Business credit is a measure of how reliable your company looks to lenders, suppliers, and partners based on its financial track record. It's tied to your business entity (not to you personally) and directly affects the loan terms, interest rates, and credit limits your company can access. If you've ever been quoted a high rate or asked to sign a personal guarantee, a thin credit profile is likely the reason.

You don't need years of revenue history to start building business credit. With the right steps, new businesses and established companies alike can create a profile that opens doors to better financing. In my 15+ years helping small business owners at Clarify Capital secure funding, I've watched how a strong business credit score changes the conversation with lenders: lower rates, higher limits, and fewer personal guarantees.

Here's what separates business credit from personal credit, how the three major bureaus score your company, and a seven-step process to build yours from scratch.

How Business Credit Differs From Personal Credit

Your personal credit score and your business credit score are tracked separately, scored differently, and used by different audiences. Here's how they compare:

Tied to different identities. Personal credit is linked to your Social Security number. Business credit is tied to your EIN (employer identification number) and your company's legal entity.

Different scoring scales. Personal credit scores range from 300 to 850. Business scores vary by bureau: Dun & Bradstreet's PAYDEX runs 0 to 100, and Experian's Intelliscore Plus also uses a 1 to 100 scale.

Public vs. private. Your personal credit report requires permission to pull. Business credit reports are generally public, so anyone (suppliers, lenders, potential partners) can check your company's creditworthiness.

Payment terms matter more. Personal credit tracks whether you pay on time. Business credit also tracks how you pay relative to terms: paying early can actually boost your score.

Separate liability. Strong business credit lets you separate your personal and business finances, reducing the need for a personal guarantee on loans. That separation between personal and business obligations protects your personal assets if the company hits a rough patch.

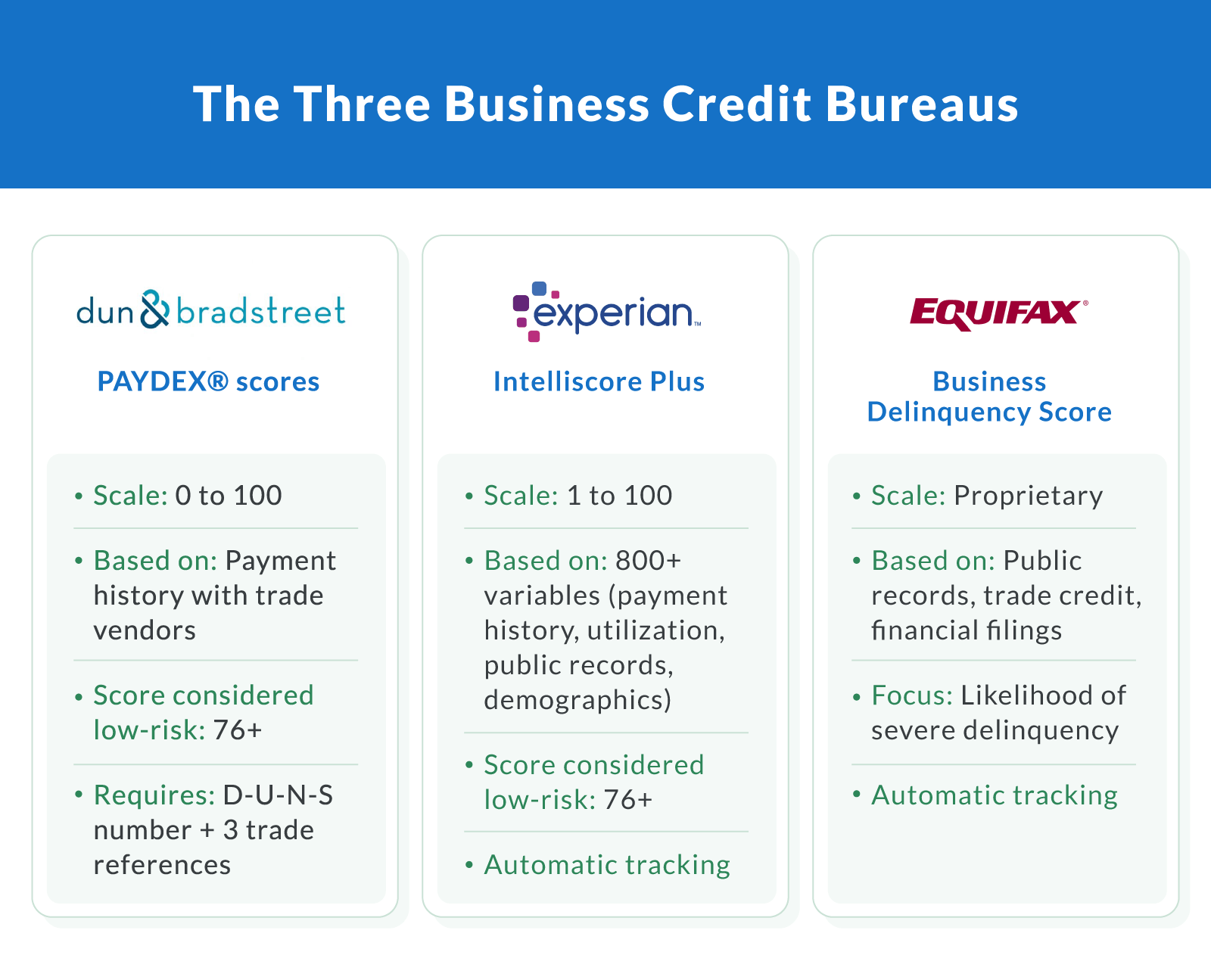

The Three Business Credit Bureaus and Their Scores

Three credit reporting agencies track and score your business credit history. Each uses different data and scoring models, and most lenders check at least one before extending credit.

Dun & Bradstreet PAYDEX Score

The PAYDEX score is the most widely recognized business credit score. It ranges from 0 to 100 and is based entirely on your payment history with vendors and suppliers that report to D&B. A score of 80 or above signals that you pay on time or early. Scores below 50 indicate late payments.

To get a PAYDEX score, you'll need a D-U-N-S number (free from Dun & Bradstreet) and at least three trade references reporting payment data. The more vendors that report, the stronger your profile.

Experian Intelliscore Plus

Experian's Intelliscore Plus weighs over 800 variables to assess your credit risk, pulling from payment history, credit utilization, public records, and company demographics. Scores range from 1 to 100, with 76 or higher considered low risk.

What sets this model apart is scope. Beyond whether you paid on time, it factors in the age of your credit accounts, outstanding balances, and industry risk patterns.

Equifax Business Delinquency Score

Equifax focuses on how likely your company is to become severely delinquent on payments. It pulls data from public records, trade credit accounts, and financial filings. Unlike D&B, Equifax doesn't require a separate application; it starts tracking your business once your company data appears in its database.

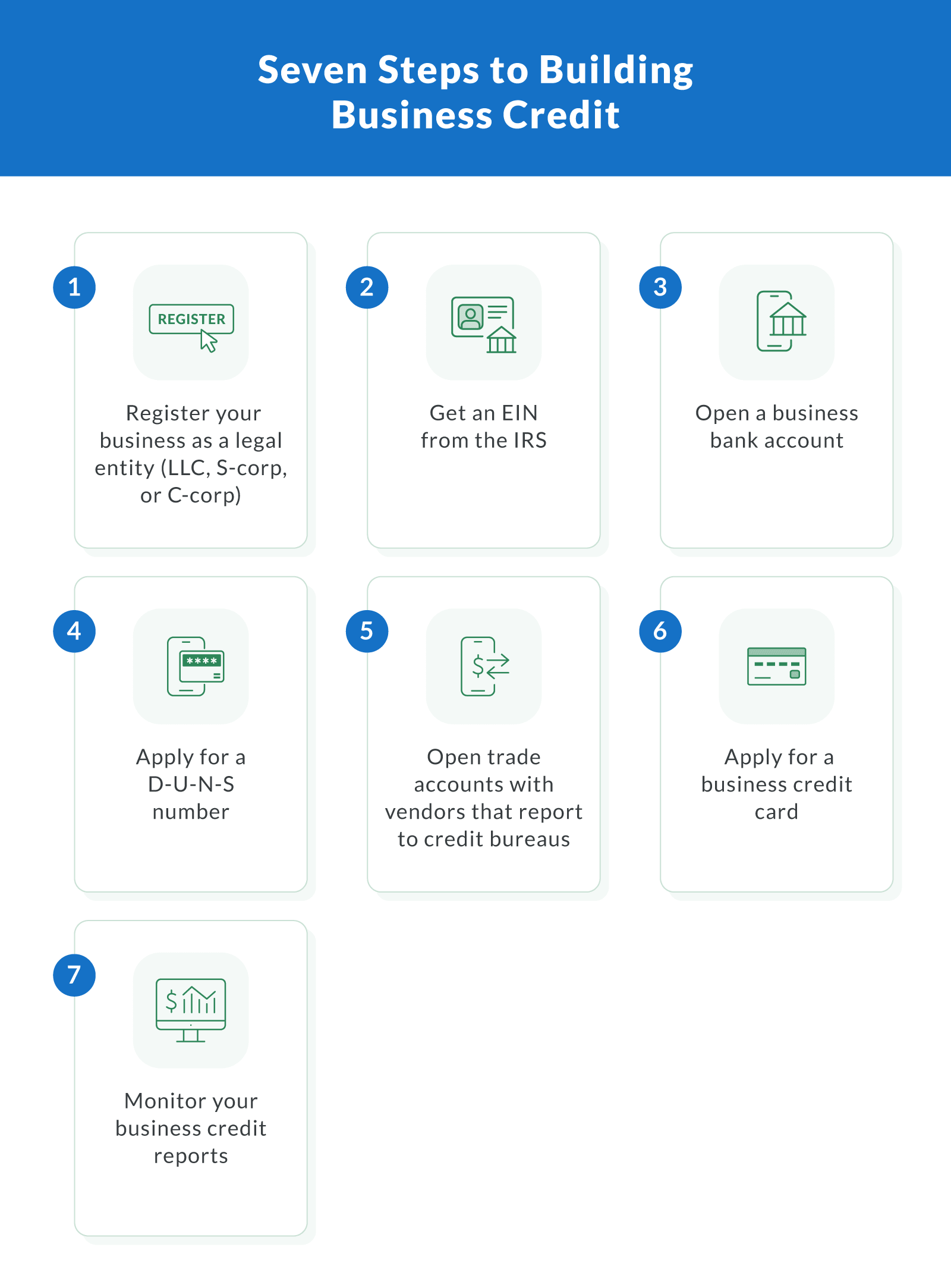

How To Build Business Credit in Seven Steps

Step 1: Register Your Business as a Legal Entity

Credit bureaus and lenders don't treat sole proprietorships the same way they treat LLCs or corporations. Forming a legal entity (LLC, S-corp, or C-corp) establishes your company as a separate business structure in the eyes of the law and financial institutions.

Register with your state, get your articles of organization or incorporation, and make sure your business name, address, and phone number are consistent across all filings. Inconsistent data is one of the first things that slows down credit building for new businesses.

Step 2: Get an EIN From the IRS

Your employer identification number is your business's tax identification number, the equivalent of a Social Security number for your company. You'll need it to open a business bank account, file taxes, and apply for credit. The IRS issues EINs for free, and you can apply online in minutes.

Already have your EIN and need funding now? Learn how to qualify for no-doc business loans with an EIN only.

Step 3: Open a Business Bank Account

A dedicated business bank account keeps your business finances separate from personal spending. Lenders want to see a clear financial trail for your company, and commingling funds is a red flag. A separate account also reinforces the wall between personal and business obligations that protects your personal credit score.

Choose a financial institution that works with small businesses and open a checking account under your company's legal name and EIN.

Step 4: Apply for a D-U-N-S Number

Your D-U-N-S number is a unique nine-digit identifier assigned by Dun & Bradstreet. It's free to obtain and serves as the foundation for your PAYDEX score. Without one, D&B can't track your payment history, and many lenders and suppliers won't be able to find your credit profile.

Apply directly through Dun & Bradstreet's website. Processing typically takes 30 days, though expedited options are available.

Ready to put your business credit to work?

Loan Amounts

Up to $5M

Fast Funding

24 Hrs

Credit Score

500+

Strong credit opens the door to better rates, higher limits, and faster funding. See what your business qualifies for.

Step 5: Open Trade Accounts With Vendors That Report

Trade credit is one of the fastest ways to build a business credit history. Look for vendors that offer net 30 payment terms and report to at least one business credit bureau. Common options include office supply companies, shipping providers, and fuel card programs.

Here's the catch: Only about 10,000 of the roughly 500,000 suppliers in the U.S. report payment data to credit agencies. Don't assume your vendor accounts are automatically helping your score. Ask up front whether they report, and prioritize lenders and suppliers that do.

Pay every invoice on time (or early if you can). Early payments boost your PAYDEX score, while even a single late payment can set back months of progress.

Step 6: Apply for a Business Credit Card

A business credit card builds your profile in two ways: it adds a revolving credit account to your business credit report, and it creates a consistent payment history. These are two of the types of credit that bureaus weigh when scoring your company. Start with a card that doesn't require extensive credit history; many issuers offer options for newer businesses with fair personal credit.

Keep your credit utilization below 30% of your available limit. Lower is better. High utilization signals risk to credit bureaus and lenders, even if you pay the balance in full each month.

Step 7: Monitor Your Business Credit Reports

Credit monitoring isn't optional once you've started building. Errors on your business credit report can drag down your score without you knowing, and they're more common than you'd expect. Check your reports at least quarterly through each bureau's website to verify that your payment data is accurate and your trade accounts are showing up.

Catching mistakes early (incorrect late payments, missing accounts, wrong company information) lets you dispute them before they affect your creditworthiness with lenders and suppliers. Regular monitoring is one of the simplest ways to protect your company's financial health.

How Business Credit Helps You Qualify for Better Loans

Your business credit score is one of the first things lenders check alongside other small business loan requirements when you apply for financing. A strong profile gives you leverage at every stage:

Lower interest rates. Lenders reserve their best rates for borrowers with proven payment histories. Good business credit can mean the difference between a 6% APR and a double-digit rate on a term loan.

Higher borrowing limits. A solid credit profile tells lenders you can handle more capital. At Clarify Capital, we offer business loans up to $5M, and creditworthy borrowers are more likely to qualify near that ceiling.

Fewer personal guarantees. When your credit profile speaks for itself, lenders are less likely to require your personal assets as collateral. That protects your home, savings, and personal score.

More financing options. Strong credit qualifies you for term loans, business lines of credit, equipment financing, and invoice factoring. Weaker profiles often limit you to higher-cost products.

Faster approvals. Lenders who can verify your credit history quickly spend less time underwriting. That means faster funding when you need it.

Common Mistakes That Stall Your Business Credit

Credit building takes patience, but these are the mistakes I see trip up small business owners most often:

Mixing personal and business expenses. Using a personal credit card for business purchases doesn't build your small business credit profile. It just adds to your personal utilization. Keep them separate from day one.

Ignoring payment terms. Paying invoices "whenever" instead of on or before the due date kills your PAYDEX score. Treat every net 30 account like a credit-building opportunity, because that's exactly what it is.

Not checking who reports. You might have five vendor accounts, but if none of them report to credit agencies, your profile stays empty. Always ask before opening an account.

Maxing out credit cards. High credit utilization hurts your score even if you pay the balance in full. Keep usage under 30% of your available limit.

Skipping credit monitoring. Errors happen: a vendor reports a payment late when it wasn't, or a closed account still shows as open. Without regular checks, you won't catch problems until they cost you a deal.

Better Credit, Better Capital

You won't build your business credit overnight, but every step you take now compounds. A strong profile gives you negotiating power with lenders and more choices in how you fund growth. Even if your company is a startup, you can begin establishing business credit with the process above.

If you're ready to put that credit profile to work, apply with Clarify Capital to see what you qualify for.

Frequently Asked Questions

I'll answer a few more questions I often get about building business credit.

How Long Does It Take To Build Business Credit?

Most businesses can establish a basic credit profile within three to six months by opening trade accounts and making consistent, on-time payments. Reaching a score high enough for competitive loan terms typically takes six to 12 months of active effort.

How Do You Get a 100 Business Credit Score?

A PAYDEX score of 100 means you consistently pay vendors before the due date. To get there, open trade accounts with suppliers that report to Dun & Bradstreet, set up net 30 terms, and pay every invoice early. It's achievable, but it takes discipline and the right vendor relationships.

Can You Build Business Credit With Bad Personal Credit?

Yes. Business credit is tracked separately, so a low personal score doesn't prevent you from establishing business credit. Start by forming a legal entity, getting your EIN, and opening trade accounts. Some lenders will factor in your personal credit when evaluating applications, but a strong business credit history can offset that over time. Alternative lenders also offer business loans with no credit check that focus on revenue and time in business instead.

Do All Lenders Check Business Credit?

Not all, but most. Traditional banks and SBA lenders almost always pull a business credit report. Alternative lenders may weigh other factors more heavily, like monthly revenue and time in business. Still, having strong credit gives you more options and better terms across the board.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts