Most small business owners will need outside financing at some point, whether it's to cover a cash flow gap, purchase equipment, or fund a major expansion. In 2024, 37% of small firms applied for loans, lines of credit, or merchant cash advances, and not all of them walked away with the funding they needed. Understanding how business loans work is the first step toward getting approved on terms that actually make sense for your business.

Here, I'll break down the eight mistakes that cost borrowers the most during the application process, plus the most common types of business loans and how each one works.

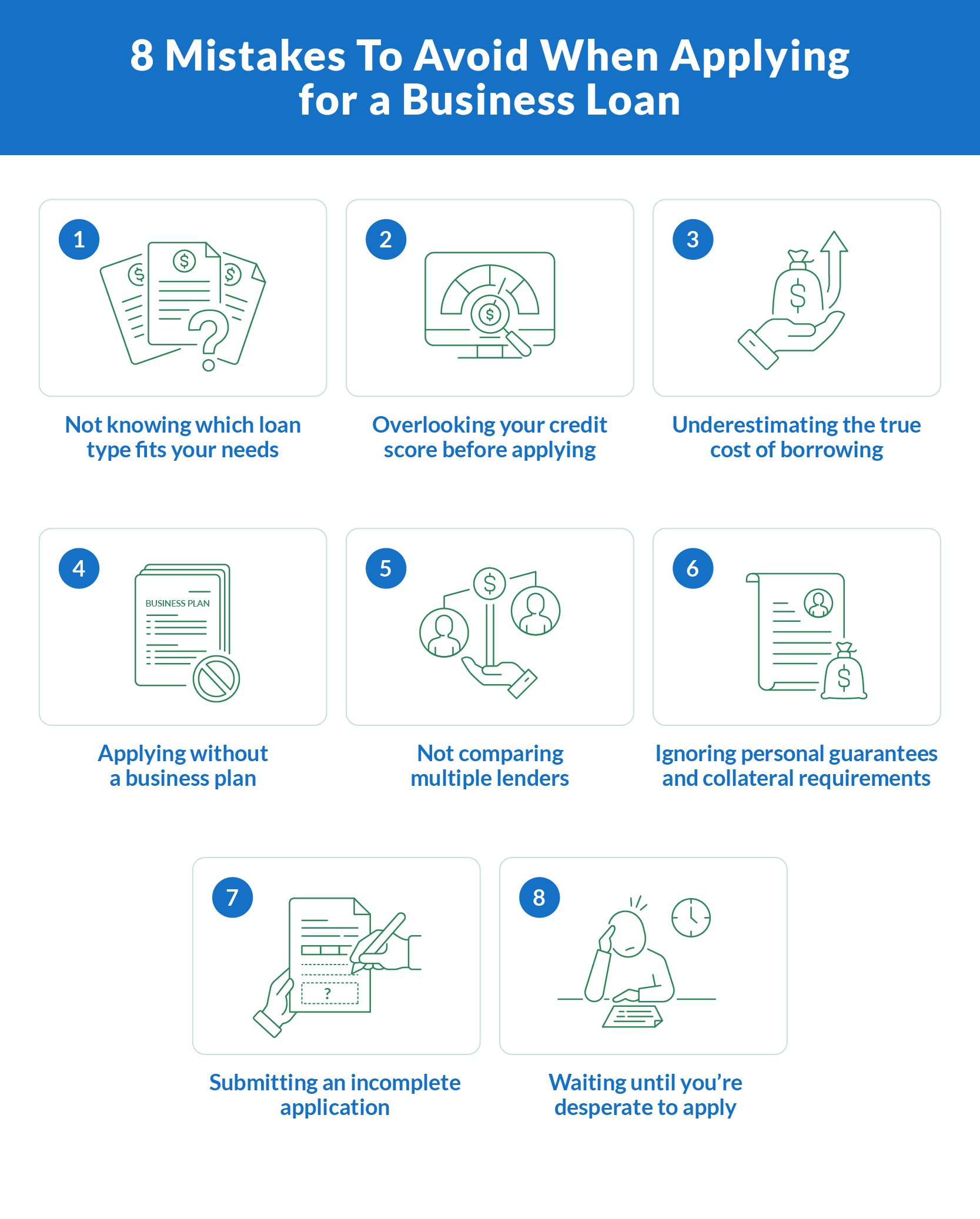

8 Mistakes To Avoid When Applying for a Business Loan

These are the most common mistakes borrowers make during the loan application. I'll show you how to avoid each one.

1. Not Knowing Which Loan Type Fits Your Needs

One of the biggest application mistakes is applying for the wrong type of financing altogether. A business that needs short-term working capital to bridge a seasonal gap shouldn't lock into a 10-year term loan. Someone buying commercial real estate should look at an SBA 504 loan, not a line of credit.

Before you start an application, match the loan type to your specific business needs and timeline. Ask yourself the following things:

Do I need a one-time lump sum or ongoing access to capital?

How quickly do I need funding?

How long will it take to repay?

The answers will narrow your financing options to the products that actually make sense for your situation.

2. Overlooking Your Credit Score Before Applying

The top reason for denial in the 2025 Federal Reserve survey was too much existing debt (cited by 41% of denied applicants in 2024, up from 22% in 2021).

Many borrowers apply without checking their credit score first, then get denied (or offered unfavorable terms) because of issues they could have addressed ahead of time. Lenders evaluate both personal credit and business credit history, and thresholds vary widely by lender type.

Traditional banks generally look for a credit score of 680 or higher. SBA lenders typically require 650 to 690, depending on the program and the individual bank. Online lenders may accept borrowers with scores as low as 500 to 600. Your creditworthiness directly affects not just approval odds but also the rates and terms you're offered. Check your personal credit report and dispute any errors before applying.

3. Underestimating the True Cost of Borrowing

Borrowers often fixate on the interest rate or monthly payment without understanding what the loan actually costs over its full term. The difference is significant. A $50,000 term loan at 10% APR over five years costs roughly $1,062 per month and about $13,740 in total interest. Stretch that same loan to 10 years, and monthly payments drop to approximately $661, but total interest nearly doubles to around $29,290.

Merchant cash advances and factor-rate products can be especially deceptive because they don't quote APR. A factor rate of 1.3 on a $50,000 advance means you repay $65,000, but the effective APR depends on how quickly you repay (and it's almost always higher than a term loan). Always calculate the total cost of borrowing across the full repayment period before signing anything.

4. Applying Without a Business Plan

Many lenders (especially for SBA loans and traditional bank financing) require a formal business plan. Even when it's not mandatory, having one strengthens your application by showing the lender you've thought through revenue projections, use of funds, and market conditions.

This matters even more for startups and new businesses, which face extra scrutiny from underwriters. The good news is that lending for newer firms is growing: the SBA supported 103,000 financings in 2024 (the highest since 2008), with loans under $150,000 doubling since FY20. Opportunity exists for new business owners who prepare properly. A solid business plan is the most controllable way to improve your odds.

5. Not Comparing Multiple Lenders

Rates, terms, and fees vary dramatically across lender types, and accepting the first offer you receive can cost thousands over the life of the loan. The 2025 Federal Reserve Small Business Credit Survey found that small banks had the highest full approval rate at 54%, while net satisfaction with online lenders dropped from 15% to just 2%.

Get quotes from at least three sources before committing. Some of the differences between lender types are:

Traditional banks tend to offer lower interest rates but slower processing and stricter requirements.

Credit unions often provide relationship-based flexibility and competitive rates for members.

Online lenders and alternative financial institutions prioritize speed and accessibility, but charge more for it.

Each type of lender has trade-offs. Comparing them side by side is the only way to find the best fit.

6. Ignoring Personal Guarantees and Collateral Requirements

Many borrowers don't fully understand what they're agreeing to when they sign a personal guarantee. It means your personal assets (home, savings, vehicles) are on the line if the business defaults on the loan. SBA loans require personal guarantees from all owners with 20% or more ownership, and most traditional bank loans do the same.

Collateral requirements add another layer. Some lenders file Uniform Commercial Code (UCC) liens against business assets, which can restrict your ability to borrow elsewhere until the debt is repaid. If you're already carrying high-cost business debt, refinancing into a lower-rate product before taking on additional financing can reduce your overall exposure and improve your personal finance position.

7. Submitting an Incomplete Application

Incomplete applications are one of the most common reasons for delays and outright denials. The underwriting process requires specific documentation, and missing items signal disorganization to lenders. The most commonly requested documents include:

Personal and business tax returns. Lenders may ask for two to three years' worth. At Clarify Capital, we usually just ask for bank statements.

Financial statements. They might also want profit and loss statements plus a current balance sheet. You typically don't need these when you get a loan through Clarify Capital.

Bank statements. We ask for three months of business banking records, but some lenders want up to six.

Business licenses and legal documents. You may need formation documents, operating agreements, and any relevant permits, depending on the lender.

Proof of collateral. Some loans require documentation of assets being pledged.

Before starting the application process, review your current obligations and gather every document your lender might request.

8. Waiting Until You're Desperate To Apply

Applying under financial pressure leads to worse outcomes across the board. Borrowers in a cash crunch tend to accept unfavorable terms, skip due diligence, or turn to high-cost products like merchant cash advances because they need funding immediately. That urgency is expensive.

The best time to build a relationship with a business banking partner is before you need capital. According to the same Federal Reserve survey, 57% of small firms that didn't apply for financing said they already had sufficient funds. Being in that position (applying from strength rather than desperation) gives you leverage to negotiate better rates and terms.

Types of Business Loans and How They Work

Business loans come in several forms, each built for different business purposes and financial situations. Some provide a one-time lump sum for a specific purchase, while others give you ongoing access to capital as you need it. Here's how the most common financial products work.

| Business Loan Types at a Glance | |||||

|---|---|---|---|---|---|

| Loan type | Get funded in | Borrow up to | Interest / factor rate | Term length | Payment frequency |

| Term loan | 24 to 72 hours | $5M | 6% to 12% APR | Three to 10 years (long-term); six to 24 months (short-term) | Monthly (long-term); weekly or monthly (short-term) |

| Business line of credit | 24 to 48 hours | $5M | 6% to 14% APR | Revolving credit with terms from six to 36 months | Weekly or monthly |

| SBA loan | Two to 12 weeks | 7a: $5M 504: $5.5M | 7a: base rate + 3.0% to 6.5% (7(a)) 504: fixed rate tied to U.S. Treasury bond rates | Up to 25 years (real estate); 10 years (other) | Monthly |

| Invoice factoring | 24 hours | 70% to 100% of invoice amount | 0.5% to 3% per 30 days | 30 to 120 days | N/A |

| Merchant cash advance | 24 hours | $5M | 1.08 to 1.45 factor rate | Six to 24 months (approximate) | Daily, weekly, monthly, or % of sales |

| Equipment financing | One to two days | 100% value of equipment | 4% to 45% APR | 24 to 72 months | Monthly |

Business Term Loans

A business term loan is the most straightforward type of business financing. The borrower receives a lump sum up front and repays it (plus interest) in fixed loan payments over a set repayment period. Most term loans use a monthly payment schedule, though some short-term lenders collect weekly.

Terms typically range from six months to 10 years, depending on the lender and loan amount. Long-term loans (three to 10 years) usually carry lower monthly payments but cost more in total interest over the life of the repayment schedule. Short-term loans (six to 24 months) have higher payments but lower total cost. At Clarify Capital, term loan APRs start at 6% with funding in as fast as 24 hours.

Business Lines of Credit

A business line of credit works more like a business credit card than a traditional loan. Instead of receiving a lump sum, you get access to a revolving credit limit you can draw from as needed. You only pay interest on the amount you've actually borrowed, not the full limit.

This makes lines of credit a strong fit for managing working capital gaps, covering seasonal cash flow dips, or handling unexpected expenses without locking into a fixed repayment term. At Clarify Capital, business lines of credit go up to $5 million with APRs from 6% to 14% and revolving terms of six to 36 months. A business credit card is a similar product but typically comes with smaller credit limits and is better suited for everyday operational expenses.

SBA Loans

SBA loans are backed by the U.S. Small Business Administration, which doesn't lend directly. Instead, the Small Business Administration guarantees a portion of the loan through approved lenders, which reduces risk for the lender and enables lower interest rates for the borrower. The trade-off is stricter eligibility requirements and longer processing times.

Three main programs fall under the SBA umbrella:

7(a) loans. The most common SBA program, offering up to $5 million with terms up to 25 years for real estate and 10 years for other purposes. Interest rate caps are tied to a base rate plus a spread that varies by loan size.

504 loans. Designed for major fixed assets like commercial real estate, 504 loans go up to $5.5 million with rates pegged to the 10-year Treasury rate and terms of 10, 20, or 25 years. The standard down payment is 10%, rising to 15% or 20% for new businesses or special-purpose properties.

Microloans. Built for smaller capital needs, SBA microloans max out at $50,000 (the average is around $13,000) with terms up to seven years and rates generally between 8% and 13%. They can't be used for real estate loans or to pay off existing debt.

Equipment Loans

Equipment loans are used to purchase specific business assets (machinery, vehicles, technology, restaurant equipment), and the equipment itself typically serves as collateral. That built-in security makes equipment financing easier to qualify for than unsecured loans, where no collateral backs the debt.

At Clarify Capital, equipment financing covers up to 100% of the equipment's value with APRs from 4% to 45% and repayment terms of 24 to 72 months. Payments are monthly, and funding can happen in one to two days.

Merchant Cash Advances and Invoice Factoring

A merchant cash advance isn't technically a loan. A provider advances a lump sum in exchange for a percentage of your future sales, repaid through automatic daily, weekly, or monthly deductions. MCAs use factor rates (typically 1.08 to 1.45) rather than traditional APR, and the effective cost is often significantly higher interest rates than what you'd pay on a term loan. They're short-term financing tools best used when speed matters more than cost.

Invoice factoring works differently: you sell outstanding accounts receivable to a factoring company at a discount (typically 0.5% to 3% per 30 days) in exchange for immediate cash. The factoring company collects payment directly from your customers. Both MCAs and factoring can help businesses with thin credit histories or urgent cash needs, but the cost of borrowing is real. Treat them as short-term solutions, not long-term business debt strategies.

How To Qualify for a Business Loan

Qualification standards vary by lender and loan type, but most lenders evaluate the same core factors. Here's what you'll typically need:

Credit score. Traditional banks generally look for 680+; SBA lenders want 650 to 690; online lenders (including Clarify Capital) may accept 500+. Both personal credit and business credit factor into the decision.

Time in business. Banks generally require at least two years of operating history. Clarify Capital accepts as few as six months.

Annual revenue. Minimum thresholds vary by loan amount and lender: Most traditional lenders want to see at least $100,000 to $250,000 in annual revenue for term loans, and Clarify Capital requires $10,000 in monthly revenue.

Existing debt. In 2024, 39% of small firms carried more than $100,000 in outstanding debt. High existing obligations are the number one reason for denial, so reducing your current business debt before applying improves your odds.

Down payment. SBA 504 loans require a 10% standard down payment, 15% if the business is under two years old or the property is special-purpose, and 20% if both. Most other loan types don't require a down payment.

Documentation. Have your tax returns, financial statements, bank statements, and legal documents ready before you apply. Reference the list in Mistake 7 above.

Smart Borrowing Starts With the Right Preparation

Understanding how business loans work gives you a real advantage in the application process. The small business owners who get funded on the best terms aren't necessarily the ones with the highest revenue or the longest track record. They're the ones who took the time to understand their options, prepare their documentation, and avoid the mistakes that trip up most applicants.

If you're ready to explore your business financing options, Clarify Capital has helped more than 50,000 businesses access nearly $1 billion in funding. With APRs starting at 6%, loans up to $5 million, and funding in as fast as 24 hours, we can help you find the right loan for your business.

Frequently Asked Questions

How much is a $50,000 business loan monthly?

It depends on the interest rate and repayment term. At 10% APR over five years, a $50,000 loan costs roughly $1,062 per month. Stretch the repayment schedule to 10 years, and the monthly payment drops to about $661, but you'll pay significantly more in total interest. Shorter terms mean higher loan payments but lower overall cost. Use a business loan calculator to estimate monthly payments based on your specific rate and term:

What are the disadvantages of a business loan?

The main disadvantages include interest costs over the life of the loan, the risk of signing a personal guarantee (which puts personal assets on the line), collateral requirements that can restrict future borrowing, and the impact of loan payments on your monthly cash flow. The application process itself can also be time-consuming, particularly for SBA loans and traditional bank products that require extensive documentation. High-cost options like merchant cash advances carry additional risk of accumulating business debt quickly.

What credit score is needed for a $40,000 loan?

A $40,000 loan falls within most lenders' standard ranges. Traditional banks typically want 680+, SBA lenders generally require 650+, and online lenders may approve borrowers with credit scores as low as 500 to 600. Your creditworthiness affects not just whether you're approved but also what rates and terms you're offered. Higher scores generally unlock lower interest rates and better repayment terms.

How are business loans paid off?

Loan repayment structures vary by product type. Term loans are most commonly repaid through fixed monthly payments over the full repayment period, though some online lenders use weekly or daily schedules. Business lines of credit work on a revolving basis: you draw funds, repay them, and can borrow again up to your credit limit. Merchant cash advances are repaid through automatic deductions (daily, weekly, or as a percentage of sales) until the balance is settled. Some loans carry prepayment penalties for paying off early, while others allow it without extra cost. Always check the repayment terms before signing.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts