Small business loan fees can significantly increase the total cost of borrowing, sometimes even more than the advertised interest rate. That's why transparency is crucial when comparing business financing options. Common fees include origination, loan application, closing, maintenance, late payment, and even prepayment penalties, depending on the type of loan and lender.

Each product, whether it's a term loan, SBA loan, or business line of credit, may come with a unique fee structure. These charges can reduce the real value of your loan amount and surprise borrowers if not clearly disclosed up front.

At Clarify Capital, we prioritize full transparency. We never charge application fees or prepayment penalties, and we work with a trusted network of lenders to ensure small business owners understand all costs associated with their financing.

When you know what to look for, you can choose a small business loan that meets your needs without compromising your budget. Clarify Capital is here to help you borrow smarter so you can focus on running and growing your business.

How SBA Loan Fees Work

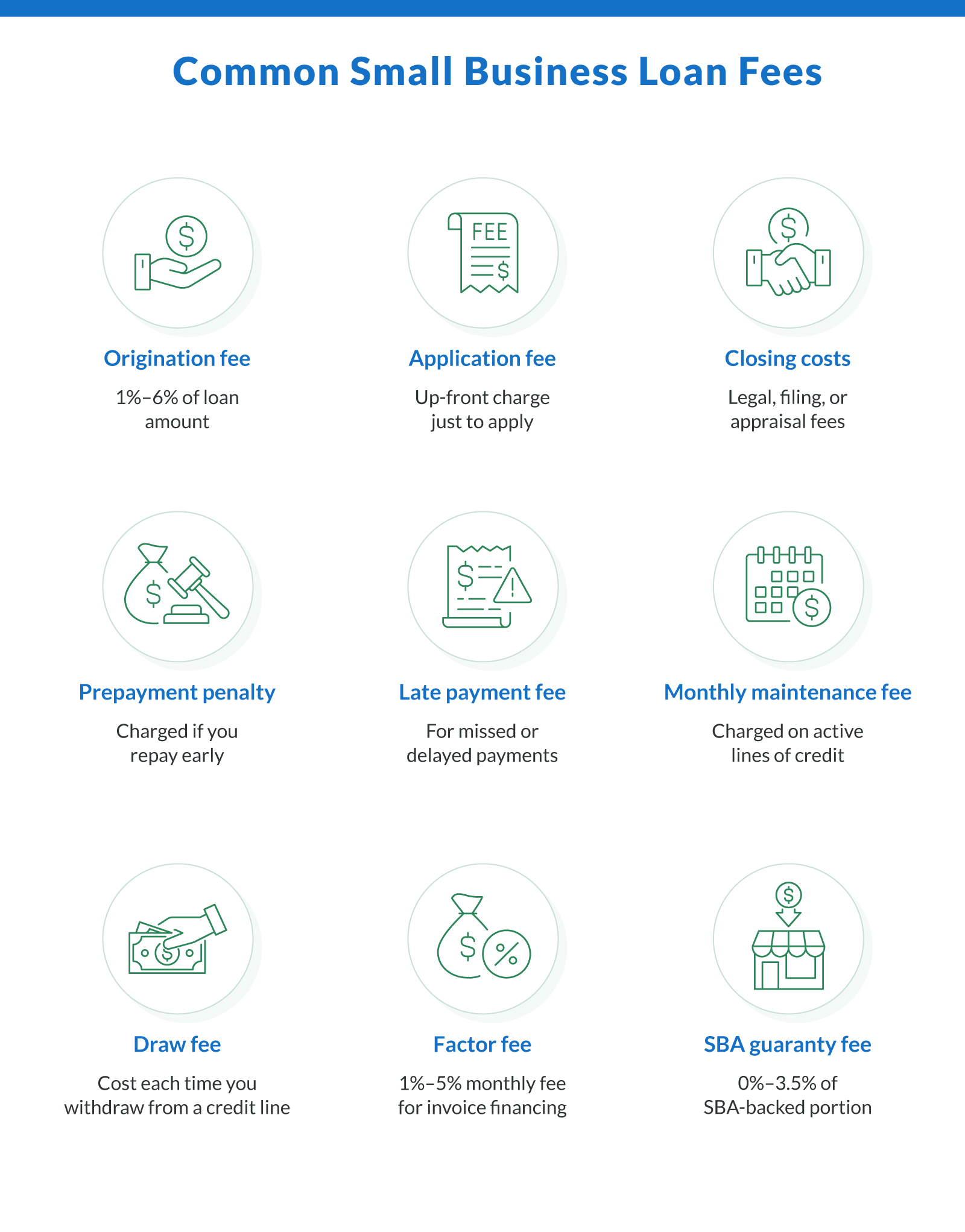

SBA loans, backed by the Small Business Administration, come with a few specific fees that borrowers should understand. One of the most common is the guarantee fee, which typically ranges from 0.25% to 3.75% depending on the loan size. This fee helps the SBA cover its portion of the risk and is often included in the total loan agreement, meaning it can be rolled into the loan amount instead of being paid up front.

In addition to SBA-set fees, lenders may include their own charges, such as an annual fee or packaging fee. However, the SBA caps certain costs to protect borrowers and keep these SBA loan fees manageable.

Despite these added expenses, SBA loans are popular because they usually offer lower interest rates and longer repayment terms compared to traditional options, making them a cost-effective choice for many small businesses. Understanding all terms before signing helps ensure you're getting the full benefit of this government-supported funding.

Common Small Business Loan Fees

Lenders charge fees to cover the cost of processing, underwriting, and servicing a loan. These fees vary depending on the type of loan, such as traditional term loans or business lines of credit. Understanding these costs up front helps you evaluate the total cost of borrowing and avoid surprises after credit approval.

Origination Fees

Origination fees are one of the most common charges in small business lending. They vary but can typically range from 1% to 6% of the loan amount, covering underwriting fees, administrative tasks, and initial loan setup.

While some lenders apply these fees universally, others offer more flexibility. Borrowers working with Clarify Capital's lender network may qualify for waived or reduced origination fees based on their financial profile and loan type.

Being aware of origination fees and how they affect your bottom line allows you to better assess the true cost of financing. Always ask if fees are negotiable, and compare offers to find the most cost-effective option for your business.

Application Fees

An application fee is an up-front fee some lenders charge to review your loan application, even if you're not ultimately approved. These lender charges are meant to cover administrative work but can add unnecessary costs, especially for businesses exploring multiple business financing options.

Clarify Capital does not charge application fees, allowing you to compare funding opportunities without added risk or expense. This fee-free approach helps small businesses to focus on securing the right financing, rather than worrying about initial costs.

Closing Costs

Closing costs are fees commonly associated with secured loans, especially those involving commercial real estate or large equipment purchases. These costs may include UCC filings, property appraisals, attorney fees, and title searches.

Some business lenders also include a service fee as part of closing. While these expenses are often itemized in your loan documents, they can significantly increase the total cost of borrowing. Understanding and planning for these costs is essential when evaluating secured financing options.

Prepayment Penalties

Prepayment penalties are fees charged by a lender if you pay off your small business loan before the end of the agreed repayment term. These fees are meant to compensate lenders for the interest they lose when a loan is repaid early, especially on long loan term agreements.

Clarify Capital believes in flexibility. That's why loans arranged through Clarify come with no prepayment penalties, allowing you to reduce interest costs and pay off your balance on your schedule without extra fees.

Late Payment Fees

Late payment fees are charged by your lender when loan payments are missed or delayed beyond the due date. These business loan fees help protect the lender against risk but can add up quickly, especially if your business is managing tight cash flow.

To avoid these charges, consider setting up autopay or calendar reminders to ensure on-time payments. Staying consistent not only prevents late fees but also helps maintain your financial reputation and creditworthiness.

Monthly Maintenance and Draw Fees

If you're using a business line of credit, be aware that some financing options include ongoing charges like service fees or draw fees. These may be billed as part of your monthly payments or applied each time you withdraw funds from the credit line.

Fees can vary based on your credit limit or annual revenue, and they help cover the lender's cost of keeping the account active. When comparing lines of credit, always check how often fees are applied and whether they impact the total cost of borrowing.

Factor Fees (For Invoice Financing)

Factor fees are charges applied when using invoice financing or merchant cash advances, typically ranging from 1% to 5% per month of the invoice or advance value. These fees are not interest rates but fixed charges that increase the overall loan cost over time.

Used to provide fast access to working capital, factor fees can add up quickly, especially if repayment takes longer than expected. While useful for businesses that don't qualify for a traditional small business loan, it's important to weigh these costs against more affordable funding options when planning your financing strategy.

How To Compare and Avoid Hidden Fees

When evaluating financing options, always compare the annual percentage rate (APR), not just the interest rate. APR includes all business loan fees and gives a more accurate view of the total cost over the loan term. This helps you better understand how loan payments will impact your cash flow.

Ask your lender for an itemized fee breakdown, and carefully review the loan agreement for mentions of service fees, closing costs, or recurring charges. This due diligence ensures you're comparing offers fairly and avoiding unpleasant surprises.

At Clarify Capital, we're committed to full transparency. Our network offers competitive rates with no hidden fees, allowing you to choose the right loan with confidence.

Tips for Reducing Small Business Loan Costs

Keeping your loan costs manageable starts with knowing how to evaluate offers and maintain good financial habits. Whether you're a startup or a growing business seeking working capital, using the right strategies can help you secure lower interest rates and avoid unnecessary fees throughout the repayment term.

Here are some ways to reduce the cost of business lending:

Ask about fee waivers. Some lenders waive origination fees for businesses with a strong credit history or high approval potential.

Compare APRs. Use the annual percentage rate to measure total cost, including fees and business loan interest rates.

Choose lenders with no prepayment penalties. This gives you the flexibility to pay off the loan early and save on interest.

Monitor cash flow. On-time payments help avoid late fees and keep your repayment schedule on track.

Work with transparent providers. Clarify Capital clearly discloses all fees right away, helping you make informed decisions without hidden costs.

Clarify Capital's Transparent Approach to Business Loan Fees

At Clarify Capital, we believe business owners deserve honesty and clarity when exploring business financing. That's why we charge no application fees, no prepayment penalties, and offer full transparency on all loan options before you sign anything.

With a vast network of trusted business lenders, Clarify helps you access flexible terms and competitive rates tailored to your goals. Whether you're comparing business credit cards, term loans, or lines of credit, we're here to help you find financing that fits, without hidden fees or fine print surprises.

Don't let fine print surprise you. When you work with Clarify Capital, we ensure you understand every cost up front — no surprises. Get a quote now.

FAQ About Small Business Loan Fees

Understanding the full cost of a loan is key to making smart financial decisions. This FAQ addresses some of the most common questions borrowers have about small business loan fees, helping you navigate terms, avoid surprises, and compare offers with confidence.

How Much Does It Cost To Get a Small Business Loan?

The loan cost of a small business loan depends on several factors, including the loan amount, interest rate, repayment term, and any additional fees such as origination or closing costs. The total cost increases if your credit report shows limited history or lower scores, which can result in higher rates.

To get a clearer picture, always compare offers using the annual percentage rate (APR), which includes both business loan interest rates and fees, giving you a more complete view of what you'll actually pay over time.

What Are the Current Average Business Loan Interest Rates?

Business loan interest rates vary based on several factors, including your credit score, the lender you choose, and current market conditions. Currently, average rates typically range from 6% to 12% for traditional term loans, depending on the repayment term and the borrower's financial profile.

Rates may be lower for highly qualified borrowers or SBA-backed loans, while riskier profiles may face higher loan costs. Always review the full offer, including fees and structure, to understand your total borrowing expense.

What Is the 20% Rule for SBA?

The 20% rule for SBA loans requires that any individual who owns 20% or more of a business must personally guarantee the loan. This means they agree to repay the loan if the business cannot, adding a layer of security to the SBA guarantee for the lender.

The Small Business Administration includes this requirement in the loan agreement to ensure accountability and reduce risk. If you fall under this rule, be prepared to provide personal financial information as part of the application process.

Can a New LLC Get an SBA Loan?

Yes, a new LLC can qualify for SBA loans, as long as it meets key eligibility requirements such as creditworthiness, projected revenue, and available collateral. While newer businesses and startups may face more scrutiny, they're not excluded from accessing this type of business financing.

To strengthen your loan application, be prepared to submit a detailed business plan, financial projections, and possibly personal guarantees. Demonstrating your LLC's viability can help establish lender confidence and improve your chances of approval.

What Are Typical Terms for a Small Business Loan?

The repayment term for a small business loan depends on the type of loan. Short-term loans generally range from three months to two years, while SBA loans can extend up to 25 years, such as for real estate or equipment financing.

Longer loan terms result in lower monthly payments but increase the total cost due to more interest paid over the life of the loan. To get the clearest picture, use the annual percentage rate (APR) to compare overall affordability between loan options.

Does a Small Business Loan Have a Fixed or Variable Interest Rate?

A fixed interest rate remains constant over the life of the loan, offering predictable payments. In contrast, a variable interest rate can fluctuate based on market conditions, meaning monthly costs may rise or fall.

Most term loans come with a fixed interest rate, making them a good fit for businesses seeking payment stability. On the other hand, a business line of credit usually has a variable interest rate, which can offer flexibility but also more uncertainty. The type of loan product you choose will determine how your business loan interest rates are structured.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts