If you're a small business owner looking at financing options for your company, the long and documentation-heavy application processes of many conventional loan options can be really daunting.

Maybe you don't have perfect credit, or your business is new and doesn't have much financial history yet. Maybe you just want less hassle and fast funding options.

Traditional lenders, like banks, have ever-stricter lending requirements that exclude many businesses trying to reach their growth goals. Alternative lenders (like online lenders and fintech platforms) can often offer financing options that use bank statements and business revenue instead of traditional documentation.

What "No-Doc" and "EIN-Only" Really Mean

Before we get into the meat of these two financing options, there's an important distinction to understand about them that most lending platforms don't fully explain. The terms "no-doc" and "EIN-only" (EIN meaning employer identification number) are often used together and describe the same types of financing: options that rely more on revenue and cash flow than traditional documentation or credit requirements. But here's the difference:

| What it's supposed to mean | What it really means in practice | |

|---|---|---|

| No-doc loans | Minimal documentation required | No tax returns, but still requires bank statements and revenue verification |

| EIN-only loans | Approval based on business (not personal credit) | Less reliance on personal credit, but still may check it and require a guarantee |

Loans that actually require zero documentation are very rare, if not completely nonexistent. "No-doc" actually just means fewer documents and a fairly easy application process. It refers to lending options where documents like tax returns and profit and loss statements (P&Ls) aren't required, but things like bank statements and a soft check of your personal credit most likely still are.

Similarly, "EIN only" loans are not lending options that you can obtain by only giving out your employer identification number. Rather, they're business loans that you can qualify for based on business performance rather than your personal credit.

Can You Get a Loan With Only Your EIN?

You can find lenders who focus on your business's revenue and cash flow rather than your personal credit score. This is what is really meant by "EIN-only" loans in the industry.

Often, these types of options have higher rates and shorter terms. But that's the trade-off of applying with fewer qualifications and more flexible requirements. We'll go over the best options below.

Invoice Factoring

Invoice factoring is when a business sells its unpaid invoices to a factoring company. The factoring company gives you an up-front payment and takes over the legwork of collecting payments on future invoices in exchange for a cut of them.

This is a great option if you tend to have trouble with slow-paying clients and don't mind a third party intervening in the relationship. Invoice factoring is often one of the easiest to obtain because eligibility is based on the strength of your invoices rather than your personal ability to repay a loan.

Equipment Financing

Equipment financing is a funding option specifically for businesses that need to purchase new equipment, from machinery to tech and vehicles. It's great if you need to replace old assets or expand your operations, but you can't quite shoulder the huge up-front cost that often comes with it. This helps you spread payments over time.

Basically, the lender pays for the equipment (either directly or by reimbursing you), and then you make monthly payments (plus interest) over a set period, usually somewhere between one and six years. Key to this funding is that the equipment itself serves as collateral, so if you default on payments, the equipment can be taken away.

Merchant Cash Advance

A merchant cash advance (MCA) is a type of financing in which a business receives a lump sum up front in exchange for a portion of its future sales.

After getting the cash advance, you repay a fixed percentage of your daily or weekly revenue (called a holdback) until the agreed repayment total is paid off. That total is determined by factor rates instead of traditional interest rates. For example: An advance amount of $20,000 with a factor rate of 1.3 would equal a total repayment cost of $26,000.

The main caveat is that you pay more when sales are high (and less when they're slow), but eligibility is based primarily on revenue consistency and sales volume.

No-Doc Loan Options

These are common financing options that offer application processes with fewer documentation and more lenient eligibility requirements. More than "no doc" loans, they're "lower doc" loans. They include the options I just fleshed out, plus two more that are also quite flexible.

| Documentation/info required | What's important for qualifying | Typical funding speed | Best for | |

|---|---|---|---|---|

| Invoice factoring | Business invoices, basic business information, and bank account details (no tax returns typically required) | The strength of your invoices | Often within 1 to 2 weeks (after invoice verification) | Business-to-business (B2B) businesses with unpaid invoices that need fast access to cash flow |

| Equipment financing | Equipment quote or invoice, basic business info, and sometimes bank statements | Equipment as the loan collateral | Usually, 1 to 5 days | Businesses buying or upgrading equipment without shouldering high up-front costs |

| Merchant cash advance | Recent bank statements or credit card processing statements (no tax returns typically required) | Revenue consistency and sales volume | Can be as fast as 24 to 48 hours | Businesses with steady sales that want fast and flexible funding |

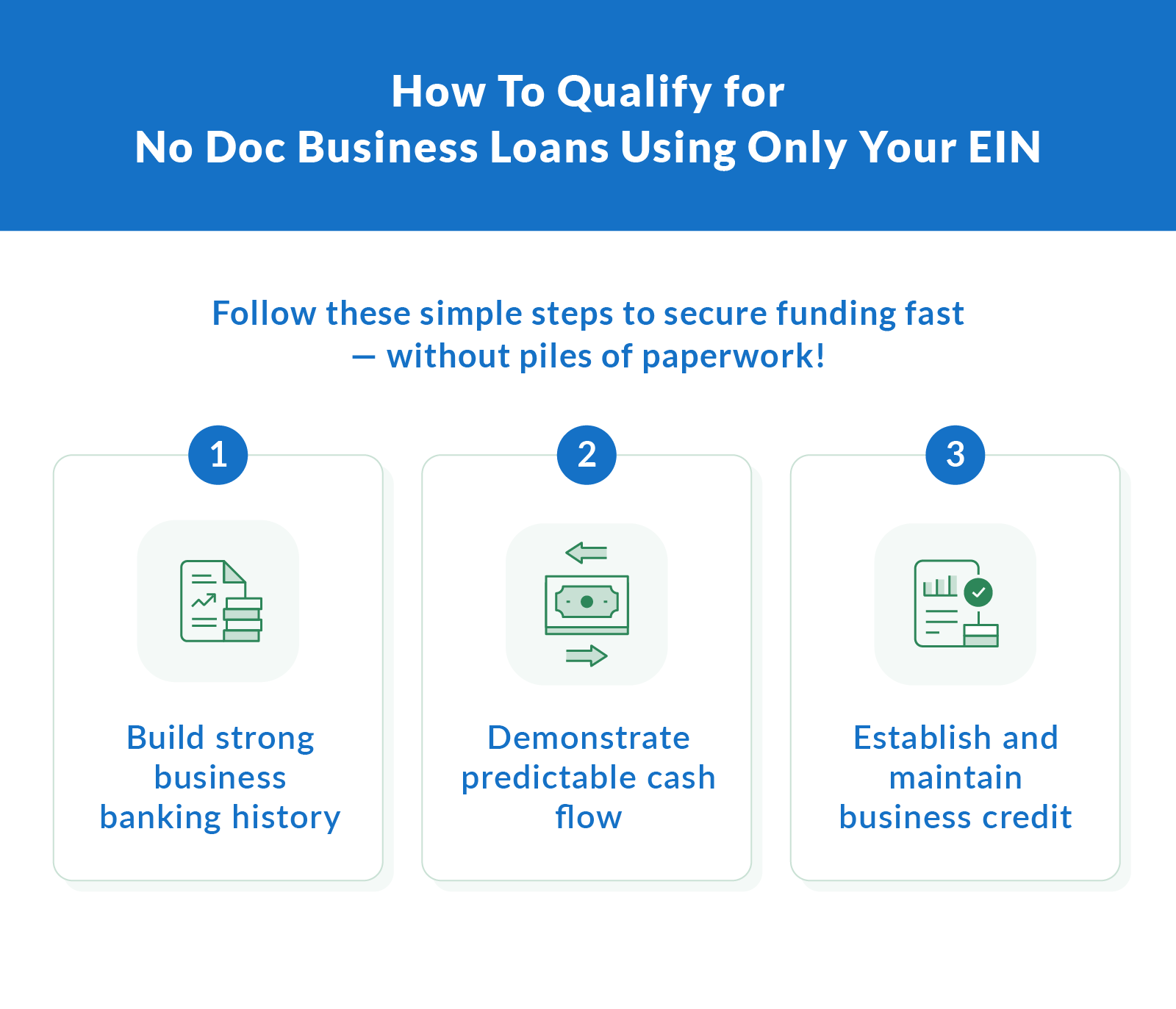

How To Qualify for No-Doc Business Loans

When lenders can't rely on things like tax returns and personal credit scores, they tend to focus instead on a few key factors:

Banking activity and history: Lenders will want to see if you've taken out other loans or financing options in the past, and if so, how you handled repayment and money management.

Cash flow and deposit patterns: Looking at the way cash flows in and out of your business will tell lenders how reliably your business generates and manages income.

Business credit: If you have a business credit profile, it can help demonstrate how your business handles financial obligations independently of your personal credit.

Revenue consistency: Lenders want to see steady or predictable revenue over time, rather than large fluctuations.

If your business is lacking on any of these, spend time figuring out how you can build a strong business banking history, demonstrate predictable cash flow, and establish business credit before applying for EIN-only/no-doc business loans.

Clarify Customer Testimonial: Scaling Faster Than Revenue

At Clarify Capital, we're dedicated to helping businesses not only survive, but grow. Listen to a real customer talk about his experience using Clairfy for a business loan.

Pros and Cons of EIN-Only Loans

All loan options have benefits and trade-offs. Let's be clear about them with EIN-only and no-doc financing:

| Pros | Cons |

|---|---|

| Relatively fast approval time | Higher interest rates |

| Minimal paperwork | Smaller loan amounts |

| No hard personal credit pull (can vary) | Shorter repayment terms |

| Less risk to personal finances (but personal guarantees may still be required) | May cost more than other financing |

How They Compare to Traditional Business Loans

Compared with traditional loans such as SBA loans or bank-provided term loans, no-doc EIN-only options are more accessible for borrowers without years of tax returns and extensive financial statements. That said, they also typically come with higher interest rates, shorter repayment terms, and smaller loan amounts.

| EIN-Only Loan vs. Traditional Business Loan Requirements | ||

|---|---|---|

| Criteria | Traditional loans | EIN-only loans |

| Personal credit score | Required (most lenders check FICO score, usually 550 to 650 minimum) | Not usually required (some may do a soft pull) |

| Tax returns | Typically required | Not required |

| Financial statements | Typically required (profit and loss statements, balance sheets) | Not required in most cases |

| Bank statements | Reviewed to verify cash flow and account activity | Required (primary method for evaluating cash flow) |

| Personal guarantee | Often required, especially for small or new businesses | Sometimes required, depending on lender and risk |

| Collateral | May be required | Not usually required (depends on loan type) |

| Business plan | Required (includes strategy, revenue projections, and market research) | Not typically required |

Other Loan Options

Depending on your business and situation, traditional financing might make more sense. They tend to offer lower rates, larger amounts, and longer terms. You might just meet more qualifications than you think. Here are some other options.

SBA Loans

SBA loans are designed for small businesses and are backed by the Small Business Administration (SBA), a government agency that aims to expand loan access for more small businesses. The SBA guarantees part of the loan, which makes this option one of the best for low interest rates and longer repayment periods.

Those benefits also mean they're harder to qualify for. Lenders look for solid financials and established business history, which often includes credit. They're often referred to as the benchmark for affordable business financing, even though they aren't realistic for every borrower.

The SBA 7(a) is one of the most common types of SBA loans, and can be used for working capital, expansion, or refinancing. SBA Microloans are another type of financing that is generally for smaller amounts (typically up to $50,000) and designed for startups or early-stage businesses.

Term Loans

Term loans are provided by lenders as a lump sum and repaid with a set APR over a set period of time.

There are short-term loans, which are paid back in a shorter window (usually anywhere from six to 36 months) and are typically more expensive. There are also long-term loans, which are harder to qualify for but offer better rates, higher loan amounts, and longer terms in general.

Business Line of Credit

A business line of credit is similar to a credit card. It allows you to spend up to a certain amount of money on a revolving basis, and you only pay back and accrue interest on what you use in a given period.

They usually have lower interest rates than regular credit cards, and using one can also be a great way to build back up your personal credit score if it's low (if the lender reports payment activity to credit bureaus). This type of funding is very flexible, so it can be used for a variety of expenses, and you won't be charged for paying back your balance early. The main caveat is that qualifying can still be challenging, especially for higher limits, and rates can increase quickly depending on usage.

You deserve low rates and an honest lender who has your back.

From our humble beginnings in 2018, we remain committed to helping businesses achieve success regardless of their credit score. We keep things simple, convenient and transparent Read our manifesto →

FAQs About EIN-Only/No-Doc Loans

I know loan information can be overwhelming. Here, I've gathered and answered some of the questions I get most about bad-credit loans.

Can You Get a No-Doc Business Loan?

It's important to understand that "no-doc" actually just means fewer documents and a fairly easy application process. It refers to lending options where documents like tax returns and profit and loss statements (P&Ls) aren't required, but things like bank statements and a soft check of your personal credit most likely still are.

Can I Get a Loan With My EIN Number?

Usually, you'll need more than your EIN alone. But you can find lenders who focus on your business's revenue and cash flow rather than your personal credit score.

What Credit Score Is Needed for a No-Doc Loan?

There's no universal minimum, but a lot of lenders look for a personal credit score of at least 500 to 600. Stronger credit will almost always lead to better rates and terms.

What Is the Trump Small Business Grant?

There isn't currently a specific "Trump small business grant." There were pandemic-era relief programs like the Paycheck Protection Program (PPP) and Economic Injury Disaster Loans (EIDL), but they're no longer widely available.

Can I Get a Business Loan With an LLC With Bad Credit?

As always, it depends on your scenario. LLCs can qualify for business loans with low credit scores, but options will likely be more limited. Most lenders will look at a combination of your personal credit, business revenue, and time in business. Online and alternative lenders are usually more flexible.

What's the Minimum Credit Score I Need To Qualify for a Business Loan?

It depends. Not all financing options focus on credit score, as I discussed in this article. For those that do, some lenders go as low as 500, but better credit will mean better terms.

How Much Is a Down Payment for a Loan?

Many no-doc or EIN-only financing options don't require a traditional down payment, but some products (like equipment financing) may require 10% to 20% up front, depending on the lender.

How Does Clarify Capital Protect My Business and Financial Information?

Clarify Capital follows SOC 2 security principles designed to protect sensitive business and financial information. This includes safeguards such as secure data handling practices, controlled access to information, and ongoing monitoring to help protect your data throughout the application and funding process.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts