When applying for a secured loan, one of the biggest factors affecting approval and terms is the item of value you offer as collateral. In short, collateral means the asset a borrower pledges to a lender to secure a loan. If the borrower can’t keep up with payments, the lender can seize that item to recover losses.

The types of collateral you provide directly impact the interest rates, repayment timeline, and total borrowing cost. A home, for example, can help lock in a much lower rate than your business inventory or a personal vehicle. Whether you’re applying for a collateral loan or trying to refinance, the right asset could make a major difference in the repayment of a loan.

Lenders evaluate several factors when accepting collateral — its market value, how easily it can be sold, and how closely its value matches the loan amount. Understanding the most common forms of collateral and how lenders view them can give you a strategic edge when applying for financing.

What Is Collateral?

Collateral is something of value that a borrower pledges to a financial institution as a backup in case they can’t repay a loan. If the borrower defaults, the lender can take ownership of that asset and sell it to recoup the money owed.

In lending terms, the collateral meaning is simple: It’s a form of protection for the lender. It creates a security interest, which means the lender has a legal right to claim the asset if the loan isn’t repaid.

The type of collateral you offer depends on the type of loan you’re applying for. For example, a mortgage is backed by real estate, while a business loan might be backed by equipment or receivables. In all cases, the asset helps secure the repayment of a loan and may improve your chances of approval or lower your cost of borrowing.

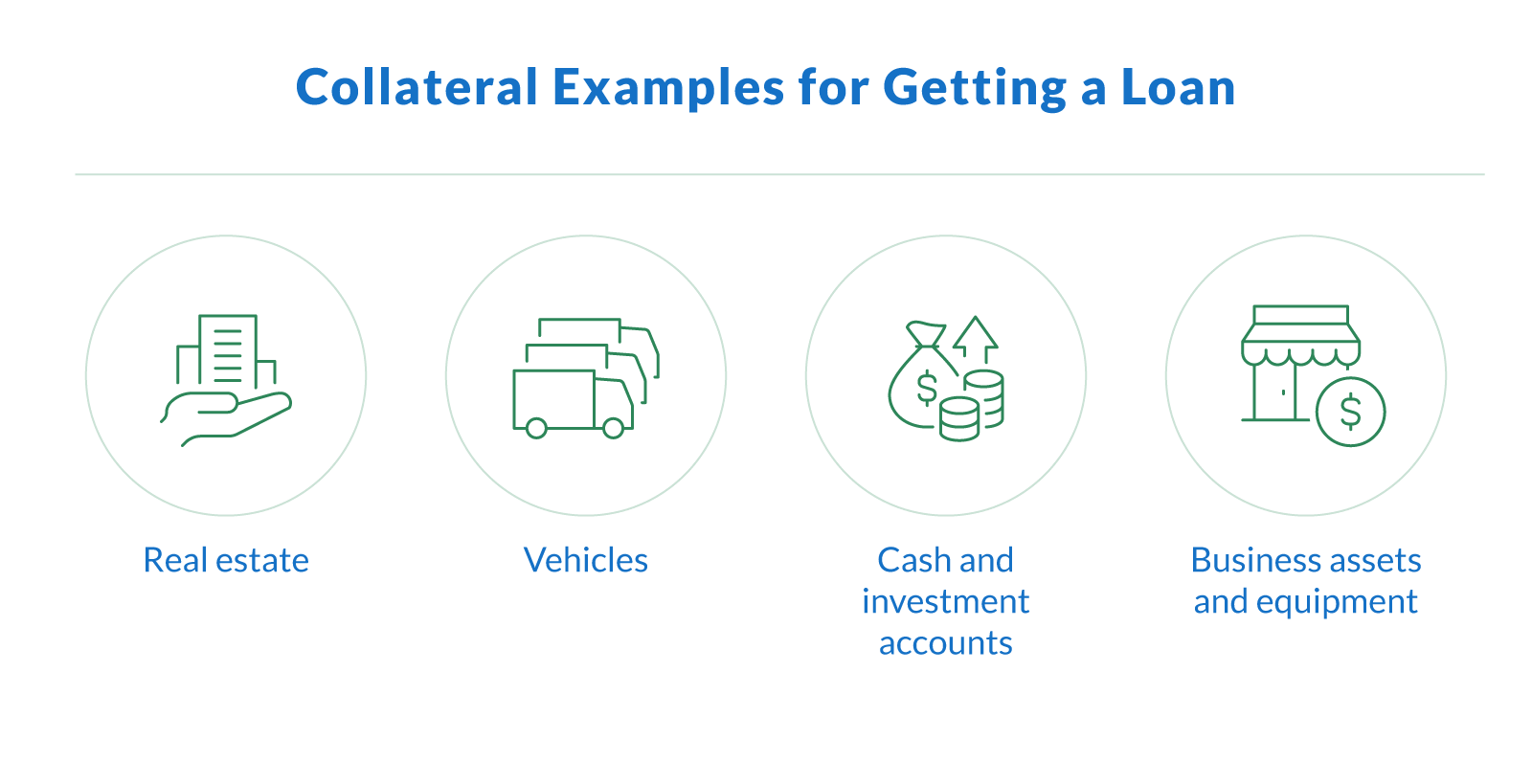

Examples of Collateral in Different Types of Loans

Collateral can take many forms, and the value and stability of the asset often determine how favorable your loan terms will be.

Real Estate

Real estate is one of the most common and valuable examples of collateral. Homes, commercial buildings, and undeveloped land are often used to secure a mortgage loan or business financing. Because real estate typically retains value and can be resold, lenders view it as a low-risk item of value. For example, a borrower might use their home to back a mortgage loan, or a business owner might use a warehouse as collateral for a secured loan.

Vehicles

Cars, trucks, and other motor vehicles are often used to back a car loan, personal loan, or even a business loan. These assets can be repossessed and sold by the lender if the borrower defaults. While vehicles depreciate faster than real estate, they are still commonly accepted as collateral. A business might pledge delivery vans to secure a short-term collateral loan, or an individual may use a personal car to qualify for lower interest rates on a secured loan.

Cash and Investment Accounts

Savings accounts, certificates of deposit (CDs), stocks, and bonds are strong examples of collateral because they’re easy to liquidate. When a borrower uses financial accounts to secure a loan, they typically receive lower interest rates due to the low risk involved for the financial institution. For instance, a borrower might use a $50,000 investment portfolio to back a collateral loan for business expansion.

Business Assets and Equipment

Companies often use business equipment, inventory, and accounts receivable to secure a commercial or secured loan. These assets serve as proof of value and revenue potential. For example, a manufacturer may use industrial machinery as an item of value for a working capital loan. Or, a retailer may pledge inventory and unpaid invoices to get fast funding through invoice factoring.

How Collateral Affects Loan Terms

Collateral has a direct impact on the cost and structure of your loan. In general, a secured loan backed by a valuable asset may offer better terms than unsecured loans (such as those you can get through Clarify Capital), which rely more heavily on the borrower’s revenue or credit history.

When you offer collateral, lenders take on less risk. That often leads to lower interest rates, higher loan amounts, and more flexible repayment terms. In contrast, unsecured loans come with higher interest rates because there’s no asset backing the repayment of a loan.

Borrowers with a strong credit history can qualify for good terms on unsecured loans, but pledging a high-value item — like real estate or investment accounts — might get them better terms with a secured loan. Among all types of collateral, real estate and cash accounts tend to bring the best rates and approval odds because they’re stable and easy for a financial institution to recover if the borrower defaults.

Collateral Issues: Risks and Considerations for Borrowers

While offering collateral can improve your loan terms, it also comes with risks. The biggest concern is that if the borrower defaults, the lender has the right to seize the asset. That could mean losing property, business equipment, or cash accounts if you fall behind on payments.

Lenders also evaluate the value of collateral relative to the loan amount. If the asset is worth less than the requested loan, the lender may reject the application or approve a smaller amount. This is why it’s important to know the fair market value of the item of value you’re offering.

Financial institutions look for collateral that’s easy to appraise, holds value over time, and can be quickly resold if needed. Borrowers should weigh the benefits of a secured loan against the risk of losing essential assets during the repayment of a loan.

Alternatives to Collateral Loans

Not every business owner has valuable assets to pledge for financing. Fortunately, there are several options that don't require collateral but still offer competitive terms. These alternative financing solutions focus more on your revenue and business performance than physical assets:

Unsecured business loans. These loans don't require collateral, making them accessible for businesses without significant physical assets to pledge.

Business lines of credit. Access flexible financing with revolving credit based on your business performance rather than physical collateral.

Working capital loans. Designed specifically for day-to-day operations, these loans typically evaluate your business revenue instead of requiring collateral.

Merchant cash advances. Get funding based on your future credit card sales, with repayment that adjusts based on your daily revenue rather than requiring assets.

For businesses seeking financing without risking valuable assets, Clarify Capital offers all these alternatives with a quick two-minute application process and funding possible in as little as 24 hours.

FAQ: Understanding the Meaning and Usage of Collateral

Here are answers to some of the most common questions about collateral — in both financial and everyday contexts.

What Does Collateral Mean in Simple Terms?

Collateral refers to an item of value a borrower pledges to a lender as a form of protection in case they can’t repay the loan. It gives the lender a security interest in that asset, meaning they can take possession of it to recover their money if needed.

The collateral meaning is straightforward: it’s an asset used to reduce risk for the lender when approving a loan.

Example sentences:

The borrower used their car as collateral for a personal loan.

A financial institution may require collateral to back a large business loan.

Collateral helps secure the repayment of a loan if the borrower defaults.

What Are Some Examples of Collateral?

Common examples of collateral include:

Real estate. Homes and commercial properties are often used in a mortgage loan or business loan to secure funding and reduce risk for the lender.

Vehicles. Cars or trucks can be pledged in a car loan or secured personal loan, giving the lender a claim to the asset if the borrower defaults.

Cash and investment accounts. Savings, stocks, or bonds can be used as collateral to help qualify for lower interest rates and improve loan approval odds.

Business assets. Equipment, inventory, and accounts receivable are commonly used in a secured loan to show repayment ability and reduce lender risk.

The type of item of value offered can affect approval odds, repayment terms, and the overall cost of borrowing. Financial institutions usually offer better terms when the collateral is stable and easy to liquidate.

What Is the Synonym of Collateral?

Several synonyms can be used for "collateral," depending on the context. In financial terms, these include:

Security

Guarantee

Pledge

Asset

Surety

In a general context, "collateral" might also be replaced with broader terms like “support” or “proof.” Referencing a thesaurus or word list can reveal new words that fit specific usage.

Example sentences:

The loan required a financial guarantee.

She offered her property as a pledge for the loan.

What Is the Origin of the Word "Collateral"?

The word "collateral" comes from the medieval Latin collaterālis, a combination of com- (meaning "together" or "with") and laterālis (meaning "side"). It originally referred to something that is situated side by side or indirectly related.

Over time, especially in American English, the term took on a financial meaning — referring to an asset offered alongside a loan agreement. The word’s common ancestor language, Latin, influenced its adaptation into legal and banking terms we use today.

What Does "Collateral Damage" Mean?

"Collateral damage" is a phrase used to describe unintentional harm or loss that occurs as a byproduct of a larger action, often in military settings. It has also become common in figurative use, describing unintended consequences in areas like politics or business.

Example sentences:

Civilian casualties are often referred to as collateral damage during conflict.

The policy change led to job cuts as collateral damage.

This term is well-recognized in American English and regularly appears in discussions about war, ethics, and policy. It’s also found in dictionaries of new words due to its expanded metaphorical use.

How Is "Collateral" Used in Different Contexts?

The word "collateral" is not limited to finance. Here are a few examples of how it shows up across different fields:

Marketing collateral. Brochures, ads, and digital assets are used to promote a product or brand and support sales efforts.

Collateral evidence. Supporting material or facts help prove a point in legal or academic settings and strengthen an argument or case.

Finance. An asset can be used to secure a loan from a financial institution, reducing the lender’s risk and improving the borrower’s loan terms.

Credit cards. While most are unsecured, some secured credit cards require cash collateral to open an account and establish a credit limit.

These usages show how language evolves from a common ancestor and adapts to meet the needs of different industries. In some cases, the word also functions as an adverb or adjective, depending on context.

Get the Best Loan Terms With Clarify Capital

Collateral plays a major role in helping borrowers secure better loan terms. Whether you’re pledging real estate, equipment, or cash, the right item of value can lower your interest rates and increase your approval chances with a financial institution. Choosing the right types of collateral can lead to a more affordable and flexible secured loan while protecting the lender in case of missed payments.

However, you don't need to offer collateral to get a loan with great terms. If you’re weighing loan options, it’s smart to assess your available assets and work with a trusted advisor to determine what’s best for your business. To explore funding opportunities tailored to your needs, apply for revenue-based financing with Clarify Capital today — it only takes two minutes.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts