses with no collateral or limited collateral.

SBA Loans

Approved lenders provide SBA loans with backing by the U.S. Small Business Administration (SBA). The SBA guarantees a part of every loan to reduce the lender's risk.

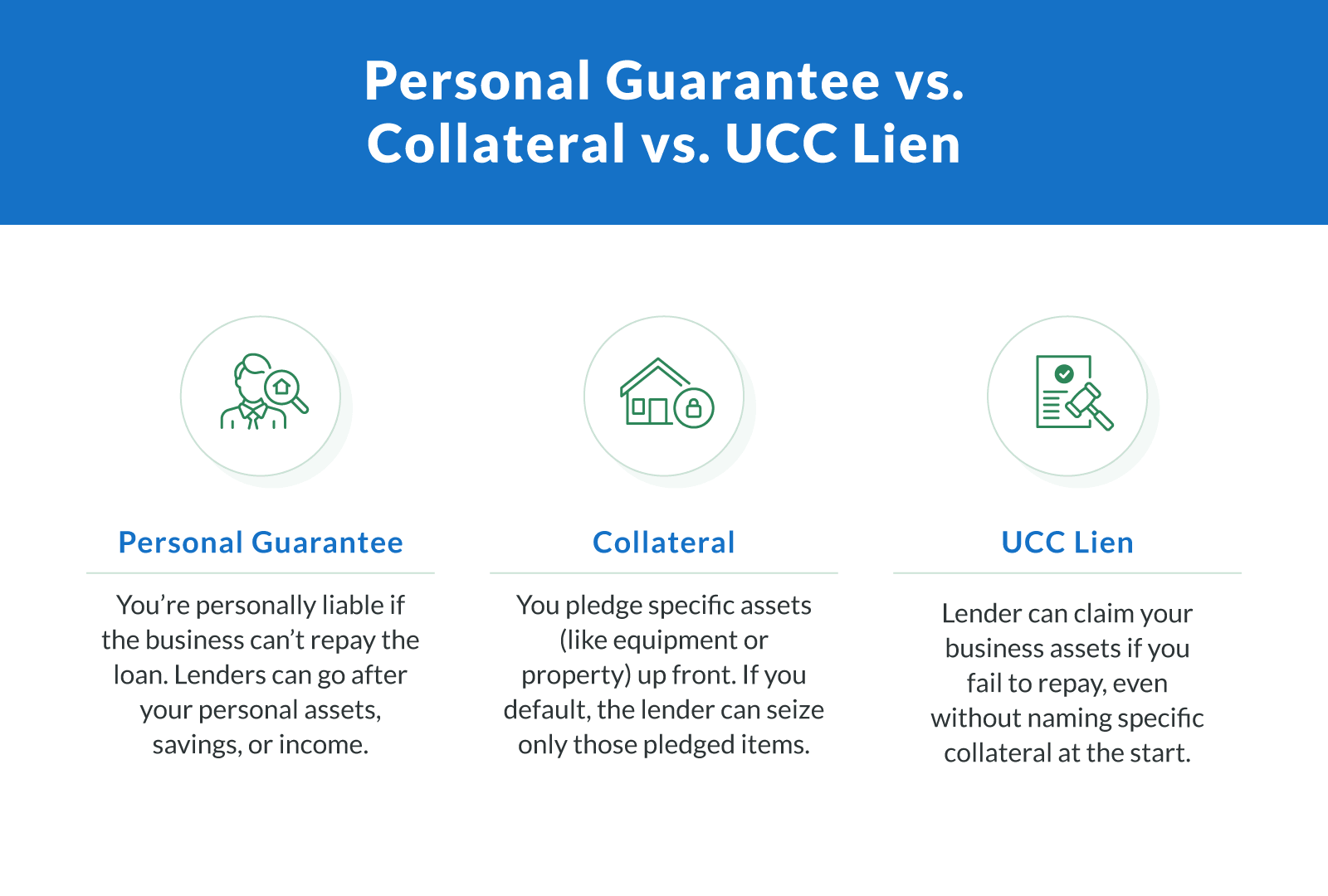

The SBA 7(a) is the most popular program for SBA loans. Lenders are not required to take collateral for loans under $50,000. SBA loans generally require a personal guarantee from those who own 20% or more of the business.

SBA loans generally offer better interest rates and repayment terms than many of the other options available in this list. But SBA loans can also take longer and involve much more paperwork. It normally takes 30 to 60 days for an SBA loan application to be processed, and it requires considerably more documentation than alternative lending products.

SBA Microloans

SBA Microloans are a separate program from SBA 7(a) loans. Microloans are capped at $50,000, and most SBA Microloan intermediaries require both collateral and a personal guarantee.

Equipment Financing

Equipment financing uses collateral, but the equipment itself is the only asset on the line. That's why owners with few additional assets find it an attractive option. Lenders usually tie the funding amount to the equipment's price, and the loan term usually matches the equipment's expected lifespan. If you default, the lender can repossess the financed equipment. That's the extent of their claim. Nothing else in the business is at risk.

Secured vs. Unsecured Business Loans

Choosing between a secured and an unsecured loan is a tradeoff. Here's how the two compare.

| Factor | Secured business loans | Unsecured business loans |

|---|---|---|

| Collateral | Requires business or personal assets | No assets required |

| Interest rates | Generally lower because the lender has collateral as a safety net | Typically higher because the lender takes on more risk |

| Loan amounts | Higher borrowing limits available | Usually smaller amounts |

| Repayment terms | Longer repayment schedules | Shorter terms, often 6 to 36 months |

| Approval speed | Slower due to asset appraisals and documentation | Faster, sometimes as fast as same-day |

| Risk to borrower | Lender can seize pledged assets on default | No asset seizure, though a personal guarantee may apply |

Banks and credit unions have always held strict requirements for approving unsecured business loans. Alternative lenders like Clarify Capital approve far more unsecured loan applications than traditional banks. We fund businesses with FICO scores as low as 500 and only require six months in business.

When a No-Collateral Loan Is the Better Choice

Secured loans can be a good option when you need to finance something, but sometimes the risk of losing your assets isn't worth the potential rewards. Below are four examples of times that an unsecured loan might be a smarter choice.

You don't have anything to use as collateral

Some businesses do not own any expensive equipment or property, and may find it easier to get funded without these types of assets.

You need fast funding

When your cash flow is in a tight spot, speed matters. Many no-collateral loans can be funded as fast as the same day.

You don't want to put your personal property at risk

Not every small business owner wants to use their personal assets as collateral for an unsecured loan.

You need funding for a short period of time

Covering a cash gap in your business or restocking inventory or hiring seasonal staff does not usually require a long-term secured loan.