The U.S. fitness club market hit $121.19 billion in 2024, and gym memberships reached a record 77 million Americans. But opening or growing a fitness business takes serious capital. Equipment alone can run $25,000 to over $288,000, depending on your facility size, and that's before factoring in build-out costs, franchise fees, or working capital. Gym equipment financing helps you spread costs and keep cash available for operations.

I've helped small businesses access almost $1 billion in funding to reach their business goals. If you're interested in growing a new or existing fitness center, here's everything you need to know about your financing options.

| Gym and fitness center financing options | Funding speed | Borrow up to | Rate/cost | Best for | |

|---|---|---|---|---|---|

| Equipment financing | 1 to 2 days | 100% of equipment value | 4% to 45% APR | Treadmills, weight machines, cardio equipment | Jump to details |

| Term loans | 24 to 72 hours | $5M | 6% to 12% APR | Facility build-outs, expansion, large investments | Jump to details |

| Business lines of credit | 24 to 48 hours | $5M | 6% to 14% APR | Working capital, seasonal gaps, ongoing costs | Jump to details |

| SBA 7(a) loans | Several weeks | Varies by program | 9.5% to 15.25% | Lower rates with more documentation and time | Jump to details |

| Equipment leasing | Varies | Value of equipment | 5% to 20% | Preserving cash, upgrading equipment regularly | Jump to details |

| Merchant cash advances | 24 hours | $5M | 1.08 to 1.45 factor rate | Fast cash for time-sensitive needs | Jump to details |

Apply for a Gym or Fitness Center Loan

Equipment Financing

Equipment financing is specifically for purchasing gym assets: commercial treadmills ($4,500 to $8,000 each), weight machines ($2,500 to $5,000), ellipticals ($3,500 to $5,500), and stationary bikes ($2,500 to $4,000). The equipment itself serves as collateral, which often means more flexible eligibility requirements than unsecured loans. You can borrow up to 100% of the equipment's value starting at 6% APR, with 24 to 72-month terms and monthly payments.

This is usually the first financing option gym owners explore because the structure is straightforward: you pick the equipment, the lender funds it, and you repay over time while using the machines to generate revenue from day one.

Term Loans

A term loan gives you a lump sum up front that you repay on a fixed schedule. Short-term options run six to 24 months with weekly or monthly payments; long-term options stretch three to 10 years with monthly payments. APRs range from 6% to 12%.

For gym owners, term loans make the most sense for larger planned investments that go beyond equipment: facility build-outs, renovations, opening a second location, or a full rebrand. The predictable repayment structure makes it easier to budget against your membership revenue.

Business Lines of Credit

A business line of credit gives you revolving access to funds. Draw what you need, pay interest only on what you use, and the credit replenishes as you repay. Funding in 24 to 48 hours, up to $5M, starting at 5% APR.

This is one of the most practical financing solutions for fitness centers because it covers the unpredictable costs that come with running a gym: a broken AC unit in July, a marketing push before New Year's resolution season, or covering payroll during a slow summer when memberships dip. It's essentially working capital on demand. You don't need to reapply each time.

SBA 7(a) Loans

SBA loans are backed by the Small Business Administration, which means lower interest rates and longer repayment terms. The trade-off is more documentation and a longer approval timeline (typically several weeks). APR starts at 6.75%.

Fitness businesses are one of the more common SBA loan categories. If your gym has strong financials and you're planning a major expansion or franchise purchase, the lower rates save you a significant amount over the life of the loan.

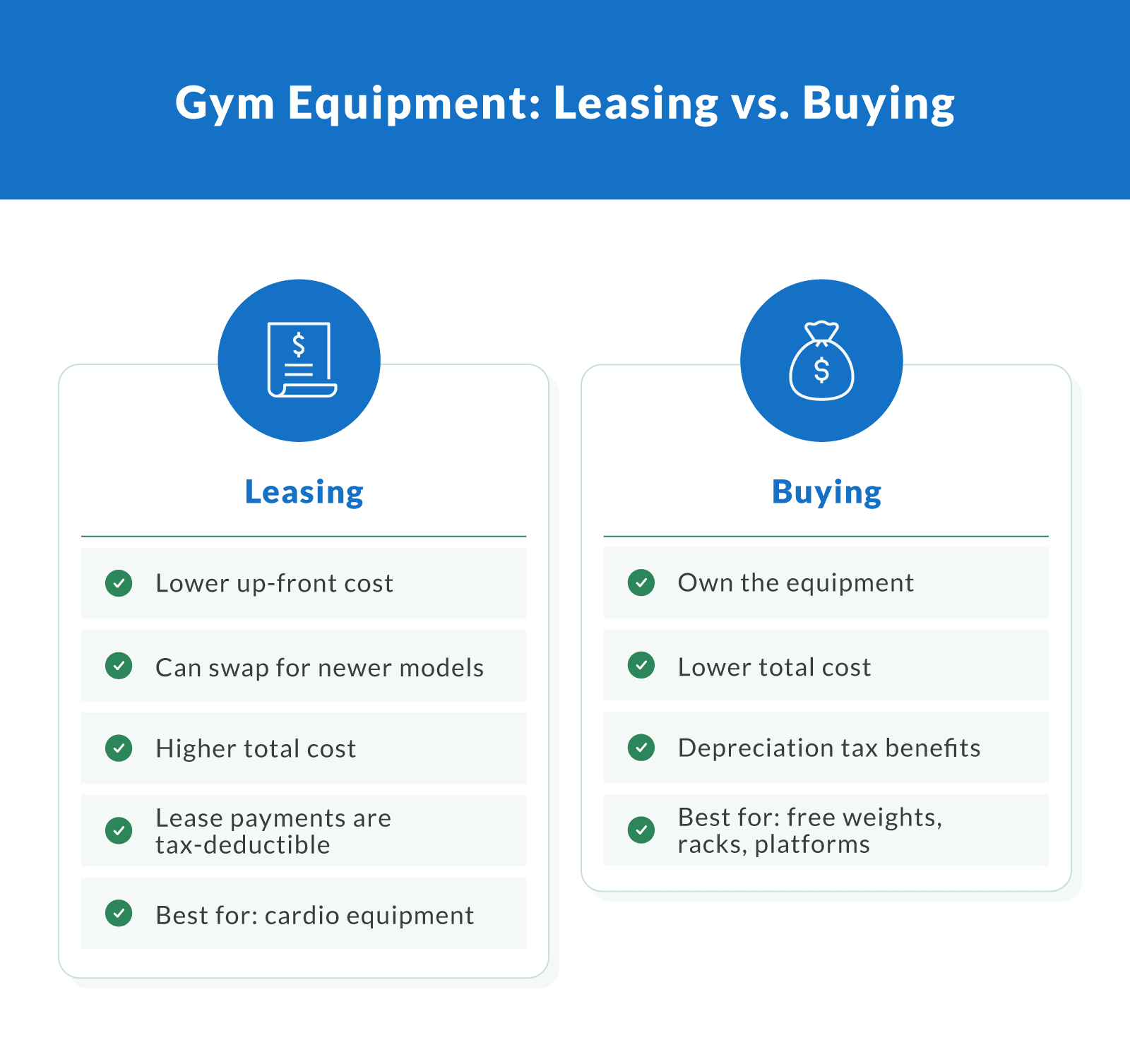

Equipment Leasing

Leasing is different from equipment financing because you're renting the equipment instead of buying it (which is what equipment loans are used for). Monthly lease costs run $150 to $250 for a treadmill, $120 to $200 for an elliptical, $85 to $140 for a stationary bike, and $80 to $160 for a weight machine. Standard terms are 12 to 60 months, with rates typically between 5% and 20%.

Leasing works well for cardio equipment that you'll want to replace every three to five years anyway. You won't own the machines at the end of the term, and the total cost over the lease is higher than buying outright, but it preserves your cash and keeps your gym floor stocked with the latest models without a large down payment.

Merchant Cash Advances

A merchant cash advance gives you an advance on future revenue, repaid as a percentage of your daily or weekly sales. Factor rates range from 1.08 to 1.45, with funding as fast as same-day.

I've seen gym owners use MCAs when a piece of critical equipment breaks down, and they need a replacement immediately, or when a build-out deadline is approaching and the contractor needs payment. The cost is higher than other financing options, so make sure you understand the total repayment amount before signing. It's a tool for specific situations, not a default choice.

Leasing vs. Buying Gym Equipment

One of the biggest financing decisions gym owners face is whether to lease equipment or buy it outright through financing. Here's how the two compare.

| Leasing | Buying (financing) | |

|---|---|---|

| Up-front cost | Low or no down payment | May require 10% to 20% down |

| Monthly cost | $30 to $250 per piece, depending on equipment | Varies by loan terms and APR |

| Ownership | You don't own the equipment | You own it after it's paid off |

| Upgrades | Swap for newer models at lease end | You sell or trade in |

| Total cost | Higher over the full term | Lower total cost of ownership |

| Tax treatment | Lease payments deductible as operating expenses | Equipment depreciates over five to seven years under MACRS |

| Best for | Cardio equipment you'll replace every three to five years | Strength equipment with long useful life (free weights, racks) |

By far, most U.S. companies use leasing to acquire equipment, but that doesn't mean it's always the right call. Free weights and power racks last 10+ years with minimal maintenance, so financing the purchase makes more financial sense for those.

Most gym owners I work with use a mix: They lease cardio equipment (which needs frequent updating) and buy strength equipment outright.

The equipment financing versus leasing decision ultimately comes down to how long you plan to keep each piece.

Watch for hidden fees in lease agreements, including prepayment penalties, end-of-lease buyout costs, and maintenance clauses. Read the full contract before you sign.

What It Costs To Open or Expand a Gym

Costs vary dramatically by facility type. Here's what to expect based on the size and model of your fitness business.

| Gym type | Total startup cost | Equipment budget | Space |

|---|---|---|---|

| Personal training studio | $30,000 to $150,000 | $25,000 to $60,000 | 800 to 900 sq ft |

| Boutique studio (yoga, cycling, CrossFit) | $75,000 to $300,000 | $60,000 to $140,000 | 800 to 1,400 sq ft |

| Mid-size gym | $150,000 to $300,000 | $60,000 to $140,000 | 1,200 to 3,000 sq ft |

| Full-service gym | $500,000+ | $112,000 to $288,000+ | 3,000 to 10,000+ sq ft |

| Franchise (e.g., Planet Fitness) | $1.5M to $5.2M | $36,300 to $1.1M | Varies by brand |

Equipment and build-out account for 40% to 60% of total startup capital. Buying used or remanufactured equipment (30% to 50% less than new) is one way to stretch your budget, but financing lets you buy new without draining your cash reserves. Either way, most gym owners need at least one type of financing to cover the gap between what they have saved and what the facility actually costs.

Financing for Different Types of Fitness Businesses

Different financing products work best for different types of fitness businesses, and here's why.

Franchise Gyms

Franchise operators face significant up-front costs, like:

Franchise fees

Build-out requirements

Brand-mandated equipment

Territory agreements

Planet Fitness requires a minimum net worth of $3.3 million and at least $1.5 million in liquid assets. Anytime Fitness starts at $381,575 to $783,897 in total investment with a $42,500 franchise fee.

SBA 7(a) loans and term loans are the most common choices for franchise financing because the loan amounts are large enough to cover these costs. Most lenders (including Clarify Capital) require at least six months in business, so plan your financing timeline before signing a franchise agreement.

Boutique Studios (Yoga, CrossFit, Cycling)

These have lower startup costs but specialized equipment needs. CrossFit boxes require rigs, bumper plates, barbells, kettlebells, and rowing machines. The annual affiliation fee is $3,000, with Level 1 certification costing about $1,000. Cycling studios invest heavily in bikes ($2,500 to $4,000 each). Yoga studios have lower equipment costs but higher build-out expenses (sprung flooring, mirrors, sound systems).

Equipment financing and lines of credit are the most common choices here. The boutique fitness market is valued at $37.15 billion and growing at 8% annually, so lenders are familiar with the model and comfortable funding these businesses.

Personal Training Studios

The smallest footprint and lowest startup costs of any gym model. A home gym or small studio can get started with $30,000 to $150,000 total. Equipment needs are focused: adjustable dumbbells, a rack, a bench, cardio equipment like a treadmill or rower, and functional training tools.

Equipment financing or a business line of credit can cover the initial outfitting. For smaller equipment purchases (under $5,000), I've seen some retailers offer checkout financing through providers like Affirm or PayPal with interest-free promotional periods. But for a full studio build-out, a business loan gives you more flexibility, better terms, and a single payment plan instead of having you juggle multiple credit accounts.

Minimum Qualifications

$10,000 in monthly revenue

Your business must earn at least $10K per month in a business bank account.

500+ credit score

You can get approved with any credit score. But the better your credit rating, the better interest rates lenders offer. Your FICO score should be above 500.

Minimum six months in business

Your company should be operational for a minimum of six months. This shows business lenders that your company is sustainable and won't go out of business.

Have a business bank account

Your Clarify advisor will need three or four months of your most recent bank statements to verify income. This is just to see you're actually making $10K+ month in revenue.

How To Apply for a Gym Business Loan

The process is simpler than most gym owners expect.

Gather your documents. You'll need three months of recent bank statements, tax returns, and proof of a business bank account. SBA loans also require a business plan.

Review your financials. Check your credit score, annual revenue, and existing debt. Most online lenders accept scores of 600 or higher; SBA and traditional banks typically want 680+. Clarify Capital offers same-day funding for credit scores over 550.

Match the loan type to your needs. Equipment purchase? Use equipment financing. Facility renovation? A term loan. Cash flow buffer? A line of credit. Matching the product to the purpose gets you better terms.

Submit your application. Clarify Capital's online application takes about two minutes.

Review your offer. Look at the total cost, not just the monthly payment. Compare the APR, repayment terms, and any origination fees before accepting.

Tips for Stronger Gym Loan Applications

A few moves before you apply can improve your approval odds and the terms you're offered.

Keep your credit clean

Check both personal and business credit reports for errors. Even small inaccuracies can pull your score down and limit your options.

Organize your financial records

Lenders want consistent, well-tracked revenue and expenses. Clean books signal a well-run business and speed up underwriting.

Reduce existing debt

Pay down credit card balances and outstanding loans before applying. A lower debt-to-income ratio opens the door to better rates.

Show membership growth trends

Give lenders month-over-month and year-over-year membership data. Proving that your gym is growing (or stable) builds confidence in your ability to repay.

Separate personal and business finances

If you're still running gym expenses through a personal bank account, open a dedicated business account before applying. Lenders check for this.

Detail your equipment and build-out plan

"I need $120,000 for 15 cardio machines, four squat racks, and a turf area for functional training" is stronger than "I need money for equipment." Specifics show you've done the math.

Build the Gym Your Members Deserve

Gym memberships hit record highs in 2024, and 86.8% of gym owners expect those numbers to keep climbing. The fitness business owners who invest in the right equipment and facilities now are the ones positioned to capture that growth. Whether you're replacing a worn-out cardio floor, opening your first boutique studio, or scaling a franchise, the right financing turns your plan into reality without draining your cash reserves. Apply through Clarify Capital and get matched with an advisor who understands what fitness businesses need to grow.

Frequently Asked Questions

These are the top questions businesses ask me about funding gyms and fitness centers.

Can You Finance Gym Equipment?

Yes. Equipment financing lets you purchase commercial gym equipment (treadmills, weight machines, bikes, free weights) and repay the cost over 24 to 72 months. The equipment serves as collateral, so qualification tends to be more flexible than unsecured loans.

What Credit Score Is Needed for an Equipment Loan?

Many online lenders accept credit scores of 600 or higher. SBA loans and traditional banks typically require 680+. Clarify Capital offers same-day funding for scores over 550.

Is It Better To Lease or Buy Gym Equipment?

It depends on the equipment type. Leasing preserves cash and makes upgrades easy, but costs more over the full lease term. Buying through financing means a lower total cost and ownership at payoff. Most gym owners lease cardio equipment (which needs frequent replacement) and buy strength equipment like racks, barbells, and dumbbells.

How Much Does It Cost To Open a Gym?

Costs range from $30,000 for a small personal training studio to over $5 million for a franchise like Planet Fitness. A mid-size independent gym typically requires $150,000 to $300,000, with equipment and build-out accounting for 40% to 60% of that total.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts