For small business owners looking to grow, choosing the right financing solution for a commercial vehicle fleet can mean the difference between scaling smoothly or struggling with cash flow issues. Luckily, there are plenty of financing options available to meet your specific needs — this guide breaks down the best ways to fund your business's vehicle fleet.

What Is Commercial Fleet Financing?

Commercial fleet financing refers to specialized lending products that help businesses purchase or lease multiple vehicles without significant upfront costs. This financing solution helps companies buy commercial vehicles like semi-trucks, box trucks, and delivery vans while preserving working capital. That's because rather than paying the full purchase price at once, businesses can spread the cost of an entire fleet of vehicles over time through manageable monthly payments.

How Does Commercial Vehicle Financing Work?

The commercial vehicle financing process typically goes like this:

Assess your business needs. Determine exactly what types of vehicles your operation requires and how many you need to purchase.

Choose your financing option. Decide whether a loan or lease makes more sense for your business model and cash flow situation.

Research lenders. Compare offers from multiple financing providers to find competitive rates and terms.

Prepare documentation. Gather necessary paperwork (with Clarify Capital, which means three months of your most recent bank statements, proof of at least six months in business, and verification of $10,000+ monthly revenue).

Submit your application. Complete the lender's application process, providing all required business finance information.

Review offers. Once approved, carefully examine the terms before accepting.

Finalize the agreement. Sign the paperwork and prepare for fund disbursement.

Purchase your fleet. Use the secured financing to acquire your commercial vehicles.

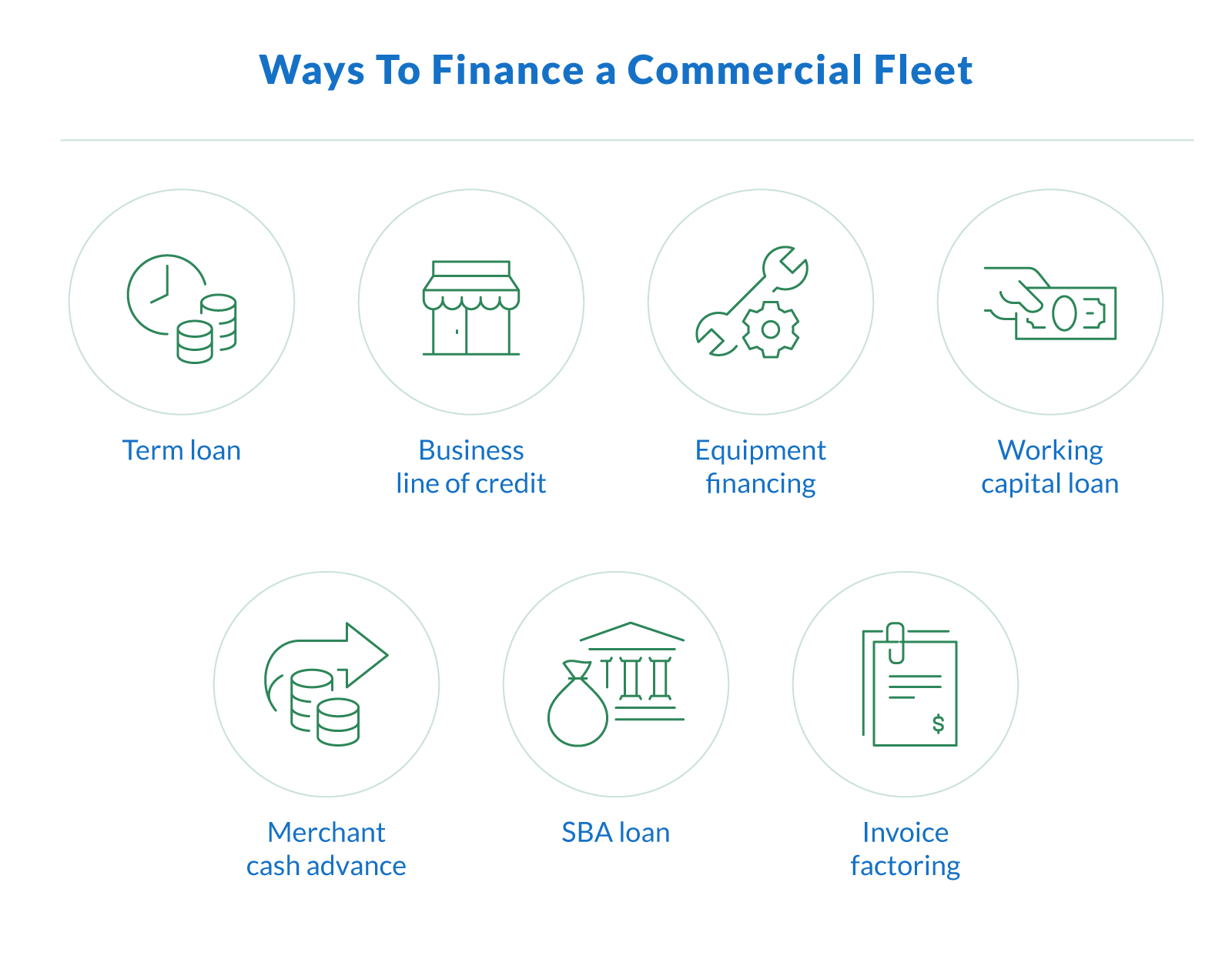

Top Commercial Fleet Financing Options

Not all business financing is created equal. The best option for your company depends on your financial situation, credit history, and specific business needs. Here's a breakdown of the top financing solutions for your commercial fleet:

Term Loan

A term loan gives you a lump sum of money upfront that you pay back with fixed monthly payments over a set period. They're straightforward and predictable, making them a popular choice for fleet financing.

Term loans offer several benefits:

Lower interest rates. Compared to other financing options, term loans typically come with more competitive rates.

Predictable payments. Fixed monthly payments make budgeting easier for your business.

Higher loan amounts. You can often secure larger sums to purchase multiple vehicles at once.

Build business credit. On-time payments help strengthen your company's credit profile.

There are some downsides to consider, though:

Strict qualification requirements. Lenders may want to see strong credit scores and established business history.

Potential collateral. Some lenders may require vehicles or other assets as security.

Less flexibility. Once your loan terms are set, you have limited options to adjust.

Long approval process. Traditional term loans can take weeks to process.

Term loans work best for established businesses with good credit that need to finance a specific, one-time fleet purchase with predictable financing terms.

Line of Credit

A business line of credit works like a credit card for your business — you get approved for a certain credit limit and can borrow any amount up to that limit whenever you need it. You only pay interest on what you actually use.

The flexibility of a line of credit offers:

Revolving access to funds. Borrow, repay, and borrow again as needed without reapplying.

Pay for what you use. Only pay interest on the amount you draw, not your entire credit limit.

Working capital on demand. Address cash flow gaps while managing fleet purchases.

Quick access to additional funds. Cover unexpected vehicle maintenance or additions to your fleet.

Possible downsides include:

Higher interest rates. The flexibility typically comes at a cost compared to term loans.

Variable payments. Your monthly payment can change based on your balance and interest rate.

Lower maximum amounts. Credit limits may be smaller than what you'd get with a term loan.

Potential for debt cycles. The revolving nature can lead to ongoing debt if not managed carefully.

Lines of credit are ideal for businesses that need flexible financing for a growing fleet or those with seasonal fluctuations in their transportation needs.

Equipment Financing

Equipment financing is specifically designed for purchasing vehicles and machinery. The equipment itself serves as collateral for the loan, which can make qualifying easier for businesses with less-than-perfect credit.

This specialized financing offers:

Self-collateralizing. The vehicles themselves secure the loan, potentially making approval easier.

Tax benefits. Section 179 deductions may allow you to write off the full purchase price.

Fixed interest rates. Many equipment loans offer stable rates for predictable budgeting.

Easier approval for startups. Even businesses with limited history or bad credit may qualify.

Consider these limitations:

Limited to equipment purchases. Can't be used for other business expenses.

Potential for obsolescence. You're committed to paying for the equipment even if it becomes outdated.

Down payment required. Most lenders require 10-20% down.

May affect business credit. These loans appear on your business credit report.

Equipment financing works well for companies of all sizes that need new vehicles but want to preserve cash flow, including startups and businesses working to rebuild their credit.

Working Capital Loan

Working capital loans provide flexible financing to cover day-to-day operating expenses, including fleet maintenance, fuel costs, and driver wages. They're designed to address short-term cash flow needs.

These short-term loans help manage operational costs while you wait for customer payments or during seasonal slowdowns. Working capital financing gives you the flexibility to cover immediate expenses without disrupting your long-term fleet investment plans.

This option is particularly good for transportation businesses with fluctuating cash flow needs or those experiencing temporary financial gaps while growing their operations.

Merchant Cash Advance

A merchant cash advance provides immediate funding based on your future credit card sales. Instead of monthly payments, you repay through a percentage of your daily credit card transactions.

This financing solution offers fast access to cash with minimal paperwork. The repayment structure adjusts automatically with your business income — you pay more when sales are strong and less during slower periods. Businesses with high credit card sales volumes and unpredictable cash flow often find this option helpful for quick fleet expansions.

SBA Loan

SBA loans are government-backed loans with some of the most competitive interest rates and longest loan terms available. Though the application process is more complex, the favorable terms make them worth considering for major fleet investments.

These loans offer lower down payments, longer repayment periods (up to 25 years in some cases), and interest rate caps that protect your business. Clarify Capital can help you navigate the complex application process, increasing your chances of approval for this desirable financing option.

Small business owners looking to make substantial, long-term investments in their commercial fleet will find SBA loans particularly valuable when they qualify.

Invoice Factoring

Invoice factoring lets you sell your unpaid invoices to a factoring company for immediate cash, typically at 80-90% of their value. The factoring company then collects payment from your customers.

This financing solution helps businesses avoid the cash flow gaps that occur while waiting for customer payments. It provides quick access to capital that can be used for fleet maintenance, fuel costs, or even new vehicle purchases without taking on traditional debt.

Invoice factoring works especially well for transportation companies with long payment cycles from clients but ongoing operational expenses to maintain their fleet.

Leasing vs. Buying Vehicles

When building your commercial fleet, one of the biggest decisions you'll face is whether to lease or buy your vehicles. Each approach has distinct financial implications for your business.

Leasing vehicles means you make regular lease payments for a fixed term without actually owning the vehicles. When your lease ends, you typically have the option to return the vehicles, upgrade to newer models, or purchase them at a predetermined price.

Buying vehicles means you own them outright — either by paying cash or financing them through loans. While the monthly payments might be higher initially, you'll eventually own valuable assets.

Leasing tends to work best for businesses that:

Want to maintain a modern fleet with the latest features and technology

Prefer lower monthly payments to conserve cash flow

Don't want to deal with selling or disposing of older vehicles

Drive predictable, limited miles each year

Want to avoid major maintenance costs

Buying is typically better for businesses that:

Plan to keep vehicles for many years

Put high mileage on their vehicles

Need to customize their vehicles extensively

Want to build business assets over time

Have the cash flow to handle higher initial costs

Advantages of Leasing

Lower monthly payments. Leasing typically requires less cash each month than loan payments for the same vehicles.

Minimal upfront costs. Leasing options often require little to no down payment to get started.

Regular fleet upgrades. You can transition to newer vehicles at the end of each lease term.

Reduced maintenance concerns. Many commercial leases include maintenance packages or cover vehicles during warranty periods.

Tax benefits. Lease payments are often fully tax-deductible as business expenses.

Disadvantages of Leasing

No ownership equity. You make payments but don't build equity in the vehicles unless you purchase them at the end of the lease.

Mileage restrictions. Most leases have limits on annual mileage with penalties for exceeding them.

Long-term cost. Over time, leasing continuously can cost more than buying and maintaining vehicles.

Less flexibility. Early termination of a lease can result in significant penalties.

End-of-lease concerns. You may face charges for excessive wear and tear when returning vehicles.

Advantages of Buying

Build equity. Each payment brings you closer to owning valuable business assets.

No mileage restrictions. You can drive the vehicles as much as needed without penalties.

Customize freely. You can modify vehicles to suit your specific business needs.

Long-term savings. Once paid off, you'll have lower operating costs and assets you can sell later.

Depreciation benefits. You can claim depreciation on your taxes to offset the vehicles' declining value.

Disadvantages of Buying

Higher initial costs. Buying typically requires larger down payments and monthly payments.

Maintenance responsibility. As vehicles age, you'll bear increasing maintenance and repair costs.

Depreciation risk. Vehicles lose value over time, sometimes faster than expected.

Capital tie-up. Purchasing vehicles requires significant capital that could be used elsewhere in your business.

Resale challenges. When it's time to upgrade, you'll need to handle selling or trading in your old vehicles.

How To Qualify for Commercial Fleet Financing

Getting approved for fleet financing depends on several key factors lenders consider when evaluating your application. Here's what you'll need to qualify:

Time in Business

Most lenders prefer to work with established businesses. Traditional lenders typically require at least two years in operation, while alternative lenders like Clarify Capital may approve businesses with as little as six months of history. Having a longer track record can lead to better financing terms.

Revenue Requirements

Your business's cash flow is a critical factor. Lenders want to see that you have the income to support loan repayments. Clarify Capital typically requires at least $10,000 in monthly revenue, though specific requirements vary by financing type and amount requested.

Credit Considerations

While personal and business credit scores both matter, they carry different weight depending on the lender:

Most lenders look for a score of 500+, with better rates available for scores over 650.

A strong business credit history can help offset a weaker personal score.

For newer businesses, personal credit often carries more weight in the approval decision

Down Payment Expectations

The down payment amount varies by financing type:

Equipment financing typically requires 10-20% down.

SBA loans may require 10-15% down.

Some alternative financing options offer zero-down solutions for qualified borrowers.

Clarify Capital works with you to find options matching your available capital, including low or no down payment solutions when possible.

Application Documentation

When applying with Clarify Capital, you'll need:

Three months of recent business bank account statements showing regular income

Proof your business has been operating for at least six months

Verification that you meet the $10,000 minimum monthly revenue requirement

The application itself takes less than two minutes to complete online. Unlike traditional lenders, Clarify Capital doesn't require complex business plans or extensive financial projections, making the application process much more straightforward.

Choosing the Best Fleet Financing for Your Business

Finding the right financing solution for your commercial fleet requires careful consideration of several factors. Here's what to evaluate when comparing your options:

Calculate the Total Cost of Ownership

Look beyond the monthly payment to understand what you'll actually pay for your business loan:

Interest rates. Even a small difference in rates can mean thousands of dollars over the life of the loan.

Hidden fees. Watch for origination fees, prepayment penalties, and administrative costs.

Term length. Longer terms mean lower payments but more interest paid overall.

Industry-Specific Considerations

Your business type matters when choosing financing:

Trucking industry operators often benefit from specialized programs designed for commercial trucks.

Construction equipment financing might offer different terms than passenger vehicle fleets.

Delivery businesses with frequent vehicle turnover may prefer leasing options.

Finance Your Commercial Fleet Today

Expanding your business fleet doesn't have to drain your capital or strain your cash flow. With the right financing option, you can grow your operation while maintaining financial flexibility.

Whether you need a single commercial vehicle or an entire fleet, today's financing landscape offers solutions for every business situation. From traditional term loans to specialized equipment financing to flexible lines of credit, you have more options than ever to fund your fleet needs.

Working with an experienced lender like Clarify Capital can simplify the process, helping you navigate the complexities of commercial vehicle financing to find terms that work for your specific business needs. Our team matches you with the most competitive offers from a network of 75+ lenders, often securing funding in as little as 24 hours after approval.

Ready to grow your business with the right vehicles and the right financing? Apply now to get started and discover your fleet financing options today.

Bryan Gerson

Co-founder, Clarify

Bryan has personally arranged over $900 million in funding for businesses across trucking, restaurants, retail, construction, and healthcare. Since graduating from the University of Arizona in 2011, Bryan has spent his entire career in alternative finance, helping business owners secure capital when traditional banks turn them away. He specializes in bad credit funding, no doc lending, invoice factoring, and working capital solutions. More about the Clarify team →

Related Posts