No Collateral Required

Business Loans Up to $5M

Get funded in as little as 24 hours with rates starting at 6% APR. Fast online application takes just 2 minutes.

Total Funded

$1B+

Businesses Served

50,000+

Average Funding Time

24 hrs

Won't affect your credit score

When you’re getting a small business loan from a bank, the paperwork can feel endless. You need tax returns, profit and loss (P&L) statements, a 12-month cash flow projection, balance sheets, and business plans. And even once your paperwork is submitted, you're often stuck waiting weeks just to find out you don’t qualify anyway.

If you need a loan but don't have time for the paperwork, a no-doc business loan might be a good option. They cut paperwork down to the basics so you can move fast when your business needs cash.

Below, I'll cover what "no doc" really means, which loans actually fit the no-doc label, and how to spot lender red flags.

What "No Doc" Means

A “no-doc” loan is really a “low-doc” loan. You still have to submit some documents, but the good news is that you're skipping the heavy stuff banks ask for, like tax returns, full financial statements, business plans, and projections. Here's what gets cut and what's still on the table.

| What's not required | What's still checked |

|---|---|

| Tax returns | Three months of business bank statements |

| Profit and loss statements | Personal credit score |

| Balance sheets | Business ownership and ID |

| Business plans | Time in business and industry |

| Cash flow projections | Monthly revenue |

No-Doc Business Loan Options

Not every loan type works as a no-doc option. Here's a quick comparison so you can see how they stack up.

| Loan type | Funded in | Borrow up to | Rate | Best for |

|---|---|---|---|---|

| Short-term business loan | As fast as same-day | $10,000 to $5M | Starting at 6% APR | Lump-sum needs with a clear repayment plan |

| Business line of credit | As fast as same-day | Up to $5M | Starting at 6% APR | Ongoing or unpredictable expenses |

| Merchant cash advance (MCA) | As fast as same-day | Up to $5M | Factor rate 1.08 to 1.45 | Businesses with strong card sales |

| Invoice factoring | 1 to 2 weeks | Up to 100% of invoice value | 0.5% to 5% per invoice per month | Business-to-business (B2B) companies with slow-paying clients |

| Equipment financing | 1 to 5 days | 100% of equipment value | Starting at 6% APR | Buying or leasing machinery and vehicles |

The rates and terms I've shown above are just starting points. Your actual offer depends on your credit, revenue, and time in business.

Types of No-Doc Business Loans

Each of these financing options handles low documentation differently. Here's what to know about each one.

Short-Term Business Loans

A short-term business loan gives you a lump sum that you pay back over six to 36 months, usually through weekly, biweekly, or monthly payments.

For most short-term loans through Clarify, three months of bank statements are enough to apply. Rates start at 6% APR for qualified applicants, and you can borrow from $10,000 up to $5M, depending on your revenue. These work well when you've got a one-time expense and a clear plan for paying it back.

Business Line of Credit

You can draw funds from a business line of credit, pay them back, and draw again up to your limit. You only pay interest on what you actually use.

Rates start at 6% APR, and funding can be as fast as same day. Like short-term loans, the application is bank-statement driven. You don't need tax returns or financial statements to get approved.

In my experience, lines of credit are the go-to for businesses with unpredictable cash flow. If you don't know exactly when you'll need money or how much, this gives you flexibility without committing to a single lump sum.

Merchant Cash Advance

A merchant cash advance, or MCA, is an advance against your future sales. You get cash up front, and you pay it back as a percentage of your daily, weekly, or monthly card sales.

MCAs are one of the fastest options on the list. Funding can hit your account as fast as the same day. Pricing is set with a factor rate, usually between 1.08 and 1.45, instead of an APR.

MCAs can be expensive, and the daily payment structure can squeeze cash flow if your sales drop. But if you've got steady card volume, they're an option that doesn't ask for much paperwork.

Invoice Factoring

With invoice factoring, you sell your unpaid invoices to a factoring company and get most of the value up front, up to 100% of the invoice amount.

Factoring is paperwork-light because the invoices are the underwriting. The factoring company is evaluating your customers' ability to pay, not yours. Setup typically takes one to two weeks, and fees run 0.5% to 5% per invoice per month the invoice is outstanding.

Equipment Financing

Equipment financing covers the cost of vehicles, machinery, technology, and other business gear. The equipment itself acts as collateral, which keeps the documentation light.

Clarify funds equipment loans in one to five days, with terms from 12 to 72 months and rates starting at 6% APR. You can finance up to 100% of the equipment's value.

What You'll Still Need To Provide

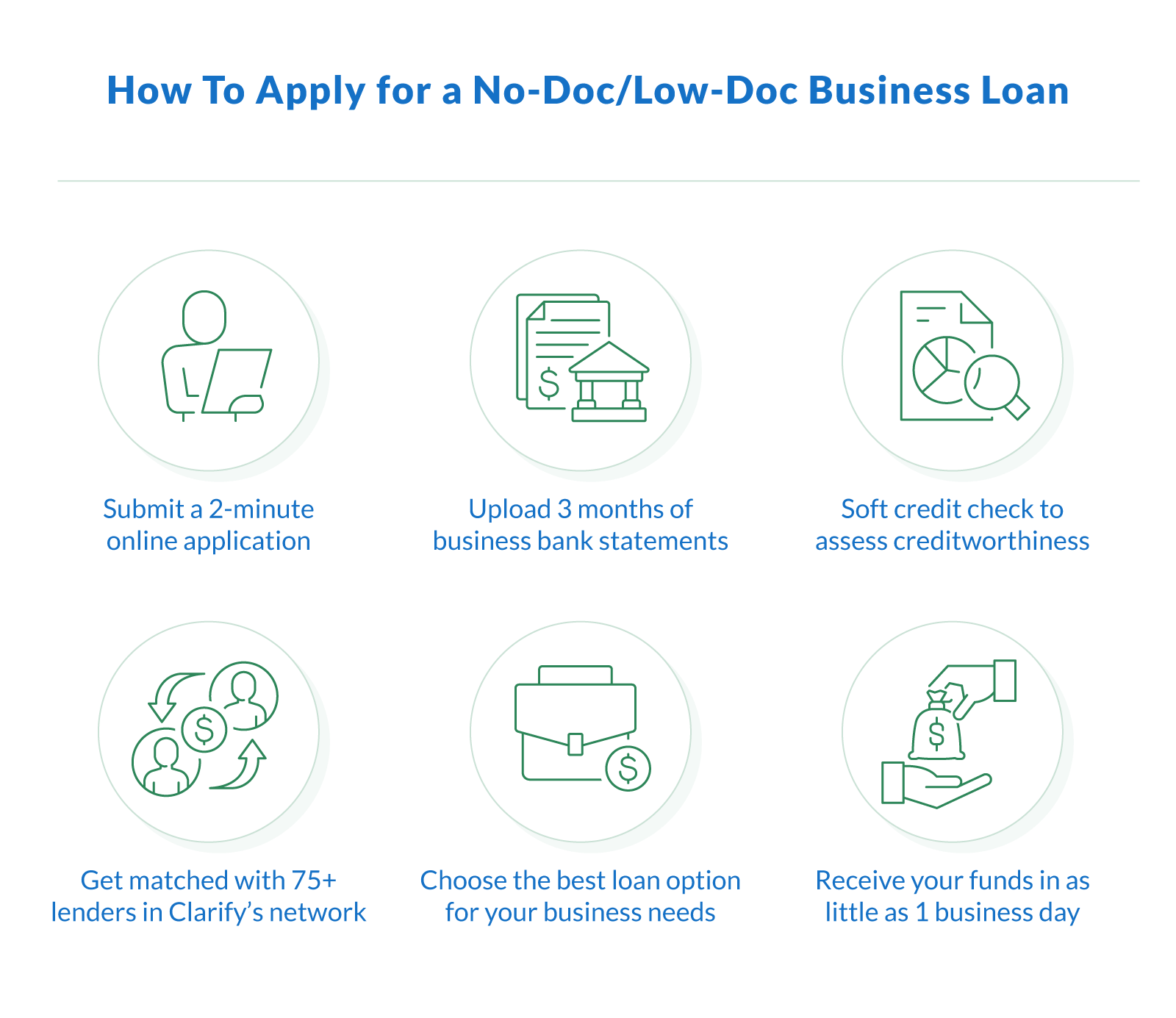

Expect to provide a few basics, even with no-doc loans. The entire application process takes about two minutes. Here's what to have ready before you apply.