When selecting the ideal business financing option, small business owners typically compare two popular choices: a business line of credit and a business loan. A business line of credit gives you flexible access to funds you can draw on as needed, while a small business loan provides a lump sum with fixed repayment terms. Each serves a different purpose and offers unique benefits depending on your business needs, cash flow, and funding timeline.

This guide defines both financing options and compares costs, eligibility requirements, and best-fit use cases to support smarter financial decisions.

What Is a Business Loan?

A business loan provides a lump sum of capital up front, which the borrower repays over time through scheduled installments. It's designed for specific business purposes, from purchasing equipment to funding long-term growth.

Each loan type comes with its own loan amount, repayment schedule, interest rate, and documentation requirements. With a lump sum of money paid out up front, clear repayment terms help you plan monthly payments and forecast cash flow.

The following table outlines several common loan types, including traditional, government-backed, and alternative options:

| Types of Business Loans | |||

|---|---|---|---|

| Loan type | Typical loan amount | Typical repayment period | Cost notes |

| Term loan | $25,000– $500,000 | 1 to 10 years | Interest rates vary by lender and credit profile |

| Short-term loans | Varies by lender | 3 months to 2 years | Often has higher interest rates due to a shorter repayment window |

| SBA loan | Up to $5 million | 5 to 25 years | Rates vary by program and lender, with SBA caps and market-based pricing |

| Equipment financing | Up to 100% of the cost | 1 to 10 years | APR may start around 6%, but terms depend on the lender and equipment |

| Microloan | $500–$50,000 | Up to 7 years | Interest rates are generally between 8% and 13% (varies by intermediary) |

| Merchant cash advance | Varies by revenue | Based on sales receipts | Factor rates replace traditional APR interest rates |

| Commercial real estate | $100,000–$5 million | 5 to 25 years | Rates vary by lender and structure, with longer terms common for real estate |

Best Uses for Business Loans

Business loans are best for large-scale investments that require up-front capital and deliver returns over time. Common use cases include:

Expansion and remodeling. A loan can cover one-time expenses like opening a new location, renovating a workspace, or adding capacity so you can take on more work.

Buying real estate. Long-term commercial property investments align well with fixed repayment terms.

High-cost projects. Loans support endeavors with high up-front costs that may take time to generate revenue.

What Is a Business Line of Credit?

A business line of credit is a flexible form of revolving credit that lets businesses draw funds as needed up to a set limit and approved credit limit. Unlike a loan, you only pay interest on the amount you use.

This type of financing is often used to manage short-term cash flow gaps or cover operating costs. Lines of credit may be secured or unsecured, and interest rates can vary based on your creditworthiness and lender policies.

Small businesses that deal with seasonal revenue, inventory restocking, or unexpected expenses often benefit the most. It offers ongoing access to working capital while helping separate business and personal expenses. It also supports building your business credit history.

Secured vs. Unsecured Lines of Credit

Business lines of credit come in two main types, each with distinct approval processes and risk profiles:

Secured line of credit. Requires collateral, such as equipment or inventory. Usually offers lower interest rates, but you could lose the collateral if you default.

Unsecured line of credit. Does not require collateral. An unsecured line of credit is often faster to access, but it may come with higher interest rates depending on your creditworthiness.

Lenders often evaluate your credit score, cash flow, and business performance to determine eligibility. Providers can include banks, credit unions, and other financial institutions.

Best Uses for a Business Line of Credit

A line of credit is ideal when you need ongoing access to capital without committing to a full loan. It's well-suited for:

Working capital needs. Smooth out cash flow dips, especially during slow seasons.

Growth expenses. Cover inventory for a new retail partnership, ramp up marketing during an expansion, or handle up-front costs tied to a new contract.

Emergencies and repairs. Access quick funds for urgent but essential fixes.

How a Business Line of Credit Works

Getting a business line of credit is a straightforward process, but careful preparation can improve your approval odds and help you secure better terms. From application to repayment, the goal is simple: get flexible working capital without borrowing more than you need.

Apply and Share Key Documents

Before applying, gather essential documents and business details, including:

Business financials. Recent profit and loss statements, balance sheets, and revenue summaries.

Bank statements. Clarify Capital requires your last three months of business banking history.

Identification. Valid government-issued ID for verification.

Checking account details. A business checking account supports business banking verification and helps confirm cash flow.

Clarify Capital's online application takes just two minutes to complete. To avoid delays, double-check your information for accuracy and ensure all required fields are filled.

Complete the Credit and Income Review

Once submitted, your application goes through a credit review process. Lenders evaluate your:

Credit score. Many lenders look for a minimum score of 550 is required for same-day funding.

Revenue. You must earn at least $10,000 in monthly revenue.

Debt obligations. Existing loans or credit lines may impact approval odds.

Your credit history and business banking activity help the lender confirm income patterns and set terms.

Receive Your Offer and Set Your Credit Limit

If approved, you'll receive a personalized credit limit offer based on revenue trends and cash flow, credit history and payment track record, and business age and stability.

Review the terms closely, especially interest rates, draw fees (if any), and repayment details, before accepting. Once accepted, you gain revolving credit access immediately.

Draw Funds, Then Repay and Reuse

Draw funds up to your approved limit whenever necessary. Many borrowers can access funds the same day they're requested, depending on the lender's processing timelines.

You're only charged interest on the funds you draw, not the full credit line. Repayment typically involves minimum monthly payments based on the outstanding balance or fixed weekly/monthly schedules, with early repayment options that can reduce interest costs. As you repay, your available credit replenishes, so you can keep using the line when new expenses come up.

Key Differences Between a Business Loan and a Business Line of Credit

Here's a side-by-side comparison to highlight the core differences between business loans and lines of credit so you can select the right tool for your business's financial strategy:

| Business Loans vs. Business Lines of Credit | |||

|---|---|---|---|

| Funding method | When you pay Interest | Repayment style | Best for |

| Business loan | Interest applies to the full amount, often at a fixed interest rate | Fixed installments on the full amount | Lump sum funding for planned, longer-term needs |

| Business line of credit | Interest applies only to what you draw. Rates may be fixed or variable depending on the lender and product. | Pay only on the drawn amount, revolving | Flexible access up to a credit limit for short-term needs |

Benefits and Drawbacks

Each financing option has its strengths and challenges. Below are some key pros and cons to consider:

Business loans offer predictability. Fixed monthly payments support cash flow planning, and term loans may offer lower interest rates than revolving credit in many cases.

Business lines of credit provide flexibility. They work well for variable or recurring expenses, but unsecured credit lines can come with higher interest rates and require more active balance management.

Choices by Industry

Financing preferences often reflect the specific demands of each industry. Here's how different sectors typically choose:

Retail and e-commerce. Lines of credit can help cover inventory swings and short-term cash flow changes.

Construction and health care. Loans often fit better for equipment purchases or larger project costs with a clear timeline.

Real estate. Business loans are commonly used for capital-intensive real estate projects with longer repayment terms.

Cost Structure Comparison

Understanding how each financing option charges interest and fees can help you choose the most cost-effective solution:

| Cost and repayment snapshot | ||

|---|---|---|

| Product | Typical fees | How interest is charged |

| Business loan | Origination fees (often 1%–5%) are paid up front | Interest is typically charged on the full loan amount (often at a fixed interest rate) |

| Business line of credit | Possible maintenance fees plus a draw fee each time you borrow | Interest only accrues on what you draw, often with variable interest rates |

Business loans typically feature fixed interest rates, which offer predictable payments. Origination fees usually range from 1% to 5% of the total loan amount. Repayment starts immediately and follows a set schedule.

Business lines of credit often come with variable interest rates, which can fluctuate over time. Lenders may charge maintenance fees monthly or annually to keep the line open. Each withdrawal may also trigger a draw fee — a small percentage of the amount borrowed. Interest only accrues on the funds used.

Hidden Costs To Watch For

Even low-interest products can carry significant hidden fees. Origination fees, though one-time payments, can add to your overall loan total, while maintenance fees can be charged on open credit lines — even if they're unused. Late payments, or even early payments, may also trigger other fees that can add up quickly.

Example: A $50,000 loan with a 3% origination fee adds $1,500 up front before interest is factored in. Total interest cost depends on the rate and term you choose.

To reduce costs, ask for full fee disclosures. When comparing loan options, it's also important to make payments on time and pay off high-interest debt quickly.

Eligibility and Approval Factors

Qualifying for business financing depends on a few key requirements. Here's what lenders look for:

A 550+ credit score for Clarify Capital; higher scores improve terms

Annual revenue of at least $10,000 per month

At least six months of business history

Business bank account

Three months of bank statements, business details, and ID

Some lenders require collateral

Industry type also plays a role. High-risk sectors may face more scrutiny or limited offers. As a quick credibility check, a bank or credit union may list "Member FDIC," while some lenders and brokers display an NMLS ID.

How To Improve Your Approval Odds

You can boost your chances of approval with the following steps:

Raise your credit score. Pay down balances, reduce utilization, and correct credit report errors.

Prepare updated financials. Keep current profit and loss statements and bank records ready.

Plan ahead. Improvements can take three to six months, so avoid waiting until funds are urgent.

Common Application Mistakes To Avoid

Many business owners unintentionally delay or damage their approval chances. Avoid these common errors:

Incomplete documentation. Missing bank statements or ID slows down the process.

Inaccurate revenue reporting. It can lead to misaligned offers or delays.

Overlooking terms. Accepting financing without understanding fees or repayment terms can backfire.

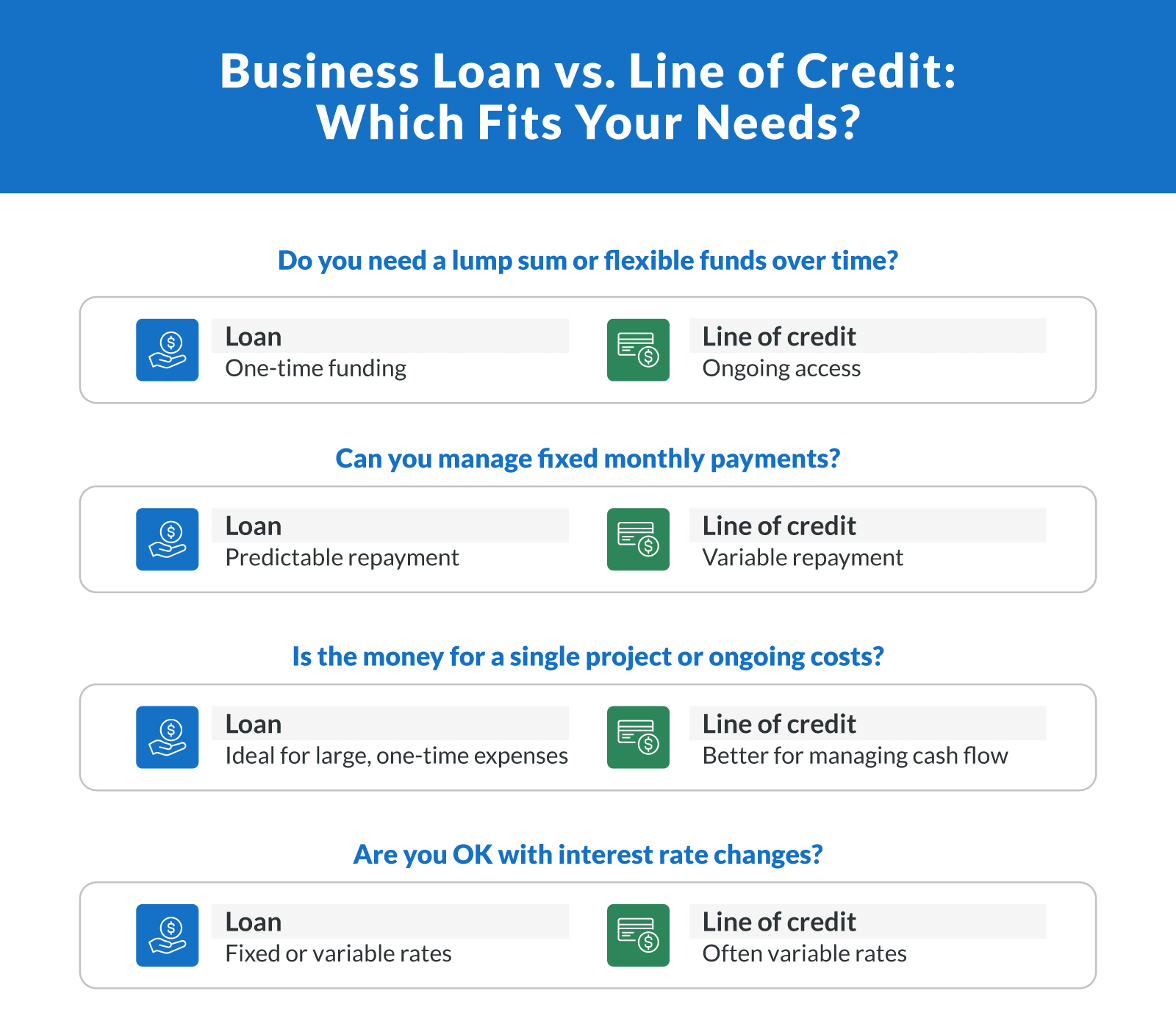

How To Choose Between a Business Loan and a Business Line of Credit

The best business financing choice depends on your business needs, cash flow, and how you want repayment to feel month to month. The following questions can help guide your decision:

Do I need a specific amount of money all at once, or flexible access over time?

Can my business handle fixed monthly payments, or is variable repayment more manageable?

Is this funding for a one-time project or recurring operating costs?

How quickly do I need access to funds?

Am I comfortable with the interest rate variability of a credit line?

Do I have documentation and revenue history that will meet approval requirements?

How To Choose: Ongoing vs. One-Time Needs

Choosing the right option often comes down to whether you need it for:

One-time expenses: Start with a business loan or term loan. It fits planned costs like an equipment upgrade, a second location buildout, or a real estate purchase when you want fixed installments and clear repayment terms.

Ongoing access: Start with a business line of credit. It fits working capital needs like ramping payroll for a new contract, covering inventory purchases, or smoothing short-term gaps while revenue catches up.

If you're still deciding, the factors below can help narrow the choice based on repayment structure, interest rates, and term length:

Predictable monthly payments: Lean toward a loan.

Flexible repayment: Lean toward a line of credit.

Fixed interest rate: Lean toward a loan.

Variable interest rates and fluctuations: Lean toward a line of credit.

Longer repayment terms: Compare SBA loans if you qualify.

Ready to compare your options based on your cash flow and timeline? Apply today to see what you may qualify for.

Use Cases by Business Stage

As businesses evolve, so do their financing needs. The right funding option often depends on your business's stage of maturity — whether you're navigating early growth, managing seasonal demand, or scaling operations.

| Funding Options by Business Stage | ||

|---|---|---|

| Business stage | Typical needs | Recommended product |

| Newer business (6+ months) | Working capital, basic inventory, marketing spend | Microloans, business credit cards |

| Growth phase | Hiring, adding shifts, scaling marketing with measured ROI, and equipment upgrades | Term loans, lines of credit |

| Seasonal business | Inventory purchases, payroll, and operating costs | Business line of credit, short-term loans |

| Established business | Real estate, acquisitions, long-term projects | SBA loans, commercial real estate loans |

Clarify Capital does not fund startup businesses. Newer businesses with at least six months of revenue history may still qualify for smaller funding options, such as business credit cards or microloans, especially if they meet minimum revenue and time-in-business thresholds.

As businesses move into the growth phase, funding needs become more complex. In these cases, term loans offer structured support, while a business line of credit can offer needed flexibility.

Seasonal businesses often require fast access to funds for peak inventory or staffing needs. A credit line enables draw-as-needed flexibility without overcommitting on interest-bearing debt.

Established businesses, by contrast, often leverage long-term capital for real estate purchases or acquisitions. With a solid track record and strong financials, they can access larger loan amounts, lower interest rates, and longer installments.

Alternatives to Business Loans and Lines of Credit

In some cases, neither a traditional loan option nor a line of credit may be the best fit. Businesses with unique circumstances, cash flow patterns, or short-term capital needs may benefit from other options that serve a specific purpose.

Business Credit Card

For smaller recurring purchases, a business credit card can be a simple option for day-to-day business expenses. Unlike personal finance cards, it can help separate business spending and may support business credit building.

Pros: Fast access for smaller purchases and useful for recurring expenses.

Cons: Rates can be high if you carry a balance. However, limits may not cover larger projects.

Invoice Factoring

Invoice factoring lets you sell outstanding invoices to a third party in exchange for immediate cash. It's often used when customer payments are delayed.

Pros: Improves short-term cash flow, but can be quicker than a loan.

Cons: Fees can add up, and collections may affect client relationships.

Crowdfunding

Crowdfunding raises money from many people through an online platform, often through reward-based, equity-based, or donation-based campaigns.

Pros: No repayment required for rewards/donations, and can double as marketing.

Cons: Results vary, and campaigns often take time to plan and run.

Small Business Grants

Small business grants are non-repayable funds awarded by government agencies or private organizations. They're competitive and usually tied to specific goals or eligibility rules.

Pros: No repayment and no equity loss.

Cons: Long application cycles with strict requirements and heavy competition.

Choosing the Right Option for Your Business

Deciding between a business loan, a business line of credit, or an alternative funding method comes down to how each one fits your goals, revenue model, and cash flow needs. Loans offer a fixed structure for planned, larger expenses, while lines of credit give you more control over timing and draw amounts. Use the decision framework above to match the product to your funding timeline and comfort level with repayment.

For personalized guidance or to explore funding tailored to your needs, apply today with Clarify Capital.

FAQs About a Line of Credit vs. Business Loan

If you're weighing these financing options, here are quick answers to the most common questions small business owners ask.

What's Better, a Loan or a Line of Credit?

A loan fits one-time expenses where you want a lump sum and fixed installments. A line of credit works better for ongoing access to working capital and short-term cash flow gaps.

What Is the Monthly Payment on a $50,000 Business Loan?

It depends on the interest rate and repayment terms. Your lender can quote an exact payment, but a shorter term or higher rate increases monthly payments.

Is It Better To Get a Bank Loan or a Line of Credit?

A bank loan can offer lower interest rates for strong credit and stable revenue. A line of credit may be easier to use for fluctuating expenses, but rates are often variable.

How Does Paying Back a Business Line of Credit Work?

You repay what you draw, plus interest and any fees. Many lenders require minimum monthly payments, and as you repay, your available credit replenishes.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts