About 71% of small businesses carry some form of debt, and roughly 27% of business owners seeking financing do so specifically to refinance or pay down existing obligations. If you're carrying business debt that no longer fits your financial picture, two strategies come up most often: refinancing and consolidation.

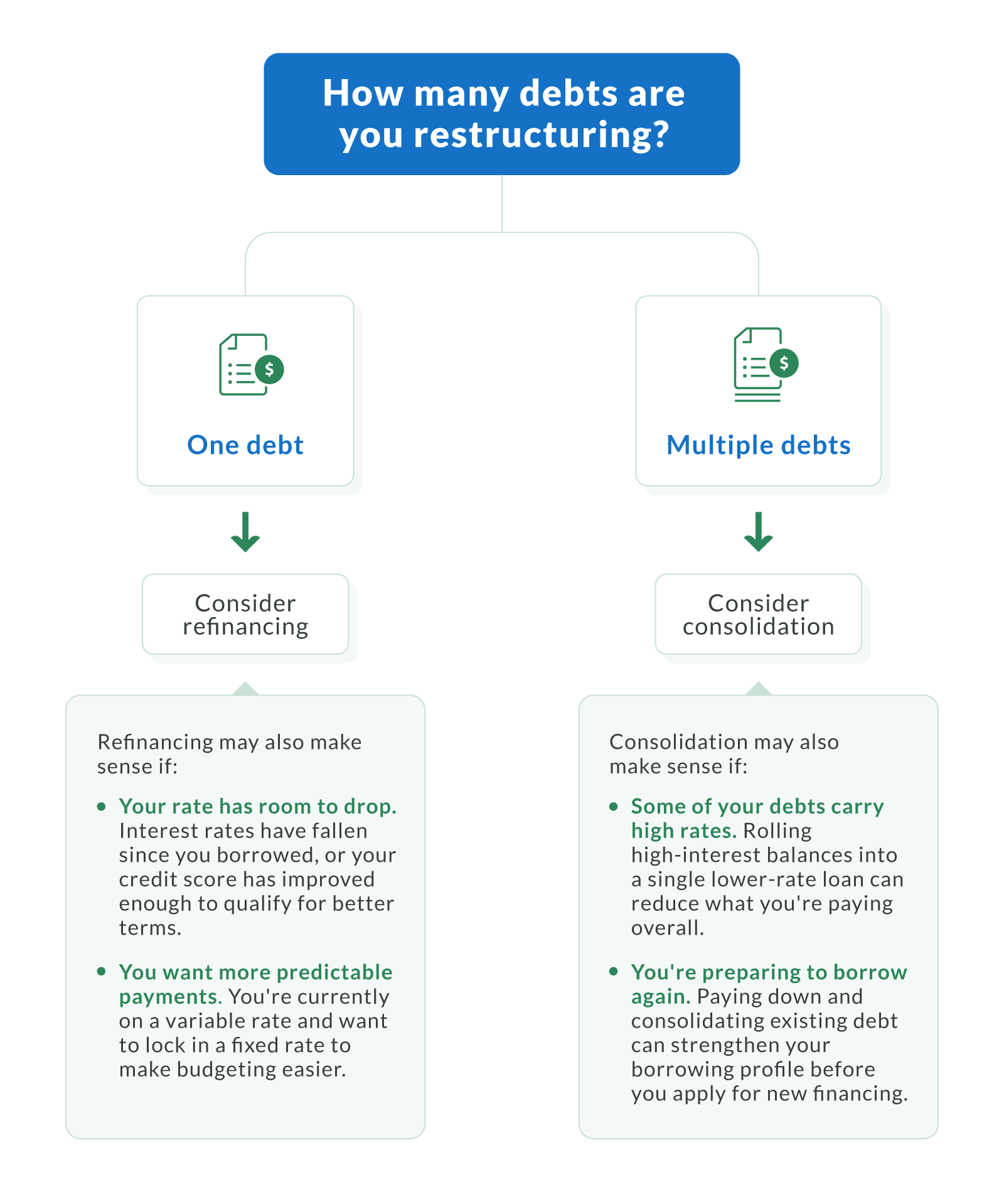

Refinancing replaces a single loan with a new one at a lower interest rate or better terms. Consolidation rolls multiple debts into one loan with one monthly payment. Refinancing tends to work best when you have one loan, and you want to reduce your rate or adjust your repayment period. Consolidation makes more sense when you're juggling several debts and need to simplify your cash flow.

With the Fed cutting rates six times since September 2024, many business owners are sitting on loans priced at the peak. Here, I'll show you how these two options compare and when each one makes sense.

| Debt Refinancing vs. Consolidation | ||

|---|---|---|

| Factor | Refinancing | Consolidation |

| Goal | Secure a better interest rate or new terms on a single loan | Combine multiple debts into one loan with one payment |

| Number of loans | Replaces one existing loan | Replaces multiple existing debts |

| Interest rate impact | Can lock in a lower fixed or variable rate based on current market | New rate may reflect a weighted average, or drop if creditworthiness improved |

| Best for | A borrower with one high-rate loan who wants better terms | A borrower managing multiple debts who wants a simpler cash flow |

| Credit impact | Hard inquiry; old account closes, new one opens | Hard inquiry; may improve debt-to-income ratio |

| Typical timeline | One to four weeks (bank); as fast as 24 to 48 hours (online lender) | One to four weeks (bank); as fast as 24 to 48 hours (online lender) |

What Is Business Debt Refinancing?

Refinancing means replacing an existing loan with a new loan that has better terms. That might mean a lower interest rate, a switch from a variable rate to a fixed interest rate, or a different repayment period that better fits your cash flow. I see business owners pursue refinancing most often when market rates drop or their credit profile improves enough to qualify for something better than they originally locked in.

How Refinancing Works

The process is fairly straightforward:

Review your current loan terms. Pull up your existing agreement and note your interest rate, remaining balance, repayment period, and any prepayment penalties.

Check your credit score. Lenders will pull your credit report, so know where you stand before applying. A higher score gives you leverage to negotiate the lowest rates available.

Compare lenders. Look at offers from banks, credit unions, and online lenders. Focus on the full picture: APR, fees, and repayment terms.

Apply with your preferred lender. Submit your application along with tax returns, bank statements, and profit and loss statements.

Close and fund. Once approved, your new lender pays off the original loan. You start making payments at the new interest rate and updated terms.

Traditional banks may take one to four weeks to close. Online lenders like Clarify Capital can fund in as fast as 24 to 72 hours.

When Refinancing Makes Sense

Not every loan is worth refinancing. Here are the scenarios where it typically pays off:

Your credit improved since you first borrowed. If you took out a loan when your score was lower, you're likely eligible for better rates now.

Market rates dropped. Bank term loan rates currently range from 5.35.% to 11%, down from the highs of 2023. The Federal Reserve Bank of Kansas City reported that fixed-rate small business term loans averaged 7.67% in Q4 2024, compared to 8.6% at the start of that year.

You want predictable payments. Switching from a variable rate to a fixed rate locks in your monthly payment for the life of the loan, which makes budgeting easier.

You need to adjust your repayment period. Shortening your term builds equity faster (though payments go up). Lengthening it provides lower monthly payments but increases total interest.

The math works. A $100,000 business loan at 10% APR over 10 years costs about $158,581 total. Refinancing after three years at 8% saves roughly $6,787 in interest. But don't rely on rules of thumb; run your own break-even calculation.

Learn more about how to refinance a single high-rate loan.

What Is Business Debt Consolidation?

Debt consolidation takes a different approach. Instead of replacing one loan, you combine multiple debts into a single consolidation loan with one monthly payment. The goal isn't necessarily a lower rate on any individual debt; it's about simplifying your repayment plan and making your cash flow more manageable.

How Consolidation Works

Here's what the process typically looks like:

Inventory all your debts. List every loan, line of credit, credit card balance, and merchant cash advance. Note each balance, rate, monthly payment, and remaining term.

Calculate your total debt load. Add up all outstanding balances. This is the minimum your consolidation loan needs to cover.

Assess your creditworthiness. Your credit history and debt-to-income ratio both factor into the rates and terms you'll qualify for.

Compare consolidation products. Look at term loans and business lines of credit from multiple lenders. Pay attention to the APR, not just the payment amount.

Apply and close. Once approved, the new lender either pays off your existing debts directly or deposits funds so you can pay them yourself.

Confirm zero balances. After payoff, verify each old account shows a zero balance. Decide whether to close revolving accounts or keep them open for credit purposes.

When Consolidation Makes Sense

Consolidation isn't always the right move, but it works well in these situations:

You're managing multiple debts with different due dates. Tracking four or five payments to different lenders each month drains time and increases the risk of missed payments.

Your existing debts carry higher interest rates than current market offerings. If you're paying 20% to 40% on merchant cash advances or credit card balances, rolling everything into a single loan at 7% to 12% can slash your total cost.

You want one predictable payment. Simplifying your repayment schedule frees up bandwidth for running your business instead of managing debt.

You need to strengthen your borrowing profile. Forty-one percent of denied loan applicants cited "too much existing debt" as the reason in 2024, nearly double the 22% who said the same in 2021. Consolidation reduces your number of open obligations, which can help on your next application.

Learn more about how to consolidate multiple obligations.

How Each Option Affects Your Business Finances

Both refinancing and consolidation change your debt structure, but they hit your finances differently. Here's what to watch across three areas.

Interest Rates and Total Cost

Refinancing targets one loan and aims to reduce what you're paying. If you locked in at 9% or 10% during the rate peak, refinancing into today's range could save thousands over the life of the loan. Median fixed-rate term loans sat at 7.23% as of mid-2025, a meaningful drop from just a year prior.

Consolidation works differently. Your new rate could reflect a weighted average of your existing rates, or it may be lower if your creditworthiness has improved since you originally borrowed. The real savings often come from eliminating the most expensive debts in the mix. Replacing a 30% merchant cash advance and a 22% credit card balance with a 10% term loan changes the math dramatically, even if some of your original debts had reasonable rates.

One caution: Online lenders charge anywhere from 14% to 99%, so compare carefully. A consolidation product that "simplifies" your payments but charges 25% APR isn't doing you any favors.

Credit Score and Debt-to-Income Ratio

Both strategies require a hard credit inquiry, which may temporarily lower your score by a few points. Beyond that, the impact diverges.

Refinancing replaces one account with another on your credit report. Your total debt stays roughly the same, and the old account shows as closed. If you've held that loan for years, closing it can slightly reduce the average age of your accounts.

Consolidation can actually help your credit profile. Paying off multiple revolving balances (like credit card debt) and replacing them with a single installment loan reduces your credit utilization ratio. It also lowers the number of accounts with outstanding balances. Both factors can improve your creditworthiness over time, and a lower debt-to-income ratio makes you a stronger borrower for future financing.

Fees To Watch For

Don't overlook the costs of restructuring:

Origination fees. Many lenders charge 1% to 5% of the loan amount. On a $200,000 consolidation loan, that's $2,000 to $10,000.

Prepayment penalties. Check your existing loan agreements. Some lenders charge a fee for paying off early, which eats into your savings.

Closing costs. SBA loans and some bank products come with documentation fees, appraisal costs, and other expenses.

Application fees. Less common with online lenders, but some banks still charge them.

Before committing, calculate your break-even point: how many months of lower payments does it take to recoup the up-front costs? If you plan to pay off the new loan quickly, the fees might outweigh the loan benefits.

See What You Qualify for

With Clarify Capital

Rates From

6% APR

Funding In

24 Hours

Min. Credit Score

550+

Get a fast decision and same-day funding, whether you're refinancing a single loan or consolidating multiple debts.

How Business Debt Differs from Student Loans and Personal Debt

Business debt operates under different rules than student loans or personal debt, and most search results for "refinancing vs. consolidation" focus on the latter. Here's how the key differences break down.

| Business Debt vs. Student Loans and Personal Debt | ||||

|---|---|---|---|---|

| Debt type | Consolidation option | Refinancing option | Federal protections | Business applicability |

| Federal student loans | Federal direct consolidation loan; weighted average rate | Private lender refinancing; may lower rate but forfeits federal benefits | Income-driven repayment, loan forgiveness, IBR | No |

| Personal/credit card debt | Balance transfer to promotional-rate card | Personal loan from bank or credit union | None (private market) | No |

| Business debt | No federal program; negotiate directly with lenders | Term loans, lines of credit, secured loans | None | Yes |

Business owners can't rely on the programs designed for student borrowers or personal finance. Your options will depend on what you negotiate with your lender.

How To Refinance or Consolidate Your Business Debt

Whether you're refinancing one loan or consolidating several, the process follows a similar path:

Audit your existing debt. Pull together every loan agreement, credit line statement, and merchant cash advance contract. List the balance, rate, payment, and remaining term for each. You can't make a smart decision without knowing exactly what you owe.

Pull your credit report. Your creditworthiness drives the rates and terms you'll qualify for. Even a 50-point improvement can meaningfully affect your new interest rate.

Calculate your break-even point. Add up the fees for the new loan (origination, closing costs, etc.) and divide by your monthly savings. That's how many months it takes to recoup the costs.

Compare lenders. Don't just go with your current bank. Small banks had the highest full approval rate at 54% in the 2024 Federal Reserve Small Business Credit Survey, while large banks approved 45% and online lenders approved 30%. But approval rates don't tell the whole story; online lenders often fund faster and work with a wider range of credit profiles.

Gather documentation. Most lenders want two years of tax returns, six months of bank statements, a current profit and loss statement, and a balance sheet.

Apply and close. Traditional banks may take two to four weeks. Online lenders like Clarify Capital can close and fund in as fast as 24 to 48 hours, which matters when cash flow is tight.

The Right Option Starts With the Right Lender

Refinancing and consolidation solve different problems. If you have one loan with terms that no longer make sense, refinancing is the cleaner path. If you're spread across multiple debts with different rates and due dates, consolidation brings everything under one roof.

Either way, the goal is the same: lower your cost of capital, simplify your payments, and free up cash flow so you can invest in growing your business.

At Clarify Capital, we offer term loans up to $5 million starting at 6% APR, with funding in as fast as 24 hours. Whether you're looking to refinance a single high-rate loan or consolidate multiple obligations, we can help find the right structure. Apply today for a loan through Clarify Capital.

FAQs

I'll answer a few questions I often get about refinancing or consolidating debt.

Can Clarify Capital Refinance My Business Debt?

Yes. We help business owners replace existing loans with more competitive terms. Our rates start at 6% APR, with repayment terms from six months to 10 years and funding in as fast as 24 to 72 hours. Start your application here.

Is It Better To Refinance or Consolidate Business Debt?

It depends on your situation. Refinancing works best when you have one loan and want a lower rate or different terms. Consolidation makes more sense when you're managing multiple debts and want to streamline into a single payment. Consider your total debt load, the rates you're currently paying, and how much you'd save after accounting for fees.

Does Refinancing Hurt Your Credit Score?

A hard inquiry may temporarily dip your score by a few points. But if refinancing leads to consistent on-time payments at a lower balance, your score typically recovers within a few months and may improve over time.

What Is the 2% Rule for Refinancing?

The 2% rule is a guideline from mortgage lending that suggests refinancing makes sense when you can reduce your rate by at least two percentage points. For business loans, the calculation is more nuanced: a smaller rate reduction can still save significant money on a large balance, and fees plus remaining term length also factor in. Run your own break-even analysis rather than relying on a blanket rule.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts