Many lenders offer million-dollar business loans, but your likelihood of qualifying depends on the type of lender, your business's financial status, and more. We'll show you strategic ways to stand out from other borrowers.

From expanding a restaurant across new locations to investing in heavy construction equipment, running a business isn't cheap. Securing a $1 million business loan may sound hefty, but many business owners need that amount and more.

Fortunately, many lenders are willing to loan millions to business owners. Applying for a large loan amount, however, requires careful planning, substantial revenue, and a strategic approach.

In this guide, we'll show you how to successfully obtain a million-dollar loan, including key steps to increase your borrowing chances.

1. Assess Your Financing Needs

Good cash flow management will take care of day-to-day operations, but a large amount of capital can go a long way when it comes to scaling your business. Consider the investments and assets that take your business to the next level.

With a seven-figure loan, you can:

Renovate and/or expand into new locations

Purchase equipment and technology

Build an emergency fund

Invest in marketing campaigns

Buy inventory in bulk

Before applying for a loan, assess what revenue-driving factors you need in different areas of your business. This way, you can determine how much funding you need and plan how to use the loan.

To qualify for a million-dollar business loan in 2026, most lenders expect your business to demonstrate high and predictable income. A clear funding plan backed by cash flow projections or existing contracts can help justify the loan amount and make lenders more confident in your request.

Many lenders often look for annual revenue in the $1 million to $5 million range for seven‑figure loans, especially if the business is less than five years old. If you're not generating this level of revenue yet, identifying exactly how the funds will generate ROI, such as acquiring equipment that increases output or opening locations with existing demand, can strengthen your application.

Adding this level of detail to your financing plan helps you stand out from other borrowers competing for large loan approvals.

2. Compare Lenders

There's no one-size-fits-all approach when choosing a lender. It's important to research and identify lenders who provide large business loans and have a history of working with businesses in your industry.

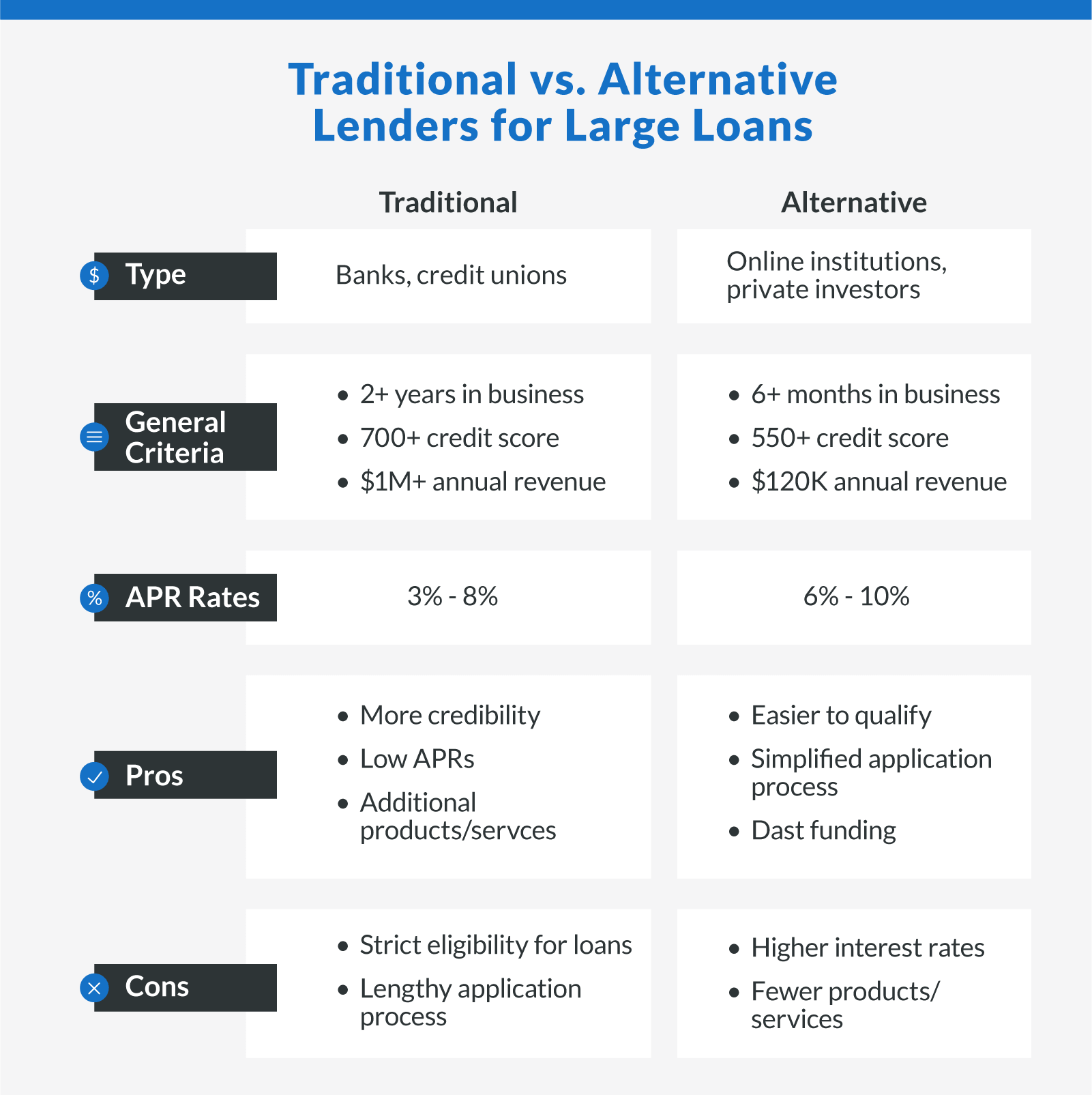

Small businesses typically have two main choices of lenders: traditional banks and alternative lenders. Let's look at their differences to determine which best suits your business.

Traditional Lenders

Banks and credit unions are known as the traditional "go-to" lenders, with most having local brick-and-mortar branches in your town. In addition to business loans, these financial institutions offer a wide range of financing products, such as business credit cards and merchant services, as well as discounts within their loan programs.

You can expect bank and credit union loans to have lower annual percentage rates (APRs) and flexible repayment terms. As for drawbacks, traditional lenders tend to have strict lending requirements, such as excellent credit scores and high annual revenue. They also charge various fees and have a lengthy loan application process.

In 2026, traditional lender interest rates typically range from 7% to 12% for well-qualified borrowers, depending on the loan type, collateral, and term length.

Alternative Lenders

Outside of banks and credit unions, there are online and private financial institutions. These alternative lenders generally work with small businesses, especially those turned down by banks, and offer simpler loan applications entirely online. They also have more flexible borrowing criteria than banks, such as lower credit scores.

You can expect alternative lenders, especially online lenders, to have a more streamlined application process and quicker disbursement of funds. The only downside is higher interest rates since alternative lenders are generally taking on more risk.

Today, online lenders may offer large loan amounts with faster approval, sometimes in just 24 to 72 hours. But interest rates often range from 9% for highly qualified applicants to 20% or higher, especially if your credit profile is below prime.

Clarify Capital works with both traditional and alternative lenders, giving small business owners access to more than 75 providers who fund loans up to $5 million. Your dedicated Clarify advisor helps you compare loan types and choose the most affordable financing for your business goals.

3. Determine Your Eligibility

Before approaching lenders, thoroughly assess your borrowing eligibility. Understand that a $1 million business loan will most likely have more stringent borrowing criteria. Lenders will review both your credit score and credit history, including payment patterns, delinquencies, and existing debt.

While application requirements vary by the lender, many lenders review the following factors:

Credit score: At least 550

Time in business: At least six months

Annual revenue: Over $1M+

If your business doesn't meet this criteria yet, it's still possible to qualify for a million-dollar loan. This is where strategic planning enters.

Ways To Boost Your Chances of Approval

A strong credit profile can significantly enhance your loan approval odds. You'll want to address any outstanding issues on your credit report, pay off existing debt, and make on-time payments to other loans to boost your credit score.

Additionally, offering a personal guarantee or collateral — high-value equipment and business assets — can significantly increase your chances of loan approval. Since many lenders already require collateral to mitigate the financial risk, offering it to one who doesn't can make you a favorable borrower.

Keep in mind that while some lenders may approve $1 million loans with monthly revenue as low as $50,000, most prefer to see annual revenue near or above $1 million, especially if you're requesting unsecured funding.

Other factors lenders may assess include:

Business plan strength. Does it clearly show how you'll use the funds to drive revenue or ROI?

Debt-to-income ratio. If your business is already highly leveraged, that may hurt your chances.

Industry type. Lenders may view businesses in high-risk or seasonal industries differently.

Your Clarify Capital advisor can walk you through eligibility requirements and recommend loan options based on your business's financial profile and goals.

4. Prepare Your Business Documentation

The process of applying for a business loan will vary depending on the lender, but most of them still require a significant amount of documentation, especially to get approved for $1 million. You'll most likely need to gather:

Credit reports. Both personal and business credit scores help lenders assess your creditworthiness.

Tax returns. Provide at least two years of personal and business tax returns to verify income and profitability.

Business bank statements. These help lenders evaluate your cash flow, average balances, and consistency of deposits.

Balance sheets or accounts receivable. Show your assets, liabilities, and the strength of your balance sheet.

A solid business plan. Detail your growth strategies, how you'll use the loan, and projected revenue or cost savings.

Any applicable business licenses, certifications, and registrations. These confirm your business is legally authorized and compliant.

Some lenders may also request financial statements prepared by a CPA, including profit and loss (P&L) statements, especially for loan amounts over $1 million.

To streamline the approval process, Clarify Capital helps you gather and organize all necessary documents. Your dedicated advisor will walk you through exactly what's needed based on the lender's requirements and the type of loan you're pursuing.

Having your documentation in order upfront can help speed up the approval timeline, especially when applying through online lenders that offer faster funding options.

5. Apply and Submit Your Application

After gathering all of the necessary paperwork, you can complete the loan application. Some lenders allow you to submit everything online, but some traditional lenders, such as banks, may require you to visit a local branch in person.

After submission, you're officially in the waiting period. While waiting for approval can take up to a few weeks for traditional lenders, most online lenders can guarantee a loan decision within a few business days.

Once approved, your lender will send you the loan agreement to review, outlining the total amount, your interest rate, monthly payment, and any additional fees. After signing the agreement, your lender will disburse the loan.

With Clarify Capital, the application process is simple and fast. You can apply online in just two minutes, and your dedicated advisor will match you with lenders based on your business's unique profile. Once approved, you can receive funding in as little as 24 hours.

If you're applying for a $1 million loan, be prepared to respond quickly to lender questions and provide any follow-up documentation. Staying responsive can help avoid delays and speed up your approval.

Types of $1 Million Business Loans

Several types of business loans have limits of over $1 million. Depending on your eligibility, here are a few from which you can choose:

| Types of $1 Million Business Loans | |||

|---|---|---|---|

| Loan type | Overview | Max. limit | Min. credit score |

| SBA 7(a) | Government-backed loan; flexible terms and low interest rates | $5 million | 640 |

| Working capital | Short-term loan for any business, credit score decides interest rate | $5 million | 500 |

| Business line of credit | Revolving credit line with preset limit; interest on borrowed funds | $5 million | No minimum (varies by lender) |

| Equipment financing | Loan for equipment based on their value, assets are leverage | Asset value | 500 |

| Term loan | Traditional loan based on business revenue; set repayments | $5 million | No minimum (varies by lender) |

SBA 7(a) Loan

A Small Business Administration 7(a) loan is a government-backed loan that offers up to $5 million. 7(a) loans tend to provide more favorable terms and lower interest rates for business owners seeking substantial funding, generally those with a 640 or higher credit score.

Clarify Capital works with SBA lenders nationwide who specialize in large loans for growing businesses.

Working Capital

A type of short-term financing loan of up to $5 million that businesses can take out to cover daily operating expenses, cash flow gaps, and more. This loan is easily accessible for businesses of different sizes and types, where your credit score determines your interest rate. If you're not ready for a $1 million loan today, consider starting with a smaller loan and refinancing once your revenue and credit profile improve.

Business Line of Credit

A revolving credit line with a preapproved limit of up to $5 million, high approval rates, and no prepayment penalties. With lines of credit, you only pay interest on the amount you borrow.

Equipment Financing

An asset-based loan of up to 100% of the equipment or asset's value, which can cost millions. This financing option is good to utilize if you have quality assets to leverage.

Term Loan

A traditional loan that you can borrow up to $5 million with up to two years of repayment if short-term. A business term loan offers a lump sum of capital with set repayment terms, typically between one and 10 years. Eligibility is purely based on your cash flow, such as having six months of bank statements to prove substantial revenue. You may be able to choose between fixed-rate or variable-rate terms depending on your lender and credit profile. Variable-rate loans may start with a lower interest rate, but monthly payments can increase over time depending on market conditions. This structure is more common with lines of credit or short-term loans.

Secure up to $5 Million Through Clarify Capital

It can take a lot of time and planning to secure $1 million in financing. Fortunately, with the right lender, you can avoid jumping through hoops.

Clarify Capital has more lenient eligibility for small businesses and faster approval. We team with our 75+ network of lenders to secure the best loan option for your industry and business needs.

Frequently Asked Questions

We answer common questions about $1 million business loans.

What Are the Disadvantages of a Million-Dollar Loan?

The downside of having a million-dollar loan is that your business will take on a lot of debt with a large amount of interest to repay. Large business loans also usually require collateral or personal guarantees, which can put your business at risk if you default on payments.

Additionally, repayment terms for larger loans are typically longer, meaning you'll carry the debt on your books for years. It's important to weigh the long-term financial impact alongside the immediate growth opportunity.

Can I Get a Million-Dollar Business Loan With Bad Credit?

Acquiring a business loan with bad credit is possible, but not likely. Most business loans of a substantial amount require excellent credit as well as other factors. However, several types of business loans for bad credit, including business lines of credit and equipment loans, don't rely on credit scores.

If your credit score is below 600, you may still qualify by offering collateral, showing strong cash flow, or applying with a co-signer. Clarify Capital works with lenders who consider the full picture, not just a good credit score.

What Is the Monthly Payment of a $1 Million Business Loan?

The monthly payments of a million-dollar loan will depend on the term length, interest rate, and any additional loan fees. If calculating loan repayments based on the average term length (three to 10 years) and average interest rates (6%-12%), monthly payments can range from under $11,000 to over $33,000 per month.

Here are a few examples:

$1M loan at 8% for 10 years → ~$12,100/month

$1M loan at 10% for 7 years → ~$16,600/month

$1M loan at 12% for 5 years → ~$22,200/month

Use these as general estimates — exact numbers will depend on your lender, rate, and fees.

Do All $1 Million Business Loans Require Collateral?

While some lenders offer unsecured loans for large amounts, it is rare. Most substantially large loans for a small business are secured with collateral or a personal guarantee to offset the risk for lenders.

Offering collateral, like equipment, inventory, or accounts receivable, can also help lower your interest rate and improve your chances of approval.

How Much Revenue Do I Need To Qualify for a $1 Million Loan?

Most lenders prefer to see $1 million or more in annual revenue for seven-figure loans. Some may approve lower-revenue businesses if other factors, like high margins, strong credit, or collateral, are present.

Can Startups Get a $1 Million Business Loan?

Startups may find it difficult to qualify for $1 million in funding unless they have strong financial backing, collateral, or significant contracts in place. However, Clarify Capital can help newer businesses explore creative business financing solutions, such as combining equipment financing with a working capital loan, to meet their funding needs.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts