Timing matters when deciding to refinance business loans. If done right, you pay lower interest rates, improve repayment schedules, and free up working capital, demonstrating some of the biggest benefits of refinancing. This gives small business owners more room to breathe and grow.

Whether you're looking to cut monthly payments, streamline multiple loans, or secure funding for expansion, refinancing can be a smart financial move.

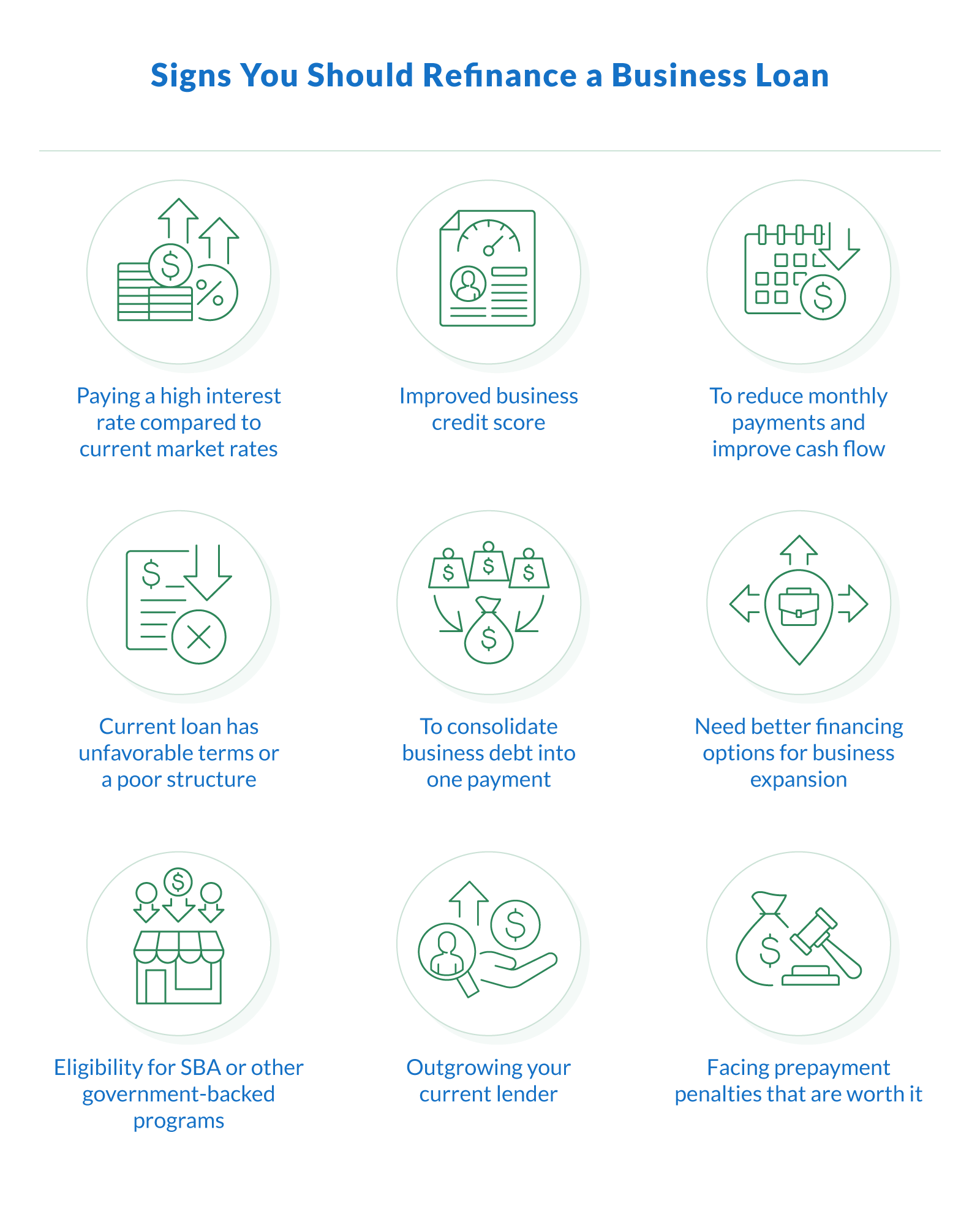

This article breaks down nine key signs that it might be time to refinance your current loan. You'll learn how to evaluate your financial situation, compare your options, and determine if refinancing can boost your cash flow and support long-term goals.

1. Are You Paying a Higher Interest Rate Compared to the Current Market Rates?

In today's market, small business loan interest rates with traditional banks generally carry rates up to 11.5+% for prime borrowers, while SBA loan rates — which are typically tied to the prime rate plus a margin — often range from roughly ~8%–13% depending on the program and lender. If your current loan is higher, refinancing could lower your payments and reduce your borrowing costs.

Fixed rates may be higher than current rates, and variable rates can spike, so switching to a more competitive rate can reduce your cost of borrowing.

Suppose your existing loan has a 12% interest rate on a $100,000 balance with a five-year term. Refinancing to a 7% rate could save you roughly $14,000 in interest over the life of the loan and lower your monthly payment by about $240.

Clarify Capital typically offers rates starting as low as 6%, depending on credit and financials.

2. Has Your Business Credit Score Improved Enough To Refinance?

When you plan to refinance a business loan, make sure your business banking records are up to date, as lenders often review bank statements. A stronger credit score opens the door to better financing options.

Whether it's your business credit score or personal credit score, lenders see improved credit as a sign of lower risk. That can make you eligible for refinancing at more favorable rates and terms. Many lenders, including Clarify Capital, consider a minimum credit score of 500 for a business loan, but higher scores often unlock better offers.

Don't let a bad credit score keep you from getting funded. Check your eligibility with a quick Clarify Capital loan application.

3. Do You Want To Reduce Monthly Payments and Improve Cash Flow?

If your current loan is putting a strain on day-to-day operations, refinancing could be a way to ease pressure. Switching to a lower interest rate or moving to longer terms can result in lower monthly payments, giving you more flexibility to manage working capital. Improving your repayment terms can help meet short-term business needs, reinvest in growth, or build a stronger financial cushion without sacrificing cash flow.

When traditional loan terms feel restrictive, a merchant cash advance (MCA) may provide temporary liquidity while you pursue refinancing, though they often come with higher costs.. MCAs offer repayments tied to daily or weekly sales, giving your business flexibility to manage cash flow during the transition.

4. Does Your Current Loan Have Unfavorable Terms or a Poor Structure?

Some loans come with features that aren't well-suited for your business, such as balloon payments, very short repayment schedules, or payment timing that doesn't match your revenue cycle. These unfavorable terms can hurt your financial situation over time. Refinancing gives you the opportunity to restructure the loan for a better fit.

With Clarify Capital, repayment schedules vary by product and may be flexible and designed to align with your cash flow, helping you stay on track without added stress.

5. Could Consolidating Your Business Debt Simplify Payments?

Is your business juggling multiple debts? Refinancing can simplify things. Debt consolidation allows you to replace several high-interest debts with one refinanced loan at a lower rate, rolling balances from business credit cards, lines of credit, and other loans.

Consolidation makes payments easier to manage and may reduce total borrowing costs depending on the new loan terms. By consolidating existing debt into a single monthly payment, you gain better control of your cash flow and create a clearer path to becoming debt-free.

6. Are You Expanding and Need Better Financing Options?

Growth takes capital — and refinancing can help unlock better business financing. Small Business Association (SBA) programs are designed to support expansion through long-term, affordable financing. Term loans provide a lump-sum up-front payment with fixed repayment terms, making them useful for buying equipment, investing in commercial real estate, or funding business growth.

You can also explore flexible funding through a business expansion loan with Clarify Capital to meet your evolving business needs.

7. Are You Eligible for SBA or Other Government-Backed Loans?

An SBA loan often offers more favorable terms than conventional financing, including lower interest rates and longer repayment schedules. If your business now qualifies for SBA-backed programs like the SBA 504 or SBA 7(a), refinancing into one of these options could improve your financial position significantly. The loan application process is more structured and typically requires additional documentation, but the payoff is access to a reliable loan program supported by the Small Business Administration.

8. Have You Outgrown Your Current Lender's Offerings?

As your business grows, your financial needs may evolve beyond what your current lender can provide. You could need larger loan amounts, extended repayment schedules, or access to specialized financing.

Clarify Capital offers a wider range of refinancing options, great customer service, and competitive rates tailored to your needs. We compare your loan options across multiple lenders to get you competitive rates and find a financing partner that truly supports your long-term goals.

9. Are Prepayment Penalties Still Worth Refinancing Your Loan?

Some original loans include prepayment penalties, but that shouldn't automatically stop you from refinancing. If the long-term savings from a new loan with lower interest rates outweigh the short-term cost of the penalty, refinancing can still be the right move.

For example, if refinancing saves you $10,000 in interest, but your prepayment penalty is $2,000, the net benefit is clear. Always calculate the total amount saved and weigh it against your remaining repayment timeline.

Refinancing vs. Restructuring: Which One Fits Your Situation?

Before jumping into loan refinancing, it's important to determine whether you really need refinancing or simply a loan restructuring.

Refinancing replaces your existing loan with a new one, often with better terms, such as a lower loan interest rate, extended repayment period, or access to additional capital. Borrowers usually refinance to improve affordability, consolidate debt, or support growth.

Meanwhile, restructuring keeps the same loan but changes the terms. Restructuring is typically used when businesses need temporary relief from unfavorable terms or short-term financial pressure.

Here's a quick overview of how loan refinancing and restructuring compare.

| Refinancing vs. Restructuring | ||

|---|---|---|

| Factor | Refinancing | Restructuring |

| Definition | Replace the existing loan with a new loan | Modifies the terms of your current loan |

| Purpose | Savings, consolidation, growth opportunities (like equipment loans or real estate loans) | Temporary cash-flow pressure |

| Impact | Long-term solution | Short-term relief |

| Repayment period | Can extend or shorten depending on the new structure | Modified within the current loan (may be temporary or permanent) |

| Credit impact | May require a credit check or underwriting (new loan) | Minimal impact on credit since it modifies the current loan |

| Closing costs | May involve closing costs (origination, underwriting, legal, or appraisal fees) | Usually minimal or none, since no new loan is created |

Restructuring suits businesses facing financial stress and in need of a short-term solution. But for those seeking long-term stability, refinancing a loan is often the better option.

Now that you have a clearer sense of your financing path, make sure you're fully prepared. Use this small business loan checklist to get organized and make your application process smoother.

Know When To Make the Move

Recognizing the right time to refinance a business loan can save you money, improve cash flow, and give your company the breathing room it needs to grow. Small business owners who take a proactive approach to loan management can often reduce their financial burden while unlocking better loan terms.

If refinancing sounds like the right move for your business, start your application with Clarify Capital to compare options and build a repayment plan that supports your financial situation.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts