From covering day-to-day expenses to funding expansions, a small business loan can provide the business financing you need to stay competitive and grow. But between choosing a lender, comparing loan programs, and submitting financial documents, the process takes preparation. Below, I'll break down how to apply for a business loan step by step, including how to speed up approval, what documents you'll need, and common mistakes that delay funding.

Step 1: Choose the Right Type of Business Loan

Businesses can choose from several loan options depending on their financial needs, timeline, and qualifications, including the following:

Term loan. A lump sum paid back in monthly payments with fixed interest, great for larger expenses or one-time needs.

Business line of credit. Revolving credit you draw from as needed for short-term needs. You only pay interest on the amount used.

Small Business Administration (SBA) loan. Government-backed, low-interest loans with longer terms. Ideal for established businesses with strong credit.

Working capital loan. Quick funding that's ideal for managing operating costs like payroll, inventory, or rent.

Equipment financing. Loans meant to help you purchase or lease business equipment; good for businesses that need machinery, vehicles, or technology but want to preserve working capital.

Merchant cash advance. Fast financing based on future sales, typically with higher interest rates. Good for businesses with strong card sales that need quick cash and can't qualify for conventional financing.

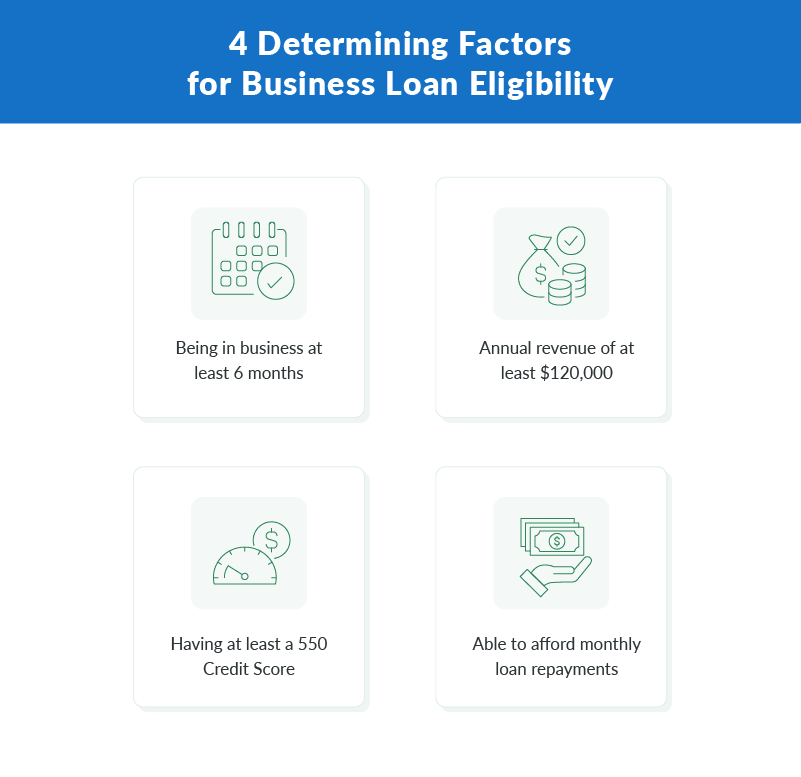

Step 2: Determine Your Eligibility

Lenders want to assess your business's ability to repay. Meeting the minimum criteria will improve your chances.

Lenders evaluate several core eligibility requirements to determine if your business qualifies for funding:

Time in business. Most lenders require at least six months of operations, so keep this in mind if the loan is for a new business or startup.

Annual revenue. A minimum of $120,000 annually ($10,000 monthly) is common.

Credit score. A 550+ personal credit score is typically needed, though some online lenders accept lower.

Ability to repay. Required for verifying deposits and cash flow.

Clarify Capital's eligibility: $10K in monthly revenue, six or more months in business, and a 550+ credit score.

Step 3: Compare Potential Lenders

Before applying, take time to compare the following lender types. Each offers distinct advantages based on your business needs and qualifications:

Traditional banks. Lower interest but a slower process. Best for high-credit borrowers.

SBA-approved lenders. Ideal for long-term financing with low APRs.

Online business lending. Online lenders offer fast funding and lower documentation. Clarify offers loan amounts up to $5M with APRs from 6%.

Credit unions. Member-only banking products with competitive rates, but more paperwork.

Step 4: Gather and Prepare Required Documents

Having your documents ready streamlines the application process and shows lenders your business is organized and loan-ready.

Business info. EIN, legal name, address, and contact info.

Financial statements. Profit and loss, balance sheet, cash flow statement.

Tax returns. One to two years of business and possibly personal returns.

Bank statements. At least three to four recent months to verify cash flow.

Business plan. Optional, but helpful to explain how you'll use the loan.

See our small business loan document checklist for a complete list.

Step 5: Complete and Submit Your Application

Once you've chosen a lender, fill out the application accurately to avoid rework. Lenders typically ask for your:

Business name, EIN, and contact details

Loan amount requested and business purpose

Monthly revenue and time in business

Business checking account details

Clarify Capital provides a two-minute online application. A loan advisor will follow up quickly.

Step 6: Review Your Loan Agreement and Accept Funding

The approval process can take anywhere from 24 hours to a few days, depending on the lender. Before signing, carefully review the loan terms to understand the full cost and repayment obligations:

Interest rate and APR. Confirm whether it's a fixed rate or variable rate.

Repayment terms. Terms may include monthly payments, term length, and total cost.

Origination fees or prepayment penalties. Watch for added charges.

After signing, funds are typically deposited within one to two business days.

What Slows Business Loan Applications

Avoid these common roadblocks that can delay loan approval or reduce your loan offer:

Missing documents. These may include incomplete tax returns, outdated bank statements, or skipped application fields.

Inconsistent cash flow. Unstable revenue can affect credit approval.

Low credit score. Improving personal credit helps you qualify for lower interest rates.

Unclear loan purpose. Lenders want to see a clear plan for how you'll use the funds.

Move Forward With Confidence

With a little planning, getting a small business loan can be fast and stress-free. Start by choosing the right type of financing, then prepare the documents that show your business is ready to borrow. Comparing providers can help you find better rates and faster approval timelines. And if you're working with Clarify Capital, your dedicated advisor will guide you through every step.

Apply today to get loan offers tailored to your goals. There's no obligation, no pressure, and no impact on your credit score.

FAQ About Applying for a Business Loan

Still have questions? Here are quick answers to the most common concerns I hear about getting a small business loan.

Who Can Apply for Small Business Loans?

Any small business owners can apply for a loan, but the business must qualify under SBA loan standards and meet the criteria of the lender.

Can I Get a Business Loan With Bad Credit?

Yes. Some lenders offer financing options for borrowers with personal credit scores under 600. Expect shorter terms or higher APRs.

Can I Apply for a Loan With No Down Payment?

Yes. Many loans, including working capital loans and credit lines, don't require down payments.

Do I Need Collateral?

Not always. Many online loans are unsecured, meaning you don't have to offer personal or business assets to qualify.

How Fast Can I Get Funded?

Clarify Capital offers same-day approval and funding. Most online lenders fund within 24 to 72 hours.

What Loan Fees Should I Expect?

Common fees include an origination fee (1% to 6%), underwriting costs, and possible prepayment charges. These are often included in your APR.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts