Most business owners with a low credit score assume the answer is no before they ask. It usually isn't. Over more than a decade of arranging financing for small and midsize businesses, I've seen plenty get approved with personal scores in the 500s, because the right lender looks at your revenue and cash flow alongside your credit, rather than the number on your report alone.

Bad credit does change the terms. Expect smaller amounts, higher rates, and more revenue-based options than a borrower with strong credit would see. Below, I cover which business loans accept lower scores, what each one costs, and the steps that improve your approval odds before you apply.

| Loan type | Minimum credit score | Loan amount | Financing speed | Best for |

|---|---|---|---|---|

| Merchant cash advance | 500 | Up to $5 million | As fast as same day | Steady card and bank sales, fast cash |

| Short-term business loan | 550 | $10,000 to $5 million | As fast as same day | A lump sum for a near-term need |

| Equipment financing | 550 | Up to 100% of equipment value | 1 to 5 days | Buying machinery, vehicles, or tools |

| Business line of credit | 600 | Up to $5 million | As fast as same day | Flexible, reusable working capital |

| Invoice factoring | Based on your customer's credit | Up to 100% of invoice value | 1 to 2 weeks | Unpaid invoices tying up cash flow |

| Home equity line of credit (HELOC) | 620 | Up to $750,000 | As quickly as one week | Business owners with home equity and thin business credit |

| SBA Microloan | Varies by lender | Up to $50,000 | Several weeks | Smaller or newer businesses needing modest capital |

Can You Get a Business Loan With a 500 Credit Score?

Yes. You can get a business loan with a 500 credit score, though your loan options narrow to revenue-based financing like a merchant cash advance (MCA), which approves based on your sales rather than your credit. A 500 score won't qualify you for a bank term loan or most Small Business Administration (SBA) loans, but alternative lenders finance businesses in that range every day. Clarify Capital's business loans for bad credit are built for exactly that situation.

You don't need perfect credit, or even good credit, to get financed. The trade-off is cost. A lower score signals more risk, so lenders offset it with higher rates, shorter terms, or a slice of your daily sales. If your revenue is steady, that trade can still pencil out.

What Counts as Bad Credit for a Business Loan?

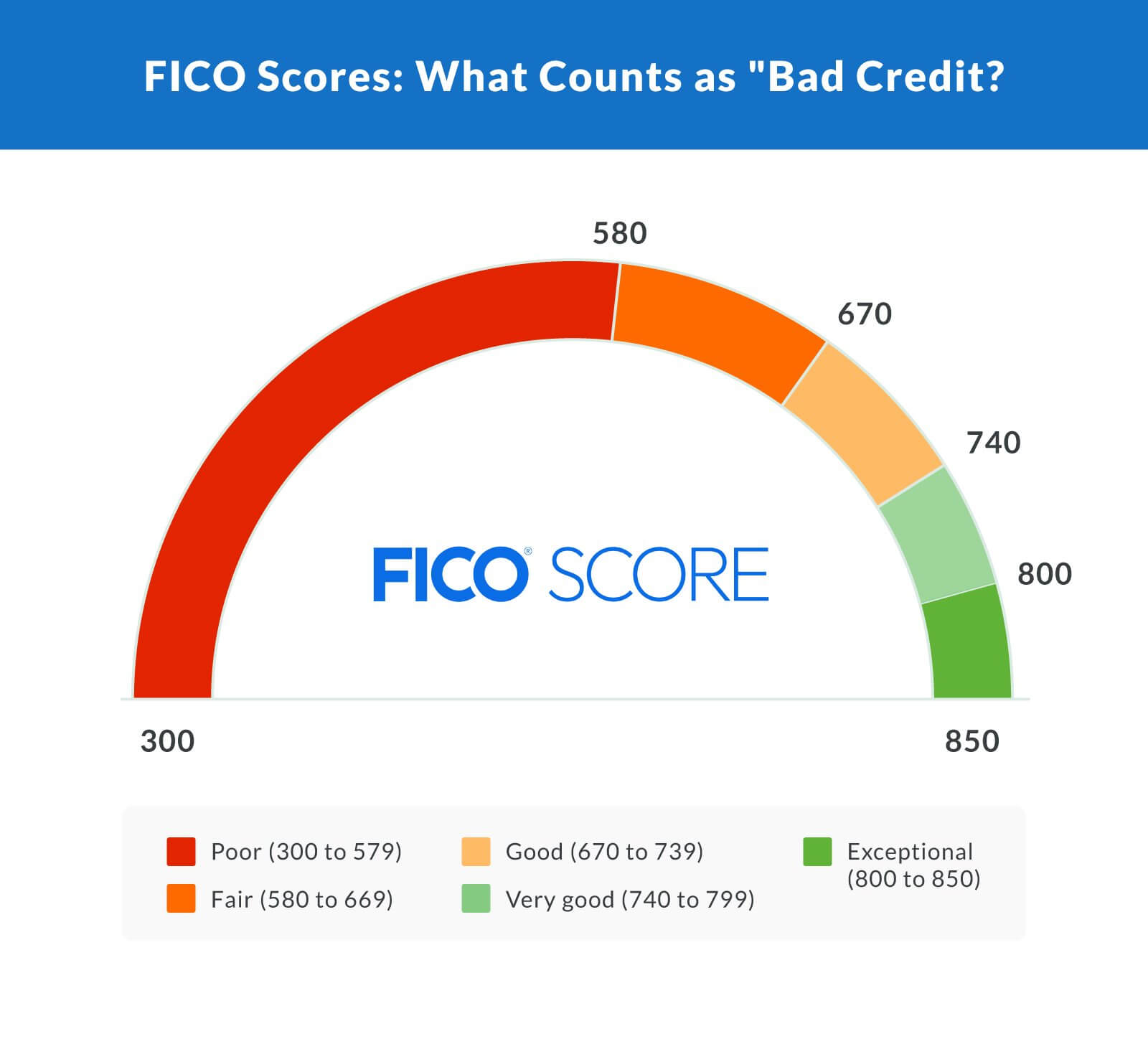

Most lenders read your personal FICO score on a 300 to 850 scale. The ranges most lenders use run from poor (300 to 579) and fair (580 to 669) up through good (670 to 739), very good (740 to 799), and exceptional (800 to 850). When lenders say bad credit, they usually mean the poor range and the low end of fair, roughly under 600.

For context, the average FICO score in the United States reached 713 in 2025, so a score under 600 sits well below the middle, which shapes who will work with you and on what terms. Some traditional banks and other financial institutions treat a sub-600 score as a near-automatic decline, while online lenders and other alternative providers weigh it against your revenue. Traditional lenders also set firmer credit score requirements than alternative lenders do. Lenders read your creditworthiness during underwriting, and poor credit tells them to look harder at everything else.

Your business has its own credit score, too, separate from your personal one. New businesses often have little or no business credit history, so lenders lean on your personal credit score and your revenue instead. As your business credit profile grows, more options open up. The exact cutoff depends on the loan, since the minimum credit score for a business loan shifts with the loan type and the lender.

Types of Business Loans for Bad Credit

The loans below are the ones most likely to approve a business owner with bad credit when traditional loans are off the table. Each underwrites a little differently and carries its own eligibility requirements, so the best fit depends on your revenue, your assets, and how fast you need the money.

Merchant cash advance

Gives you a lump sum up front in exchange for a slice of your future sales. Approval leans on your daily debit card and credit card sales and bank deposits, not your credit, which is why scores as low as 500 can qualify. Repayment flexes with your sales, so slow weeks cost less, but the factor rates (from 1.08 to 1.45) run higher than a typical interest rate. Best for businesses with steady volume and a clear use for the cash.

Short-term business loan

A fixed lump sum you repay over 6 to 36 months, usually with weekly or biweekly payments. Minimums start around a 550 score and $10,000 in monthly revenue. Unlike longer-term loans, it gives you a clean payoff date, which makes it a solid choice when you know exactly what you need, though the shorter schedule means larger payments.

Equipment financing

Uses the machine, vehicle, or tool you're buying as collateral. Because it's a secured loan, the lender's risk is lower, and approvals reach down to about a 550 score. You can finance up to 100% of the equipment value and repay over the life of the asset, often 12 to 72 months. A larger down payment can lower the rate further.

Business line of credit

Works like a revolving account: draw what you need for working capital, pay interest only on what you use, and reuse it as you repay. It typically calls for a 600 score, a higher bar than a cash advance, but it's the most flexible way to cover uneven expenses. For business owners rebuilding credit, a line of credit built for bad credit can be a realistic starting point.

Invoice factoring

Turns unpaid invoices into cash now. A factoring company advances most of the invoice value, then collects from your customer directly. Because approval rides on your customer's credit rather than yours, your own score is rarely the deciding factor. Fees run from half a percent to 5% per invoice each month, so it works best when your receivables tie up cash and your clients pay slowly but reliably.

Home equity line of credit (HELOC)

Lets you borrow against the equity in your home and put it to work in your business. Because your home secures the line, lenders focus on your personal finances and home equity more than your business credit, though you'll generally need a 620 score. You can access up to $750,000. The catch is real: your home is on the line if you can't repay, so weigh it carefully.

SBA Microloan

A smaller loan, up to $50,000, issued through nonprofit intermediary lenders. There's no single credit cutoff because each intermediary sets its own, and many are more flexible than a bank. Financing takes several weeks, so it's not for emergencies, but it's a strong option for a smaller or newer business that needs modest capital and a longer runway.

How Bad Credit Affects Your Rates and Terms

A low score reshapes the offers you'll see, in a few predictable ways:

Smaller loan amounts. Lenders limit their exposure until you've shown you can repay.

Higher interest rates and factor rates. The rate covers the added risk, so borrowers with lower credit scores pay more than those with strong credit.

Shorter repayment terms. A faster payoff lowers the lender's risk but raises your payment.

More revenue-based options. Expect structures that key off your annual revenue and daily sales rather than your score.

A personal guarantee. Many bad credit loans ask you to back the loan personally, which puts your own assets behind it.

None of this is a reason to wait until your credit is perfect. If your revenue is steady, the right loan still fits your business needs today.

Ready to see what you qualify for?

Compare offers from 75+ vetted lenders with one 2-minute application. Checking your options won't affect your credit.

How To Improve Your Approval Odds

Improving your odds isn't complicated, and the steps to get a business loan with bad credit are mostly about showing strength where your score is weak. Work through these before you submit a small business loan application:

Check your credit first. Pull your personal and business reports from the credit bureaus, fix any errors on your credit report, and know your number before a lender does.

Lead with revenue. Three to six months of healthy bank statements often matter more than your score to an alternative lender.

Offer collateral or a larger down payment. Backing the loan with equipment, invoices, or real estate, or putting more money down, lowers the lender's risk and can help you earn better terms.

Add a co-signer. A partner or backer with stronger credit can vouch for the loan and widen your options.

Borrow less. Asking for a smaller amount you can clearly repay is easier to approve, and it builds a track record for next time.

Bring a plan. A short business plan showing how you'll use and repay the money reassures a cautious lender.

Build business credit. Open a business bank account, put recurring costs on a business credit card you pay on time, and keep your books clean so your business credit score climbs.

How To Spot a Predatory Lender

Bad credit makes you a target for lenders who hide the real cost. Look for two signs in particular: interest rates far above what other lenders quote, and fees that top 5% of the loan value. Any legitimate lender will disclose the annual percentage rate (APR) and your full payment schedule before you sign.

Trust your gut on the rest. Pressure to sign today, a lender who won't put terms in writing, and vague answers about the total cost are all reasons to slow down and compare the offer against another.

Find a Business Loan That Fits Your Credit

A low score sets the terms, not the outcome. Plenty of small and midsize business owners (SMBs) with bad credit get financed every day by matching the right loan to their revenue and moving before a cash crunch forces a bad deal. Clarify Capital works with a network of 75-plus vetted lenders and seven financing options, so instead of chasing one bank, you see what you actually qualify for across the board. The application process takes about two minutes and won't affect your credit, and a US-based lending advisor walks through your options with you.

When you're ready, apply today.

Frequently Asked Questions

A few questions come up again and again when business owners with bad credit start looking for financing. Here are straight answers to the ones I hear most.

Can I Get a Business Loan for My LLC With Bad Credit?

Yes. A limited liability company (LLC) can qualify for bad credit business financing, though most lenders still check the business owner's personal credit and ask for a personal guarantee, especially if the business has little credit history of its own. Your revenue and time in business carry real weight here, so a profitable LLC with a weak personal score still has options.

Can I Use My EIN To Get a Business Loan?

An employer identification number (EIN) alone usually isn't enough. Lenders that advertise EIN-only financing are rare, and most still look at your personal credit, your revenue, or both. Building business credit under your EIN helps over time, but for now, expect a lender to weigh your personal score alongside it.

What Credit Score Do You Need for a Business Loan?

It depends on the loan. Revenue-based options like a merchant cash advance can start around 500, a short-term loan around 550, and a line of credit around 600, while bank and SBA loans usually require 640 or higher. The lower your score, the more your revenue and cash flow have to carry the application.

What Are the Easiest Business Loans to Get With Bad Credit?

Merchant cash advances and invoice factoring are typically the easiest to qualify for, because they lean on your sales and your customers' payments rather than your credit score. Equipment financing is close behind, since the equipment itself secures the loan. All three regularly approve business owners that might not qualify for a loan through a traditional bank.

Can I Get a Startup Business Loan With a 500 Credit Score?

It's tougher. Most lenders, including the ones that work with bad credit, want at least six months in business and steady revenue, so a brand-new startup with a 500 score has fewer doors open. SBA Microloans and financing that leans on personal credit are usually the most realistic paths until you have a few months of revenue behind you.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts