Most small business owners I talk to use the word "quick" to mean two different things: I need the money by Friday, or I need the money before this opportunity disappears. The honest answer is that "quick" depends entirely on which type of small business loan you're after, and your financing options stretch from same-day funding to a 90-day SBA underwriting process. Same-day funding is possible for some options and a fantasy for others.

Here, I'll walk you through how fast each major type of quick business financing actually funds, which Clarify products fit which business needs, what lenders weigh during underwriting, and how to shave business days off your approval if the clock is ticking.

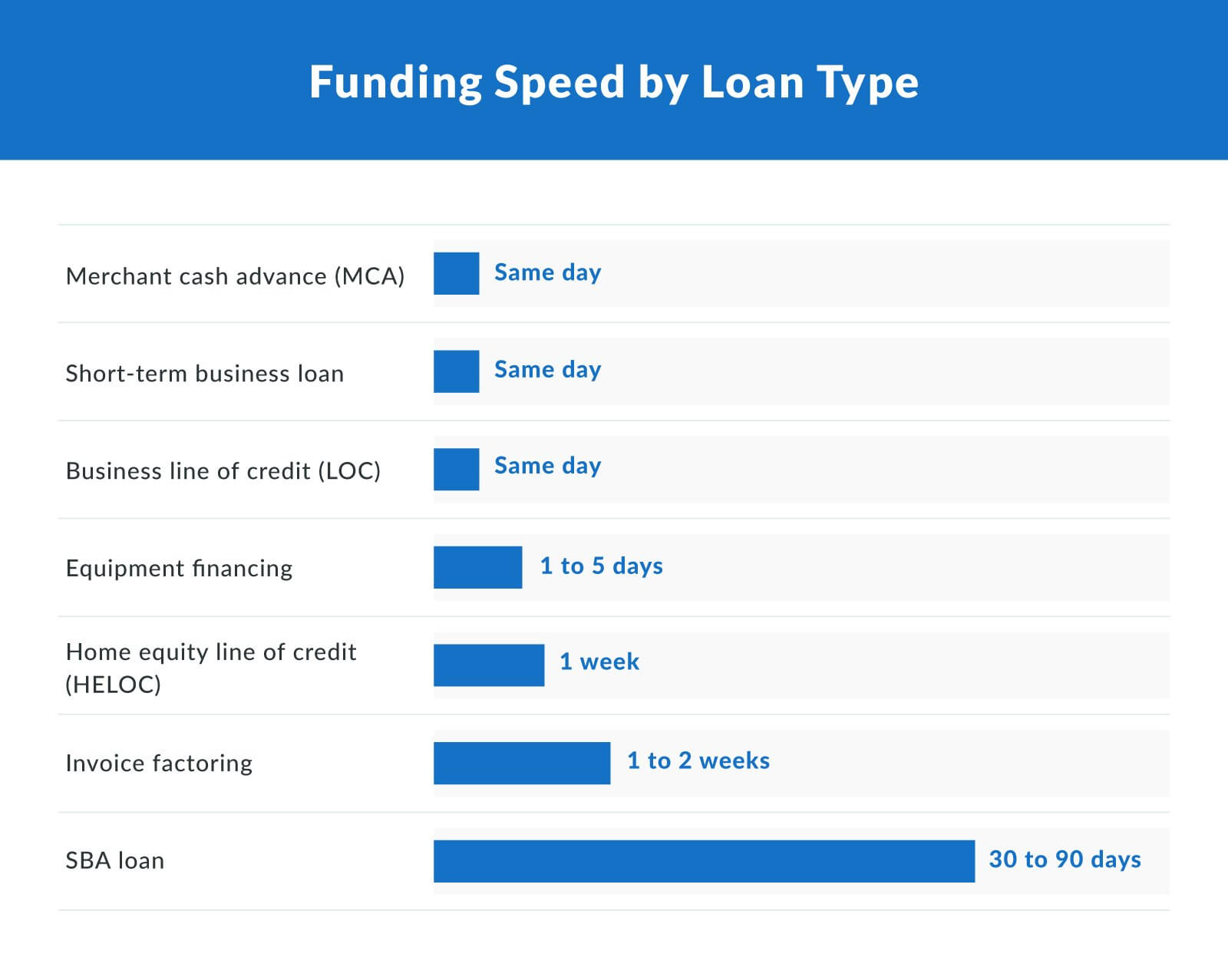

How Fast Is "Quick?" Funding Timelines by Loan Type

"Quick" is a spectrum. A merchant cash advance (MCA) can fund the same day you apply; a U.S. Small Business Administration (SBA) loan typically takes 30 to 90 days, even when everything goes right. Here's how the major loan programs compare on funding speed:

If you need money in 48 hours or less, your real options are an MCA, a short-term business loan, or drawing on an existing line of credit. If you can wait a week, equipment financing and invoice factoring open up. If you can wait a month or more, SBA financing usually wins on rate and term.

Types of Quick Business Loans

Below are the six types of small business loans I suggest when small business owners come to us for fast funding.

| Product | Loan amount | Funding speed | Rate | Repayment | Qualification floor | Best fit |

|---|---|---|---|---|---|---|

| Short-term business loan | $10,000 to $5,000,000 | As fast as same day | APR starting at 6% | 6 to 36 months; weekly, biweekly, or monthly | 550+ credit, 6 months in business, $10,000+ monthly revenue | One-time cash for a near-term opportunity |

| Business line of credit | Up to $5,000,000 | As fast as same day | APR starting at 6% | 6 to 36 months on what you draw | 600+ credit, 12 months in business, $10,000+ monthly revenue | Ongoing cash-flow flexibility |

| Merchant cash advance | Up to $5,000,000 | As fast as same day | Factor rate 1.08 to 1.45 | No fixed term; repaid via percentage of future sales | 500+ credit, 6 months in business, $10,000+ monthly revenue | Revenue-backed cash when credit is a constraint |

| Equipment financing | Up to 100% of equipment value | 1 to 5 days | APR starting at 6% | 12 to 72 months, monthly payments | 550+ credit, 6 months in business, equipment as collateral | Buying or upgrading machinery, vehicles, technology |

| Invoice factoring | Up to 100% of invoice value | 1 to 2 weeks | 0.5% to 5% per invoice per month | Tied to customer payment (typical 30, 60, 90 days) | Customer creditworthiness drives approval | Business-to-business (B2B) businesses with slow-paying customers |

| SBA loan | Up to $5,000,000 | 2 weeks to 90 days | APR starting at 6.75% | 10 to 25 years, monthly payments | 640+ credit, 2 years in business, full financials | Lower-rate financing when timeline allows |

Short-Term Business Loans

A short-term business loan is a clean path to a lump-sum infusion when you need cash in days, not weeks. Borrow $10,000 to $5 million from Clarify at APRs starting at 6%, repaid over six to 36 months. Funding can land the same day for businesses with credit scores over 550.

I've helped a restaurant operator use a short-term business loan to land a bulk supplier discount, and a trucking operator use one to cover a maintenance bill the same week a contract started. The trade-off is the short repayment window: You're paying it back fast, which means weekly or biweekly payments rather than the monthly cadence of longer-term financing.

Business Line of Credit

A business line of credit gives you up to $5 million in revolving credit you can draw against as you need it. You pay interest only on what you use. APRs start at 6%; repayment runs six to 36 months on what you draw, then the credit refills as you pay it back (much like a credit card, but underwritten on your business cash flow).

The qualification floor is a 600+ credit score, 12 months in business, and $10,000+ monthly revenue. Lines of credit are revenue-based, not collateral-based: we look at bank statements rather than business assets. For most working capital scenarios (payroll bridges, seasonal swings, surprise costs), a line of credit gives you faster access than re-applying for a new loan each time.

Merchant Cash Advances

A merchant cash advance (MCA) works differently from a loan. You sell a portion of your future sales to the funder in exchange for an up-front lump sum, then repay through a fixed percentage of daily or weekly sales until the advance plus fees is paid back. The cost is expressed as a factor rate (Clarify's range is 1.08 to 1.45), not an annual percentage rate (APR), so a $50,000 advance at a 1.30 factor rate means you repay $65,000 total.

MCAs have the lowest qualification floor of any product on this list: 500+ credit, six months in business, $10,000+ monthly revenue. That's why they're the go-to product for operators with bruised credit who still have strong revenue. Funding is typically provided on the same day. For more on same-day funding specifically, see our same-day business loans page.

Equipment Financing

Use equipment financing (sometimes called equipment loans) when the loan funds a specific asset (a vehicle, a piece of machinery, an IT upgrade) and the equipment itself serves as collateral. The collateral is what makes the qualification floor lower than an unsecured term loan; even with a less-than-perfect credit profile, you can usually get approved if the equipment holds value.

Clarify funds up to 100% of equipment value with APRs starting at 6%, repaid over 12 to 72 months. Financing lands in one to five days, which is slower than a short-term loan but still well inside the "quick" definition. Best fit: buying or upgrading machinery, vehicles, or technology that's already specced out and quotable.

Find the Right Quick Business Loan With Clarify

Apply online in two minutes. Same-day funding is available for credit scores over 550, and we can usually tell you within a few hours whether one of our loans fits your timeline.

- Loan amounts up to $5M

- APRs starting at 6%

- Funding available same day

- 50,000+ businesses funded

Won't impact your credit score.

Eligibility and Application Process

Lenders evaluating a quick business loan are answering one question: Can your business's cash flow support the repayment? The eligibility requirements vary by lender, and providers like traditional banks ask for more documentation than online lenders, but most look at the same five signals when running credit approval.

Credit score. Both personal credit and business credit factor in. A FICO score in the 700s is good credit and opens more financing options; a score in the 500s narrows the field to MCAs and a few revenue-based products. Business credit cards and other revolving accounts factor into the broader picture, too.

Annual revenue. Lenders need to see that the business is generating cash. Clarify's floor is $10,000 in monthly revenue; bank lenders typically want more.

Time in business. Most quick-funding lenders want at least six months of operating history. Clarify's minimum is six months for working-capital products and two years for SBA. Traditional banks typically want a longer operating history than online lenders.

Bank statements. Three months of recent business bank statements is the standard ask for revenue-based underwriting. A separate business bank account (not commingled with personal funds) is effectively required.

Personal guarantee. Most small-business loans require a personal guarantee from the principals, regardless of business credit. Read the fine print so you know what you're signing for.

Minimum Qualifications

$10,000 in monthly revenue

Your business must earn at least $10K per month in a business bank account.

500+ credit score

You can get approved with any credit score. But the better your credit rating, the better interest rates lenders offer. Your FICO score should be above 500.

Minimum six months in business

Your company should be operational for a minimum of six months. This shows business lenders that your company is sustainable and won't go out of business.

Have a business bank account

Your Clarify advisor will need three or four months of your most recent bank statements to verify income. This is just to see you're actually making $10K+ month in revenue.

Clarify's online application takes about two minutes. After that, a typical flow looks like this:

1. Submit the application and upload your most recent business bank statements.

2. An advisor reviews the file and matches you with the loan options that fit your revenue profile.

3. You review the term sheet (APR or factor rate, repayment cadence, fees, prepayment terms) and decide whether to accept.

4. You sign electronically. Funds land in your business checking account on the same business day for credit scores over 550, or within a few days otherwise.

For the SBA loan path specifically, the document list is longer (tax returns, financial statements, business plan, and more). Our checklist on SBA loan requirements walks through what you'll need.

Interest Rates and Repayment Terms

Two pricing concepts matter for quick business loans: annual percentage rate (APR) and factor rate. They aren't interchangeable.

APR is the annualized cost of a loan, expressed as a percentage and typically including interest plus certain fees. A 12% APR on a $50,000 short-term loan over 12 months means you pay roughly $3,300 in interest over the life of the loan. Clarify's APRs on short-term loans and lines of credit start at 6%; SBA financing starts at 6.75%.

Factor rate is used for merchant cash advances and some short-term products. It's expressed as a decimal (Clarify's MCA factor rates range from 1.08 to 1.45). A $50,000 MCA at a 1.30 factor rate means you repay $65,000 total, regardless of how fast you pay it back. Because factor rates don't amortize, the effective APR on an MCA can run much higher than a typical term loan, especially for short repayment timelines.

Repayment cadences vary. Short-term loans typically run weekly, biweekly, or monthly. MCAs repay through a fixed percentage of daily or weekly sales. SBA and equipment financing run monthly. Lines of credit follow whatever cadence the lender sets on draws.

Two potential fees to be aware of: origination fees (a one-time charge for processing the loan, which varies by lender), and prepayment penalties (fees for paying the loan off early). Not every lender charges them, but several do, and they materially affect total cost. Read the term sheet carefully.

How To Speed Up Your Approval

Most application slowdowns come from the borrower's side, not the lender's. Here's how to shave days off your approval timeline.

Have three months of business bank statements ready before you apply. This is the single most common cause of slow approval. Pull them as PDFs from your bank's portal so you can upload them immediately.

Open a dedicated business checking account if you haven't already. Commingled personal and business accounts add days to underwriting (or kill the application entirely).

Check your personal credit report before you apply. Dispute any errors with the bureau; a clean report removes back-and-forth during underwriting.

Match the loan type to your funding window. Don't apply for an SBA loan if you need cash in 72 hours. The product wasn't built for that timeline.

Fill out the application completely. Skipping fields or leaving estimates instead of exact numbers triggers follow-up questions that add a day or two each round.

Respond fast to the advisor's questions. Same-day funding for credit scores over 550 assumes same-day responses on your side, too. A 24-hour delay on a single email can push funding to the next business day.

Have your tax returns and recent financials handy. Even for revenue-based underwriting, some lenders ask for confirming documents. Having them ready prevents a second back-and-forth round.

Apply during business hours, not Friday evening. Most lenders process applications on standard business-day cycles. A Tuesday morning submission funds faster than a Friday at 5 p.m.

Trade-Offs: When Speed Costs You

Quick funding isn't free. The faster the product, the higher the cost relative to a slower-paced alternative.

An MCA funds in hours but typically costs more than a short-term loan over the same period.

A short-term loan funds in days but costs more than an SBA loan over the same multi-year horizon.

A line of credit funds same day on drawn balances once the initial application is approved.

A trade-off that's worth it: faster funding for time-sensitive opportunities where the cost of waiting exceeds the rate premium (a bulk supplier discount that expires Friday, a piece of equipment that gets the next contract signed, a contractor who needs payment to keep working on a build).

The trade-off that might not be: paying for speed that you don’t need. If you can wait a few weeks, a longer-term financing option could cost you less over the life of the loan.

If the deal you're funding isn't time-bound or has a clear revenue upside, the SBA route usually wins on total cost.

Quick Loans for Startups, Bad Credit, and Tough Situations

Not every business fits the standard quick-loan box. Two situations come up most:

Bad credit

Clarify works with credit scores as low as 500 (on MCAs). For owners with bruised credit but solid monthly revenue, MCAs and short-term business loans are usually the best fit. Rates are higher to reflect the risk, but approval is meaningfully easier than at a bank.

True startups and new businesses

Clarify's minimum is six months in business. If you're at month one or month three of operating, we can't fund you yet. For pre-six-month new businesses, the realistic business funding options are SBA Microloans through certified intermediary lenders, or personal-credit-based options like a business credit card or a personal loan you use for business expenses.

Whatever your situation, the honest first step is the same: pull your credit, gather three months of bank statements, and figure out which loan type your revenue actually supports.

Your Next Step

The right quick business loan depends on three things: how fast you need the money, what your credit and revenue look like, and how the cost of waiting compares to the cost of borrowing fast.

Small business financing isn't one-size-fits-all, so match the loan amounts and timeline to your specific business needs. For most operators with at least six months in business and $10,000+ in monthly revenue, a short-term business loan or business line of credit funds in a day or two, and runs at APRs starting at 6%. For revenue-strong operators with weaker credit, an MCA funds same day at a higher cost. For larger purchases with time to underwrite, SBA financing wins on rate.

If you're working on a deal right now, we can usually tell you within a few hours whether one of our loans fits your timeline. Apply with Clarify Capital to see your options.

FAQ

Below, I cover the questions business owners ask me most often when they first start looking into quick business loans.

Can You Get a Business Loan Immediately?

Yes, depending on the product. Merchant cash advances and short-term business loans from online lenders can fund the same business day you apply, assuming your credit score, revenue, and bank statements meet the lender's floor. Bank-originated loans and SBA financing take weeks to months, regardless of how urgent your need is.

What Loans Are the Best for Small Business?

The best loan depends on the use case. For one-time cash needs, a short-term business loan or term loan works well. For ongoing flexibility, a business line of credit is the right tool. For asset purchases, equipment financing is purpose-built. For owners with bruised credit and strong revenue, an MCA expands the option set. For lower-rate financing on longer-horizon investments, an SBA loan is hard to beat.

Can I Get a Startup Business Loan With a 500 Credit Score?

Not from most traditional lenders, and not from Clarify until you've been operating for at least six months. Once you've crossed that threshold, our merchant cash advance product approves operators with 500+ credit scores as long as monthly revenue clears $10,000. For true pre-revenue startups with a 500 credit score, the realistic options are SBA Microloans through certified community lenders or personal financing routes.

What Are the Quickest Funding Options for Small Businesses?

Merchant cash advances, short-term business loans, and business lines of credit (after the initial line is established) all fund the same business day for qualifying borrowers. Equipment financing funds in one to five days. Invoice factoring funds in one to two weeks. SBA loans take 30 to 90 days, and bank-originated term loans typically run longer than online options, so neither sits in the "immediate" tier even though they're often the cheapest option over the loan's full life.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts