If you're a business owner looking to grow without putting up specific collateral, unsecured business loans could be the right move. I've worked with thousands of small business owners who needed capital fast. For many of them, an unsecured loan was the simplest path to funding.

Lenders issue these loans based on your creditworthiness and business performance rather than physical assets, which means you can access working capital without risking what you've already built. Here, I'll walk you through how unsecured business loans work, what they cost, who qualifies, and how to get funded.

What Are Unsecured Business Loans?

An unsecured business loan is a financing option that doesn't require you to pledge assets as collateral, though many lenders require a personal guarantee. Unlike secured business loans, which are backed by real estate, equipment, or other business assets, unsecured loans rely on your creditworthiness and ability to repay.

Many unsecured loans provide a lump sum you repay over a fixed term with relatively predictable monthly payments. They're a smart option for covering:

Working capital. Working capital covers day-to-day operating expenses during slower business cycles or cash flow gaps.

Business expenses. Handling unexpected costs like repairs, inventory purchases, or marketing campaigns.

Expansion. Financing new projects, opening additional locations, or hiring staff.

Because they don't require specific collateral, unsecured loans are particularly valuable for businesses that need capital but want to keep their personal assets and business assets protected.

Unsecured vs. Secured Loans

The main distinction between unsecured and secured loans is the collateral requirement. With secured loans, you must offer something of value to back the loan. This could be real estate, vehicles, or other business assets. If you can't repay, the lender can seize the collateral to recover their money.

Unsecured loans, on the other hand, rely on your credit score, business history, and the lender's assessment of your ability to repay. This makes them more accessible to businesses with fewer assets, but it also means that interest rates are typically higher to compensate for the increased risk to the lender.

| Secured vs. Unsecured Loans | ||

|---|---|---|

| Feature | Secured business loans | Unsecured business loans |

| Collateral required | Yes: Business or personal assets | No collateral required |

| Approval speed | Slower: Involves asset appraisals | Faster: Streamlined application and fewer documents needed |

| Interest rates | Lower interest rates | Higher interest rates |

| Typical use case | Large purchases, real estate, and long-term capital expenditures | Short-term needs, working capital, cash flow bridging |

| Risk to borrower | Asset seizure if you default | No specific asset risk: Based solely on creditworthiness and repayment ability (though borrowers may still be personally liable) |

| Loan amount range | $50,000 to $5 million+ | $10,000 to $500,000 |

| Credit score sensitivity | High: Strong personal and business credit required | Moderate: Income and credit history both matter |

| Repayment terms | Longer terms (3–10+ years) | Shorter terms (6 months to 5 years) |

Types of Unsecured Business Financing

Several loan types and credit products fall under the unsecured umbrella, each designed for different business goals and cash flow needs. Here are some of the most helpful for businesses:

Term loans. A term loan gives you a lump sum up front that you repay in fixed monthly payments over a set period, typically six months to five years. This is one of the most straightforward unsecured loan options, ideal for one-time investments like renovations, equipment, or hiring.

Business lines of credit. A line of credit works like a revolving credit line. You're approved for a maximum amount and draw from it as needed. You only pay interest on what you've borrowed, making it a strong option for managing cash flow or covering recurring expenses.

SBA loans. The Small Business Administration backs several loan programs through approved lenders. SBA loans often come with lower interest rates and longer repayment terms, though the application process is more involved and approval can take several weeks.

Merchant cash advances. A merchant cash advance provides a lump sum in exchange for a percentage of your future sales. Repayment adjusts automatically based on daily revenue, making it flexible for businesses with strong sales volume but inconsistent monthly revenue.

Invoice factoring. If your business has outstanding invoices, invoice factoring lets you sell them to a factoring company at a discount for immediate cash. This can be useful for B2B companies with long payment cycles who need working capital now.

Business credit cards. For smaller, ongoing expenses, business credit cards offer revolving credit with variable APRs, typically between 18% and 30%. They can also help build your business credit history over time.

The right type of loan depends on how much capital you need, how quickly you need it, and how your business generates revenue. I often recommend that business owners compare at least two or three financing options before committing.

Benefits of Unsecured Loans for Business Growth

Unsecured loans offer several advantages. They're especially valuable when you need working capital fast, lack sufficient collateral, or want to put your personal assets on the line. Whether you're covering a short-term cash gap, funding a one-off project, or growing your business, here's what unsecured financing can do for you:

Financing Flexibility

One of the biggest benefits of unsecured loans is their flexibility. Since you don't need to offer collateral, these loans are accessible to a wider range of businesses, including those without substantial physical assets to pledge. Flexible repayment terms ranging from six months to five years help you manage cash flow without putting vehicles or real estate at risk.

For example, here's something I see a lot: If you run a retail business and a supplier offers a time-sensitive deal on bulk inventory, an unsecured loan can help you move quickly without tying up assets.

Simple Application and Approval Process

The application process for an unsecured loan is generally faster and more straightforward than for secured loans. You don't have time to appraise collateral, so lenders focus on your creditworthiness and business history, making credit approval go faster.

With many online lenders, you can complete an application in minutes and receive a funding decision within a few business days, sometimes even the same day.

Asset Preservation

Because unsecured loans don't require specific collateral, they let you preserve your business assets and personal assets for operational purposes or future opportunities. If you own a fleet of delivery vehicles, for instance, you won't have to risk them to secure capital. This separation protects what you've built while still giving you access to the business funding you need.

Improvement in Business Credit

Taking out an unsecured loan and repaying it on time can be good for your business credit score. This opens doors to better financing options down the road, including lower interest rates and larger loan amounts. Building a strong credit history shows future lenders that your business can manage debt responsibly.

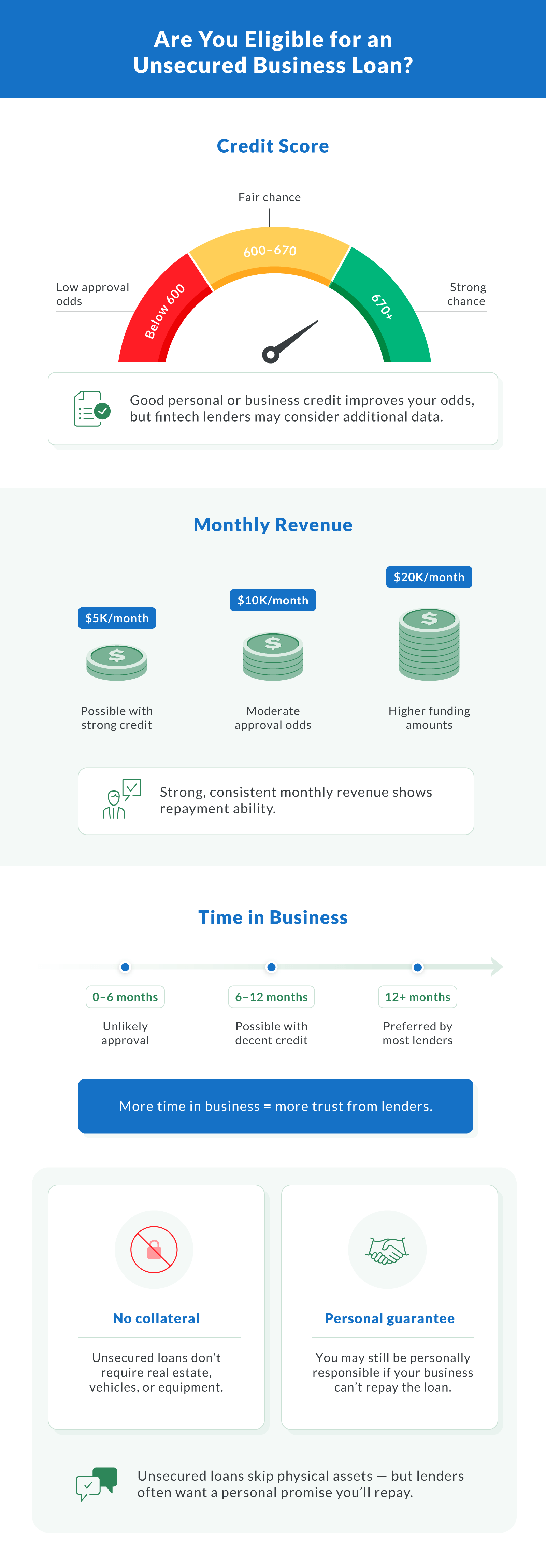

Eligibility Requirements for Unsecured Business Loans

Qualifying for an unsecured business loan depends on several factors. Since there's no collateral backing the loan, lenders lean more on your credit profile and financial performance. Here's what many lenders look for:

Personal credit score. Many traditional banks require a FICO score of 680 or higher. Online and alternative lenders may work with borrowers who have fair credit scores (as low as 500 with Clarify Capital), though higher interest rates may apply. Borrowers with good credit (generally 700+) qualify for the most competitive rates.

Time in business. Lenders typically want to see at least six months to two years of operating history. Businesses with longer track records and consistent revenue present less risk and qualify for better loan terms. Clarify Capital requires six months in business.

Annual revenue. Minimum revenue requirements vary by lender, but Clarify Capital requires $10,000 in monthly business revenue.

Business credit history. A strong business credit profile, including on-time payments, low credit utilization, and minimal hard inquiries, strengthens your application and improves your creditworthiness in the eyes of lenders.

Financial documentation. Expect to provide tax returns, financial statements, bank statements (with Clarify Capital, it's the last three months), and proof of a business checking account. Keeping your records up to date speeds up underwriting.

Personal guarantee. While unsecured loans don't require collateral, many lenders still ask for a personal guarantee. This means you're personally responsible for repaying the loan if your business can't, protecting the lender without needing you to pledge specific assets.

A growing number of fintech lenders now use cash-flow-based underwriting models that evaluate real-time business revenue rather than relying solely on personal credit scores. According to the Federal Reserve's 2025 Small Business Credit Survey, approval rates for financing tend to be higher at small banks and online lenders compared to large banks.

How Much Does an Unsecured Business Loan Cost?

The cost of an unsecured business loan depends on your APR, loan amount, repayment terms, and any additional fees. Because there's no collateral to reduce the lender's risk, unsecured loans typically carry higher interest rates than secured options. Here's what to expect:

Traditional bank loans. APRs typically range from roughly 6%–11%+ for well-qualified borrowers with strong credit and established businesses.

Online and alternative lenders. APRs can range from 6% to 75%+, depending on your credit profile, time in business, and revenue. Loans through Clarify Capital typically have APRs ranging from 6% to 14+%.

SBA loans. Fixed rates for SBA 7(a) loans currently range from roughly 8%–13%, depending on loan amount and term.

Origination fees. Some lenders charge an origination fee, typically 1% to 3% of the loan amount, deducted up front from your disbursement.

Monthly Payment Example: $50,000 Loan

To give you a sense of what monthly payments look like, here's how a $50,000 unsecured business loan breaks down at different rates and terms:

| APR | Monthly payment for 3-year term (36 months) | Monthly payment for 5-year term (60 months) | Total interest paid (5-year) |

|---|---|---|---|

| 10% | $1,613 | $1,062 | $13,720 |

| 15% | $1,733 | $1,190 | $21,400 |

| 20% | $1,854 | $1,325 | $29,500 |

These figures show why shopping for the best rate matters. Over the life of the loan, even a few percentage points in APR can mean thousands of dollars in additional interest.

How To Apply for an Unsecured Business Loan

The process for getting an unsecured business loan is more streamlined than most business owners expect, especially with online lenders like Clarify Capital. Here's a typical step-by-step process:

Determine your funding needs. Figure out how much capital you need (up to $5M with Clarify Capital), what you'll use it for, and what repayment terms fit your cash flow. Having a clear purpose strengthens your application and helps you avoid borrowing more than necessary.

Check your credit. Review both your personal credit score and your business credit profile before applying. Correcting errors or paying down balances can improve your creditworthiness and help you qualify for better rates. Clarify Capital often offers same-day funding for credit scores over 550, so even borrowers without perfect credit may still qualify.

Gather your documents. Many lenders require recent tax returns, financial statements, and basic business information. With Clarify Capital, your adviser will need three months of your most recent bank statements to verify income, along with your EIN and business checking account details.

Confirm you meet the minimum requirements. Before applying, make sure you meet the lender's baseline criteria. Clarify Capital requires at least $10,000 in monthly revenue, more than six months in business, a business bank account, and U.S. location or incorporation.

Compare lenders and loan options. Don't settle for the first offer. Compare APRs, repayment terms, fees, and funding speed across multiple lenders, including traditional banks, credit unions, and online platforms. Clarify Capital offers APRs starting as low as 6% on revenue-based financing rather than collateral-based loans, so your business performance matters more than your assets.

Submit your application. With Clarify Capital, the online application takes about two minutes. The lender then runs its underwriting review, evaluating your credit approval potential based on your full financial profile.

Review and accept your offer. If approved, carefully review the loan terms, including APR, repayment schedule, any origination fees, and whether a personal guarantee is required. Make sure monthly payments align with your projected cash flow before signing.

Receive your funds. Depending on the lender, funding can arrive in as few as one to three business days. Clarify Capital often offers same-day funding for qualified borrowers with credit scores over 550.

Key Considerations When Choosing an Unsecured Loan

While unsecured loans offer many benefits, there are trade-offs to weigh. Here are the most important factors:

Interest Rates and Repayment Terms

Unsecured loans typically have higher interest rates than secured loans because they pose a greater risk to lenders. The best approach is to compare rates from multiple lenders and understand how your credit score affects your terms.

Before signing, make sure you're clear on the full repayment schedule. Knowing your exact monthly payments makes it easier to manage your cash flow and avoid surprises over the life of the loan.

Loan Amount and Types of Financing

Unsecured loans come in various loan amounts depending on your business needs and financial situation. Determine how much funding you require and what type of loan will best support your goals.

If you need ongoing access to funds, a line of credit might be more suitable than a term loan. On the other hand, if you have a specific project in mind, a term loan with a fixed repayment schedule could be a better fit.

Also consider whether a personal guarantee is required. While unsecured loans don't require collateral, some lenders ask for a personal guarantee, meaning you're personally responsible for repaying the loan if your business can't.

Lenders and Financial Institutions

Not all lenders are created equal, and choosing the right one matters. Traditional banks (many of which are member FDIC institutions), credit unions, and online lenders all offer unsecured small business loans, but their terms, rates, and eligibility requirements can vary significantly.

Online lenders and fintech platforms often offer faster approvals and may evaluate overall business performance instead of relying solely on credit scores. The Small Business Administration also offers loan programs that provide additional support and resources for small business owners. Working with a lender who understands your industry is key to getting the best deal.

Common Misconceptions About Unsecured Loans

Despite their growing popularity, unsecured business loans are still widely misunderstood. These misconceptions can cause business owners to overlook a financing option that might be a better fit than a secured loan. Let's clear up the most common myths:

Myth: You Need Perfect Credit To Qualify

Reality: While a strong credit score helps secure better repayment terms, it's not the only factor lenders consider. Many online lenders now use alternative underwriting models that evaluate your business credit, cash flow, and overall financial performance. This shift allows borrowers with fair credit but healthy revenue to access capital that would have previously been out of reach; even those with bad credit may find options through alternative lenders.

Myth: Unsecured Loans Always Charge Sky-High Rates

Reality: Unsecured loans typically have higher interest rates than secured loans since there's no collateral backing the debt. But that doesn't mean they're unaffordable. Lenders now offer competitive rates, especially to borrowers who demonstrate strong creditworthiness or provide a personal guarantee. Funding options from credit unions and reputable online lenders can be surprisingly cost-effective, particularly for borrowers with good credit and a solid business plan.

Myth: Loan Amounts Are Always Small

Reality: There's a common belief that unsecured loans are only good for covering short-term gaps. In practice, loan amounts can reach into the hundreds of thousands, especially if your financial statements, revenue, and payment history show that your business can manage the repayment. Lenders evaluate the full picture, so businesses with strong cash flow and established business credit may qualify for larger loans than expected.

Tips for Making an Informed Decision

Making the right financing decision can have a lasting impact on your business. Before applying, review your credit profile, credit history, and keep your financial records current. Here are practical steps to set yourself up for success:

Assess your business needs. Understand what you need the funds for, how much you require, and how quickly you can repay. This clarity helps you choose the right type of loan and avoid overborrowing.

Prepare a strong business plan. A solid business plan demonstrates to lenders that you have a clear strategy for using the funds and a realistic path to repayment. Include financial projections and a detailed description of how the loan supports your goals.

Seek expert advice. Consult with financial advisors or business mentors who can help you find the best terms and avoid potential pitfalls.

Explore all your financing options. Unsecured loans are one of many loan options available. Compare SBA loans, lines of credit, merchant cash advances, and other funding options to make sure you're choosing the best fit for your situation.

Get Funded With Clarify Capital

Unsecured business loans are a flexible, accessible financing option for businesses looking to grow without the burden of collateral. By understanding the benefits, eligibility requirements, and costs covered in this guide, you can make informed decisions that put your business in the strongest position.

Ready to take the next step? Apply today with Clarify Capital. Our online application takes just two minutes, and qualified borrowers can sometimes receive same-day funding with no collateral required.

FAQs About Unsecured Business Loans

Below, we cover common questions about getting a no-collateral loan.

How Hard Is It To Get an Unsecured Business Loan?

It depends on your credit profile, time in business, and revenue. Traditional banks typically require a FICO score of 680+ and at least two years of operating history. Online lenders have broader eligibility requirements and may approve borrowers with lower credit scores if they demonstrate strong business revenue and consistent cash flow. Preparing your financial statements and maintaining a clean credit history before applying improves your chances significantly.

Can a Business Get an Unsecured Loan?

Yes. Many types of businesses, from retail and service-based companies to restaurants and professional services firms, can qualify for unsecured business loans. The key factors are your creditworthiness, business revenue, and operating history. Even businesses without significant physical assets can access capital through unsecured financing options, making this one of the most versatile loan types available.

Can I Get a Loan With Just My EIN Number?

Some lenders market "EIN-only" loans, but in practice, most unsecured business lenders require a personal credit check and a personal guarantee as part of the application process. Lenders want to evaluate the full picture (your business credit, personal credit score, and financial performance) before extending financing. That said, some alternative lenders place more weight on business revenue than personal credit, which can help borrowers who want to minimize personal exposure.

How Much Is a $50,000 Business Loan Monthly?

Your monthly payment depends on the APR and repayment term. At 10% APR over five years, a $50,000 unsecured business loan would cost roughly $1,062 per month. At 15% APR over the same term, that rises to about $1,190 per month. Shorter repayment terms mean higher monthly payments but less total interest paid over the life of the loan. See the payment estimate table in the cost section above for a full breakdown.

What Types of Businesses Qualify for Unsecured Loans?

Unsecured business loans are available across a wide range of industries including retail, restaurants, construction, trucking, health care, and professional services. Most lenders require a minimum time in business (typically six months to two years), consistent business revenue, and a demonstrated ability to make monthly payments. Your eligibility is based more on financial performance than the specific type of business you run.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts