Most business loans require a personal credit score of at least 550 to 680 to qualify for business loans and financing (the exact minimum will depend on the lender and loan type).

Small Business Administration (SBA) loans, for example, typically require a score of at least 640 or higher, while traditional bank term loans expect to see a 680+, and online and alternative lenders can finance borrowers with scores as low as 500 to 550.

That said, factors like strong revenue, longer time in business, and available collateral can help to offset a lower credit score in almost every case.

If you're a small or midsize business owner exploring financing options, your credit score shapes what you can borrow. Here, I'll show you the factors that go into a credit score, what you can realistically qualify for at each score range, and your options if you have bad credit.

How Do Credit Scores Work?

A personal credit score is a numerical value that indicates how “creditworthy” you are to potential lenders. If you have a low score, it signals to lenders that you're more likely to be a bad borrower; someone who misses payments or defaults on a loan. If you have a high score, it indicates you're more likely to be a low-risk and responsible borrower; someone they can count on to repay their loan according to its terms.

A credit score is not something you sign up for or opt in to. If you have ever had a credit card or borrowed money in any capacity, you automatically have a credit score (though it can take several months of reported credit activity to generate one at first).

Three major credit bureaus (Experian, Equifax, and TransUnion) collect information about borrowing history from lenders and credit card issuers, and then share that info with credit scoring companies to calculate credit scores.

FICO: The Most Common Scoring System

A company called FICO is probably the most well-known scoring system. A FICO score ranges from 300 to 850, and within that range, there are certain tiers:

| Tier | Score range |

|---|---|

| Poor | <580 |

| Fair | 580 to 669 |

| Good | 670 to 739 |

| Very Good | 740 to 799 |

| Exceptional | 800+ |

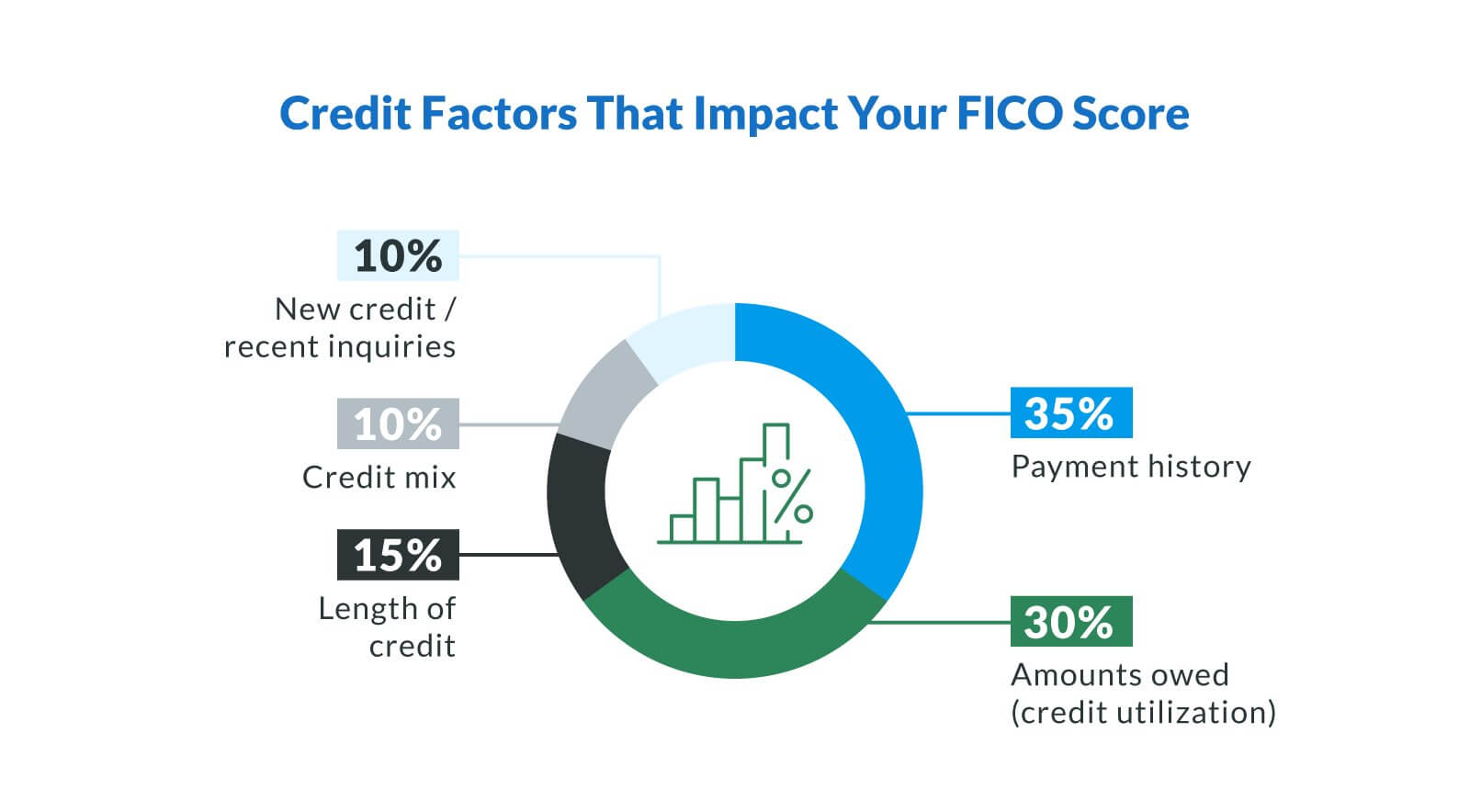

FICO scores are calculated using five different credit factors, and each factor counts a different amount toward the score.

Your Loan Options By Credit Tier

Here's a more general basis of what constitutes a good or bad score, and what you can expect to be eligible for based on your score:

| Credit tier | Loan options | Lender types | Expected APR range | What to expect |

|---|---|---|---|---|

Excellent (750+) | SBA 7(a) and 504, traditional bank term loans, bank lines of credit, the best business credit cards | Banks, credit unions, SBA-approved lenders, top-tier online lenders | SBA: 9.75% to 13.25%; bank term loans: 7% to 11% | Best rates, longest terms, largest amounts, fastest decisions across all lender types |

Good (680-749) | SBA loans, traditional bank term loans, online term loans, lines of credit, equipment financing | SBA-approved lenders, banks, online lenders | SBA: 9.75% to 13.25%; banks: 7% to 12%; online: 8% to 18% | Strong approval odds; competitive but slightly higher rates than excellent tier; full menu of loan options available |

Fair (580-679) | Online term loans, short-term loans, lines of credit (limited), equipment financing, Microloans | Online lenders, alternative lenders, some credit unions | Online: 10% to 30%; equipment: 8% to 25% | Limited options at banks; online lenders likely; revenue, time in business, and collateral matter more than credit alone |

Poor (<580) | Merchant cash advances, invoice factoring, short-term loans, secured loans, Microloans | Alternative lenders, factoring companies, MCA providers | MCA: factor rates 1.08 to 1.45; short-term: 20% to 50%+ effective APR | Few traditional options; alternative loans price for credit risk; collateral or strong receivables can unlock financing; Clarify Capital finances 550+ scores |

The Credit Score You Need for Each Loan Type

Each financing option has unique credit score requirements. Some options, like equipment financing or merchant cash advances, for example, are by nature more reliant on collateral outside of your personal assets, and therefore are more flexible on low credit scores. More traditional loan types that don't have personal guaranties or outside assets as collateral (like bank term loans) tend to be more reliant on credit score as a qualifier.

Below, I break down the credit score requirements by loan type to help give you an idea of what type of loan could be best for your business.

| Loan type | Typical minimum personal credit | Other key qualifiers |

|---|---|---|

| SBA 7(a) loan | 640+ at most SBA-approved lenders; SBA itself sets no minimum | 2+ years in business, demonstrated repayment ability, U.S.-based, "small" per SBA size standards |

| SBA 504 loan | 650+ commonly | Owner-occupied commercial real estate or long-life equipment; 10% borrower equity; job creation/retention |

| SBA Microloan | 575 to 620+ varies by intermediary lender | Up to $50,000; admin by nonprofit intermediaries |

| Traditional bank term loan | 680+ typical; 720+ for best rates | 2+ years in business, $250K+ annual revenue typical, clean balance sheet |

| Online term loan | 550 to 600+ | 6+ months in business, $10,000+ monthly revenue, 3 to 4 months of bank statements |

| Business line of credit (bank) | 680+ typical | 1 to 2+ years in business, revenue stability, DSCR 1.25+ |

| Business line of credit (online) | 600+ common | 6 months to 1 year in business, $10,000+ monthly revenue |

| Equipment financing | 550 to 630+ | Equipment serves as collateral; some lenders accept lower with stronger revenue |

| Invoice factoring | Personal score often less critical | Strength of the invoiced customer's credit; business-to-business (B2B) model; receivables to factor |

| Merchant cash advance | 500+ | Consistent credit-card sales volume; daily ACH or card receivable holdback |

| Business credit card | 670+ for best cards; some start at 580+ | Personal income often considered; revenue self-attested |

How the SBSS Score Affects SBA Loans

There's another type of score you should know about as a small or midsize business owner that's related to credit score but not quite the same.

The FICO Small Business Scoring Service (SBSS) is an application risk score used by lenders to predict the likelihood of default on small business loans. Unlike a personal FICO score, the SBSS evaluates business creditworthiness by combining personal credit data, business credit data, application data, and financial data. The SBSS range is from 0 to 300, with higher scores indicating lower risk. The general tiers of the SBSS are:

| Tier | Score range |

|---|---|

High Risk | 0 to 140 |

Moderate-High Risk | 140 to 180 |

Low Risk | 180 to 220 |

Very Low Risk | 220 to 300 |

SBA loans are some of the best financing options in the lending world, with relatively low rates and longer terms, which also makes them harder to qualify for.

Qualifying for a smaller SBA loan recently got easier.

The SBA no longer screens 7(a) Small Loans (those of $350,000 or less) against a minimum SBSS score (the SBA discontinued the SBSS prescreen for these loans on March 1, 2026). Participating lenders now underwrite these loans with their own risk models, weighing your debt-service coverage, bank statements, and projected earnings.

For you, that means a stronger path to a 7(a) Small Loan if you have solid personal credit (640+) but a thinner business credit history. Personal credit, time in business, and revenue carry more weight than any single business score.

A few things haven't changed. Lenders can still use the SBSS internally to price risk, and the SBA's general eligibility rules still apply: you operate for-profit, you're based in the U.S., you qualify as small under SBA size standards, and you can't get reasonable credit elsewhere.

The Difference Between Personal Credit and Business Credit

When we talk about “credit score,” we're usually talking about a personal credit score. But there's also something called a business credit score, which can be helpful once your business has its own credit history.

Personal Credit Scores

Personal credit scores track the individual and are linked to your personal identity. They drive the underwriting processes on many small business loans (especially those below $500,000) because business owners typically have to sign a personal guarantee, making the business owner personally liable for the loan.

The major credit bureaus track your personal credit reports: Equifax, Experian, and TransUnion.

Business Credit Scores

Business credit scores track a business entity rather than an individual. They become more important as the loan size grows or as the business credit history matures because a newly-formed LLC has no business credit history. (Lenders therefore rely entirely on personal credit, time in business, and revenue projections for the first 12 to 24 months until the LLC has reported trade lines.)

Business credit scores are based on a business's EIN, trade payment history, public records (liens, judgments, bankruptcies), and company age. Separate bureaus track them too, and each scores things a bit differently:

Dun & Bradstreet PAYDEX: Scores go from 0 to 100, based on trade payment history. An 80 or higher is "pays on time" and a 90 or higher is "pays early."

Experian Intelliscore Plus: Scores go from 1 to 100, where anything above a 76 is considered low credit risk.

Equifax Business Credit Risk Score: Scores go from 101 to 992. Equifax doesn't have official tiers, but higher scores indicate stronger borrowing potential.

FICO SBSS: Scores go from 0 to 300. Anything above 180 is a low risk.

What Lenders Evaluate Besides Your Credit Score

When lenders evaluate you for financing, your personal credit score is a big factor. But it's not the only one. Underwriting also weighs your business's revenue, time in business, debt-service coverage ratio (DSCR), collateral, and use of funds.

Time in business: SBA loans typically require two or more years in business, while online lenders can finance businesses as young as six months. New limited liability companies (LLCs) (those who have only been in business for six months or less) are limited to startup-friendly loans like Microloans, secured cards, and equipment financing tied to assets.

Annual revenue: Online lenders often want to see that your business is making $10,000 monthly revenue or more. Bank term loans typically require $250,000+ of annual revenue. The SBA itself sets no minimum, but its participating lenders apply their own thresholds.

Debt-service coverage ratio (DSCR): This is a business's net operating income divided by its total debt service. Banks typically want the DSCR to be 1.25 or higher, while SBA loans are slightly more flexible at 1.15 to 1.25.

Collateral: Equipment financing uses equipment as collateral, while commercial real estate loans use the property as collateral. Other types of unsecured term loans, lines of credit, and SBA loans under $50,000 generally don't require collateral but may have higher rates. SBA loans under $50,000 generally don't require collateral.

Use of funds: Most lenders will want to know what you plan to use the funds for as part of their underwriting process. Some loans, like SBA 504 loans, are made to be used for specific purposes like real estate and long-life equipment. SBA 7(a) loans are general-purpose loans, term loans suit one-time spends, and lines of credit best suit recurring cash flow.

Red flags on credit reports: Lenders will have a close eye out for red flags that can indicate your creditworthiness. They can include: recent bankruptcies (within two years), unpaid tax liens, defaulted SBA loans, frequent late payments (90+ days), high credit utilization (over 50%), and rapid account opening (multiple inquiries in 30 days). Lenders also flag if a personal guarantor's credit score has dropped 30 or more points in the last 6 months.

How To Improve Your Credit Score: A Realistic Timeline

If you need to improve your credit score, here's where you can start:

Pay down credit card balances. Credit utilization (the amount owed) is 30% of a FICO score. Try to pay off your credit cards to the point where they're under 30% utilization. It can take up to 30 days to see a positive impact, but the boost will be about 20 to 50 points to your score.

Dispute errors on personal credit reports. Look up your free reports on annualcreditreport.com from all three bureaus to make sure you recognize all activity. Errors can range from accounts that aren't yours to incorrect late-payment marks, and these can hurt your score. To make a dispute, follow the CFPB credit dispute guide. Credit bureaus generally investigate disputes within 30 days, and corrected errors can begin improving your credit score within 30 to 90 days.

Avoid new credit applications for six months . Every time you apply to something (a loan, credit card, etc) that does a hard inquiry on your credit score, it drops the score by two to five points. Multiple inquiries within a 30-day period can especially compound, because new credit and recent inquiries are 10% of your FICO score.

Establish trade payment history for business credit. Build business credit history by opening vendor accounts that report to the major business credit bureaus (D&B, Experian Business, and Equifax Business). Many businesses can begin establishing meaningful trade history within three to 12 months. Just make sure to pay by or before your due dates.

Pay every bill on time for six to 12 months. This is the largest single lever for increasing your credit score, but also naturally the hardest to do. Payment history makes up 35% of a FICO score, and even just six months of clean payments can recover 50 points or more (and a year can recover 80 to 100 points). By contrast, it can take six to 12 months to recover from one missed payment, 24 months for a recent bankruptcy or charge-off to start aging into a lender-acceptable range, and seven years for most negative items to drop off entirely.

Don't close old accounts. Let's say you have three credit cards, but don't use one and are thinking about closing it. Don't! Old accounts in good standing increase your average account age, which is good. When you get rid of one, it knocks down the length of your overall credit history, which is 15% of your FICO score.

Minimum Qualifications

$10,000 in monthly revenue

Your business must earn at least $10K per month in a business bank account.

500+ credit score

You can get approved with any credit score. But the better your credit rating, the better interest rates lenders offer. Your FICO score should be above 500.

Minimum six months in business

Your company should be operational for a minimum of six months. This shows business lenders that your company is sustainable and won't go out of business.

Have a business bank account

Your Clarify advisor will need three or four months of your most recent bank statements to verify income. This is just to see you're actually making $10K+ month in revenue.

Get the Business Loan That Fits Your Credit Situation

The right business loan depends less on hitting a magic credit score and more on matching your full profile (credit score + revenue + time in business + use of funds) to the right lender and loan.

SBA and bank loans favor borrowers with higher scores of 680+, online term loans and equipment financing work for those who sit at 550+, and MCAs and invoice factoring finance businesses with scores as low as 500. No matter which of those situations you're in, Clarify Capital can help you explore options.

We've gotten more than 50,000 small and midsize businesses financed and have the highest trust rating in the industry. Our application process takes two minutes and will not impact your credit score. After filling it out, you'll be linked with a dedicated lending advisor and have access to our network of more than 75 lenders.

Get started and apply through Clarify today.

FAQs About Credit Score Requirements and Business Loans

Here are answers to questions I often get about credit score requirements and how they can affect the loans your business qualifies for.

What Credit Score Is Needed for a Small Business Loan?

Most small business loans require a personal credit score between 550 and 680. SBA loans typically need a 640 or higher, traditional bank term loans expect to see a 680 or higher, and online or alternative lenders can finance borrowers with scores as low as 500 to 600 (but usually only for short-term loans, equipment financing, and merchant cash advances). Having strong revenue and a long time in business can help offset a lower credit score.

Can I Get a Business Loan With a Low Credit Score?

It's a question I hear all the time. The answer is yes, with some caveats. Bad credit business loans exist, but the options you have are significantly narrowed down. You should also expect, even within these options, to have higher rates, shorter terms, smaller borrowing amounts, personal guarantees required, and possible daily or weekly repayment cycles.

At Clarify Capital, we finance borrowers with 550+ personal credit on term loans and equipment financing, and borrowers with 500+ scores on merchant cash advances.

Can I Get a Business Loan With a 600 Credit Score?

Yes. A 600 personal FICO score can open the door to online term loans (550+ minimum), business lines of credit at non-bank lenders (600+), equipment financing (550+), invoice factoring (personal score less critical), and merchant cash advances (500+). Bank term loans and SBA loans will typically be out of reach for you until you cross 640 to 680.

Do Business Loans Check Personal Credit?

Yes, they almost always do. On most small business loans under $500,000, the lender requires a personal guarantee from any business owner who has a 20%+ stake, which means the personal FICO of the guarantor gets checked. There are some exceptions for large established companies getting business loans (over $500K with strong corporate financials) where the corporate balance sheet substitutes for a personal guarantee.

What Credit Score Does an LLC Start Out With?

A newly-formed limited liability company (LLC) has no business credit score (different from a personal credit score). Business credit bureaus (Dun & Bradstreet, Experian Business, Equifax Business) only generate a score after the LLC has reported trade payment history, public records, or active credit accounts. Most LLCs need six to 12 months of activity before a usable business credit profile exists. During that window, lenders rely on personal credit, time in business (calendar months operating), and revenue.

What Is an SBSS Score?

The FICO Small Business Scoring Service (SBSS) is an application risk score ranging from 0 to 300 that lenders use to predict default risk on small business loans up to $1 million. It combines personal credit data, business credit data, application data, and financial data. The SBA used to require participating 7(a) lenders to pre-screen applicants with a minimum SBSS of 165, but they ended that requirement on March 1, 2026. (Some lenders still use SBSS internally as a risk-pricing tool.)

How Long Does It Take To Improve My Credit Score Before Applying?

It can be faster than you might think, especially for utilization-driven improvements, but slower when improving after negative-item recovery. Paying down credit card balances under 30% utilization can show up in your score within 30 to 60 days. Disputing errors takes 30 to 90 days to improve your score. Recovering from a missed payment takes six to 12 months of clean payments. Negative items like bankruptcies or charge-offs age out over seven years but become less impactful after about 24 months. The single biggest lever is on-time payments, which makes up 35% of your FICO score.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts