Equipment financing is often one of the first things a new business will look into. With this type of business funding, a lender covers the cost of a piece of equipment. You then repay over a set term, with the equipment itself serving as collateral.

But it's not your only option. General business loans, SBA programs, and leasing all offer different trade-offs on rates, flexibility, and ownership. The wrong choice can mean overpaying by thousands or locking into terms that don't match your cash flow.

I've worked with hundreds of small business owners navigating equipment purchases, and the right financing structure depends on your credit, how long you'll use the equipment, and how fast you need funds. This guide breaks down the key differences, current rates, Section 179 tax benefits, and how to qualify for the best terms on new business equipment.

New Business? What To Know Before You Apply

Most equipment financing lenders will want to see at least six months in business and a credit score of 550 or higher, so brand-new startups may not qualify right away. If you need equipment to start generating revenue, you still have options:

Equipment leasing

Lower up-front costs than buying, and some lessors work with newer businesses. You're paying for use, not ownership, so monthly payments are typically lower.

Vendor financing

Many equipment vendors offer in-house financing or work with lenders that specialize in startups. It's worth asking your vendor directly before looking elsewhere.

SBA Microloans

Available through nonprofit intermediaries, SBA Microloans go up to $50,000 with more flexible requirements than traditional SBA programs.

Personal loan or line of credit

No business history required. Rates can be high, but it's a viable bridge for early-stage equipment needs.

CDFI loans

Community Development Financial Institutions serve underbanked and startup businesses, often with more flexible underwriting than traditional banks.

Business credit cards

Best for smaller purchases. Some cards offer 0% intro APR periods that can ease up-front costs.

Once you have at least six months of operating history and consistent monthly revenue, you'll qualify for a much wider range of lenders and better rates.

Ready to see what you qualify for? Apply through Clarify Capital today.

Key Differences Between Equipment Financing and Business Loans

Equipment financing and general business loans both put capital in your hands, but they work differently. Here's how they compare:

Collateral. Equipment financing uses the equipment itself as collateral, so you don't need to pledge other business assets. Business loans may require additional collateral or a personal guarantee.

Use of funds. Equipment financing is restricted to purchasing specific business equipment. A small business loan can fund any expense, from working capital to hiring to inventory.

Loan amounts. Equipment financing amounts are typically tied to the value of the equipment (up to 100% of the purchase price). General business loan amounts have broader ranges and aren't tied to a single asset.

Approval speed. Equipment financing approvals can take as little as one to two business days with alternative lenders. Traditional bank loans often take weeks.

Down payment. Equipment loans often require 0% to 20% down. Business loan down payments vary widely by lender and loan type.

Ownership. You own the equipment outright once you pay off an equipment loan. With some business loans, you're borrowing against assets you may already own.

If you know exactly what you need and want structured repayment terms tied to that asset, equipment financing is the more straightforward path. If you need flexibility to use funds across multiple business needs, a general loan gives you that freedom.

Equipment Financing Options for New Businesses

Not every financing option works the same way, and what's best depends on your credit profile, how long you'll use the equipment, and whether you want to own it outright. Here are the most common funding options.

Equipment Loans

An equipment loan is a fixed-term loan where a lender funds the purchase and you make monthly payments over a set period. The equipment serves as collateral, and you own it once the loan is paid off.

Most lenders offer equipment loans covering up to 100% of the equipment's value with terms ranging from two to seven years. Both new and used equipment qualify with most providers, so you're not limited to buying brand new.

Equipment loans work best for a piece of equipment with a long useful life: manufacturing machinery, commercial vehicles, restaurant ovens. The loan amount ties directly to the equipment's value, and repayment terms are structured around its expected lifespan.

Equipment Leasing

Equipment leasing lets you pay to use equipment for a set lease term without owning it. At the end of the lease, you can return the equipment, buy it at fair market value, or renew.

Leasing suits businesses that need to upgrade frequently or want lower up-front costs. Monthly payments are typically lower than loan payments because you're paying for use, not ownership. The trade-off is that you don't build equity, and the total cost can exceed what you'd pay with a loan if you end up buying the equipment at the end.

Leasing equipment is common for types of equipment that lose value quickly or become obsolete (technology, medical and healthcare equipment, construction equipment). If you'll use something for three to five years and then need the latest model, leasing keeps your options open.

| Equipment Loan To Purchase vs. Lease | ||

|---|---|---|

| Factor | Equipment loan to purchase | Equipment lease |

| Ownership | You own equipment after payoff | Lender/lessor owns; buyout option possible |

| Up-front costs | 0% to 20% down payment | First and last month's payment typical |

| Monthly payments | Higher (you're building equity) | Lower (you're paying for use only) |

| Total cost over term | Lower if you keep the equipment long-term | Higher if you exercise a buyout |

| Tax benefits | Section 179 deduction, depreciation, interest is tax deductible | Lease payments may be fully deductible as a business expense |

| Flexibility | You're locked into the equipment | You can upgrade at lease end |

| Best for | Equipment you'll use for years | Technology or equipment that needs frequent upgrading |

The total cost gap between equipment financing for buying and leasing depends on the equipment's useful life, the interest rate, and whether you plan to buy the equipment at the end of a lease.

SBA Loans

SBA loans through the 504 and 7(a) programs can fund equipment purchases at some of the lowest rates available. SBA 504 loans offer long-term, fixed-rate financing up to $5.5 million for major fixed assets, including equipment. Current 504 rates are approximately 5% to 7% with 10-, 20-, or 25-year fixed terms.

The Small Business Administration's 7(a) program offers more flexibility on how you use the funds but typically comes with variable interest rates. Both programs require more documentation and longer approval timelines than conventional equipment loans.

The trade-off between SBA loans and conventional financing is time versus savings. You'll wait longer and submit more paperwork, but the rates and terms from SBA programs are hard to beat if you qualify.

Business Lines of Credit

A business line of credit gives you revolving access to funds you can draw from as needed. It's more flexible than an equipment loan because you're not restricted to a single purchase, and you only pay interest on what you borrow.

That flexibility comes at a cost. Interest rates on lines of credit are typically higher than equipment-specific financing, and credit approval requirements can be stricter since there's no equipment serving as collateral.

A line of credit makes the most sense as a supplement: covering smaller equipment purchases, bridging cash flow gaps while you wait for other financing to close, or handling unexpected up-front costs like installation and delivery. It's not the most efficient tool for a large equipment purchase, but it offers flexible payment options as part of a broader business financing strategy.

Compare Your Equipment Financing Options

Whether you need a dedicated equipment loan or a flexible business loan, we'll help you find the right fit for your purchase.

Equipment Value

Up to 100%

Funding Speed

1–2 Days

Starting Rates

4%+ APR

Equipment Financing Rates, Terms, and Costs

Business loan interest rates depend heavily on your credit score, time in business, and the type of lender you work with. Here's what the current landscape looks like.

Equipment financing APRs generally range from 4% to 45%, depending on the lender and borrower profile. That's a wide spread, so here's how it breaks down by credit tier:

Excellent credit (700+ FICO). 4% to 11% APR

Fair credit (600 to 699 FICO). 15% to 45%+ APR

SBA 504 loans. ~5% to 7% fixed

Typical loan terms. Two to seven years (24 to 72 months)

Down payments. 0% to 20%

Origination fees. Vary by lender, typically 1% to 3%

For context, average small-business bank loan interest rates ranged from 5.35% to 11% in Q3 2025, according to Federal Reserve data. Fixed rates are common with equipment financing, which protects you from rate fluctuations over the life of the loan.

The total cost of borrowing also depends on whether you're financing or leasing. Here's how the two compare:

Before signing any financing agreement, review the lender's full disclosures, including prepayment penalties, late payment fees, and how they calculate the total cost of borrowing.

Section 179 Tax Deduction for Equipment Purchases

The Section 179 deduction lets you write off the full purchase price of qualifying business equipment in the year it's placed in service, rather than depreciating it over several years. For businesses financing new equipment, this can significantly reduce your effective cost.

The One Big Beautiful Bill Act (signed July 2025) raised the Section 179 deduction limit to $2,500,000 for 2025, more than doubling the previous cap. The phase-out threshold starts at $4,000,000 in total qualifying property. For 2026, the inflation-adjusted limit is $2,560,000 with a phase-out at $4,090,000.

The OBBBA also permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. Before this legislation, bonus depreciation had been phasing down annually under the original Tax Cuts and Jobs Act schedule.

So, if you finance a $200,000 piece of construction equipment and place it in service this year, you can deduct the full $200,000 from your taxable income. You don't need to pay cash up front to claim the deduction, either. Financed equipment qualifies, as long as it's used more than 50% for business purposes. Both new and used business equipment are eligible for Section 179, provided the asset is new to your business.

How To Qualify for Equipment Financing

Eligibility requirements vary by lender, but most equipment financing providers evaluate the same core factors:

Credit score. Most lenders require a minimum personal credit score of 600 to 650, though borrowers above 700 get the best rates. Clarify Capital accepts scores as low as 550.

Time in business. With Clarify Capital, you'll need at least six months of operating history. Startup and newer businesses can still qualify through some online lenders, but you'll likely need stronger personal credit and a higher down payment.

Annual revenue. Requirements vary, but most lenders look for a minimum of $50,000 to $100,000 in annual revenue. Clarify Capital looks for $10,000 in monthly revenue.

Down payment. This ranges from 0% to 20%, depending on your creditworthiness and the loan amount. Putting more money down can help offset a lower credit score.

Personal guarantee. Many lenders require a personal guarantee, especially for newer businesses. Building strong business credit over time reduces the likelihood.

Equipment details. Lenders evaluate the type, condition, and useful life of the equipment being financed. Equipment with a longer useful life and strong resale value is easier to finance.

Even if your business is relatively new, equipment financing is more accessible than options with stricter small business loan requirements because the equipment itself serves as collateral. The lender's risk is lower, so underwriting standards are more flexible than you might expect.

Banks vs. Alternative Lenders for Equipment Financing

Where you get your financing matters just as much as what type you choose. Traditional banks and alternative lenders offer very different experiences.

Banks typically offer lower interest rates, but the process is slower, and requirements are stricter. Most require at least two years in business, $250,000+ in annual revenue, and strong personal credit. Funding timelines at traditional banks can stretch to 10 business days or longer, and the paperwork is substantial.

Alternative lenders and equipment financing companies trade slightly higher rates for speed and accessibility. Many offer credit approval within one to two business days, and some fund same-day. The application process is simpler, the requirements are lower, and you don't need years of history to get approved.

For Franklin Zambrano, owner of Zambrano's Complete Auto Center in Trenton, NJ, speed was the deciding factor. When an opportunity came up to buy a second alignment machine for his family-owned auto repair shop, he needed capital fast:

The opportunity came up to be able to buy a second alignment machine, so we needed the funds quick. I couldn't let that opportunity pass. If you go through a normal bank, it's a pain. That requires so much information, so much paperwork. And I tell people, 'Look, you try to get a loan from the bank it's like pulling teeth.' But if you have a situation where you need money fast, and you need somebody to give you an answer right away, Clarify is a good option."

Clarify funded Zambrano's equipment purchase within 48 hours, with flexible short-term repayment under 18 months. That kind of turnaround is common with alternative lenders offering fast business funding, and it's a major reason business owners choose them for time-sensitive equipment purchases.

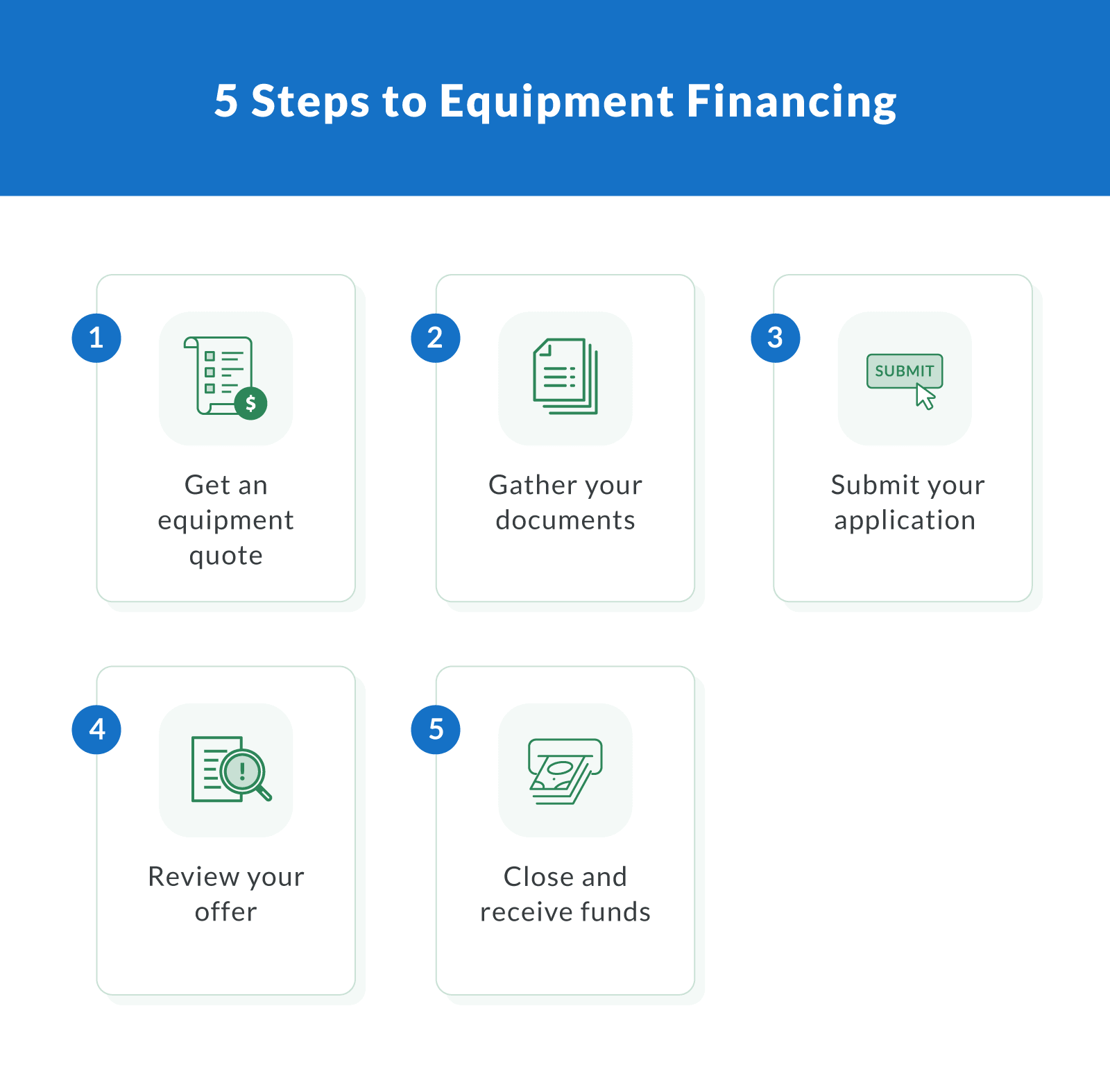

Application Steps for Equipment Financing

The application process is typically straightforward, especially with Clarify Capital. Here's what to expect:

Get an equipment quote. Know what you're buying and how much it costs. Lenders need a quote or invoice from the vendor.

Gather your documents. Most lenders ask for recent bank statements, business tax returns, a government-issued ID, and basic business details (EIN, time in business, annual revenue).

Submit your application. Many of the best equipment financing companies offer online applications that take 10 to 15 minutes.

Review your offer. Compare the APR, loan amount, repayment terms, and any fees. Pay attention to whether the rate is fixed or variable.

Close and receive funds. Once you accept, funding can arrive in as few as one to two business days.

The biggest difference between lenders is documentation. Banks want detailed financials, business plans, and sometimes collateral beyond the equipment. Alternative lenders often make decisions based on recent bank statements and your credit profile.

Clarify Capital's equipment financing offers approval in as little as 24 hours with terms up to 72 months.

Get the Equipment Your Business Needs

The right financing solution comes down to three things: your credit profile, how long you'll use the equipment, and your cash flow. A strong credit score opens the door to lower rates and better terms. If speed matters more than the absolute lowest rate, alternative lenders can get you funded in days instead of weeks.

Don't overlook the Section 179 deduction, either. With the 2026 limits now above $2.5 million, the tax savings alone can offset a significant chunk of your financing costs.

Whether you're buying your first commercial vehicle or upgrading machinery you've relied on for years, the best next step is comparing your options. Apply with Clarify Capital to see what you qualify for.

Frequently Asked Questions

I'll answer some of the most common questions I get about equipment financing for new and growing businesses.

Is It Better To Lease or Finance Equipment?

It depends on how long you'll use the equipment. Financing (buying) is better for equipment with a long useful life that won't become obsolete, since you'll build equity and pay less over time. Leasing keeps up-front costs lower and suits technology or equipment that needs frequent upgrading. If you'll use the same piece of equipment for five or more years, financing almost always costs less overall.

What Credit Score Do You Need for Equipment Financing?

Most lenders require a minimum personal credit score of 600 to 650. Borrowers above 700 typically qualify for the lowest rates (4% to 11% APR), while some alternative lenders accept scores as low as 550 with higher rates and down payments.

How Long Does Equipment Financing Take?

Timelines vary by lender. Traditional banks may take one to three weeks from application to funding. The best equipment financing companies can approve and fund within one to two business days, with some offering same-day funding.

Can a New Business Get Equipment Financing?

Yes, though your options may be more limited. Newer businesses (under two years) can qualify with many alternative lenders, especially with a personal credit score above 600 and consistent revenue. Expect a higher down payment and higher interest rates than an established business would receive.

What Is the Monthly Payment on a $50,000 Equipment Loan?

Monthly payments depend on the interest rate and term length. At 10% APR over a five-year term, a $50,000 equipment loan costs roughly $1,062 per month. At 6% APR over the same term, it drops to about $966. Your actual payment will vary based on creditworthiness and the lender's terms.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts