Small Business Financing

Denied a Business Loan? 7 Steps To Get Back on Track

A denial isn't the end of the road. Here's exactly what to do next to strengthen your application and find the right funding.

Read Your Denial Letter

Get the specific reasons behind the decision and understand your legal rights.

Check Your Credit Report

Request a free report within 60 days and dispute any errors you find.

Lower Your Debt-to-Income Ratio

Pay down revolving balances and reduce credit utilization below 30%.

Strengthen Your Financials

Organize tax returns, P&L statements, and bank statements showing steady cash flow.

Ask for Reconsideration

Contact your loan officer with additional documentation or corrected credit data.

Explore Alternative Financing

Clarify Capital matches you with 75+ lenders to find options that fit your situation, even with bad credit.

Reapply With a Stronger Application

Use prequalification tools and try a different lender type for better approval odds.

A loan denial is a lender's decision to reject a financing application, and if you just received one, you're not alone. Nearly 24% of small business financing applicants received none of the funding they sought in 2024, and the share of borrowers who were fully approved remains below prepandemic levels.

A denial can feel like a dead end, but it's actually a starting point.

Your denial letter contains specific information about what went wrong. Once you understand the reasons, you can take concrete steps to fix the issues, protect your credit score, and find the right lender for your business.

Here, I'll walk you through why business loans get denied, what your rights are, and how to move forward.

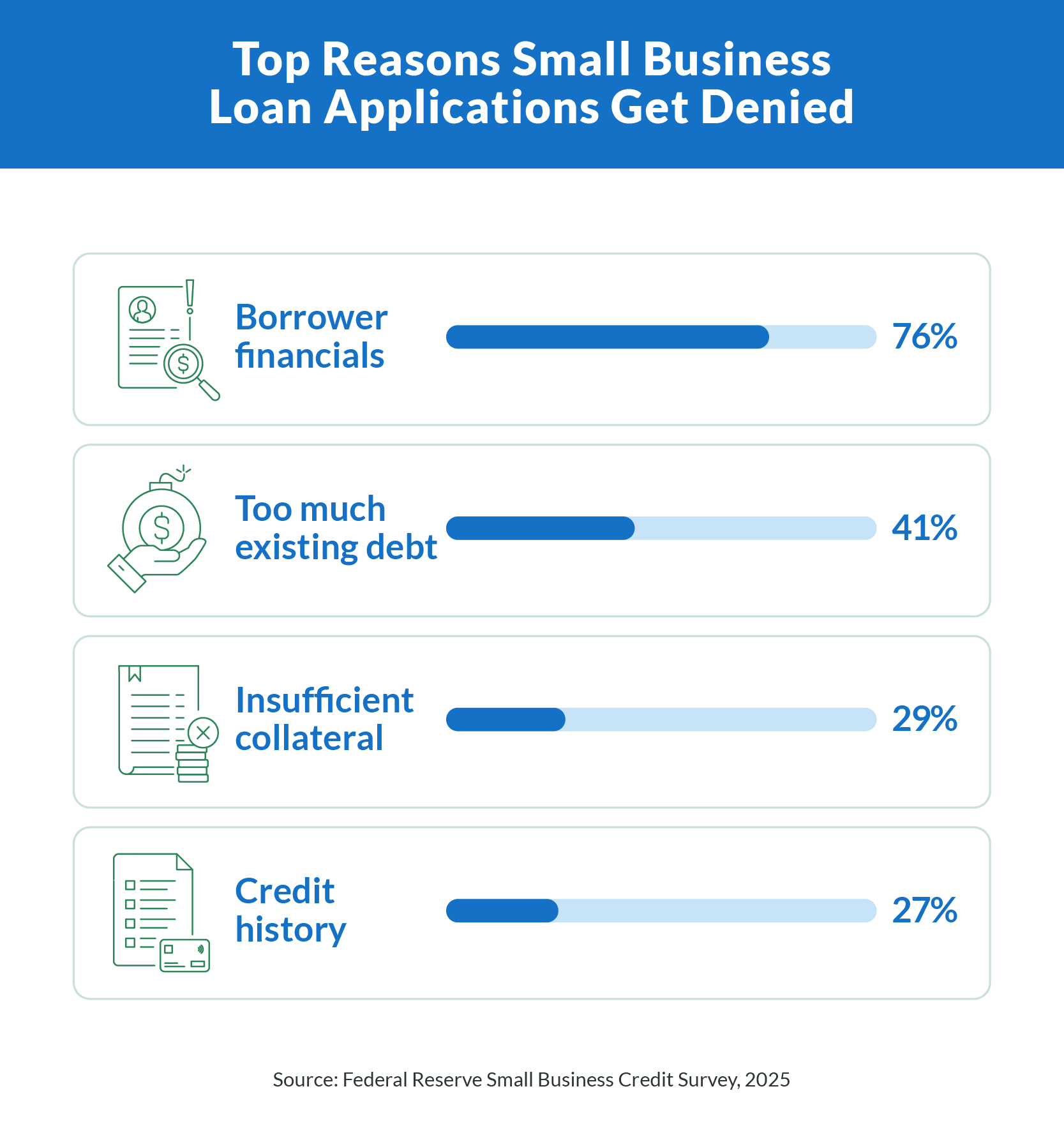

Why Business Loans Get Denied

Denial reasons vary by lender type and loan product, but most fall into a handful of common categories. The fastest-growing factor is too much existing debt, which jumped from 22% to 41% between 2021 and 2024 as a borrower-reported reason for denial. Here's what lenders are flagging most often.

Too Much Existing Debt

A high debt-to-income ratio (DTI) tells lenders you may struggle to take on additional monthly payments. In 2024, 41% of denied small business applicants pointed to too much existing debt as a factor in their denial. That’s nearly double the 22% rate from 2021.

A DTI below 36% is generally considered ideal for business loan approval, while anything above 43% makes approval significantly harder. Lenders also look at your debt service coverage ratio (DSCR), which measures whether your business generates enough income to cover its existing debt payments plus the proposed new loan.

Low Credit Score or Thin Credit History

Lenders evaluate your personal credit score (and sometimes your business credit score) when reviewing a loan application. The Federal Reserve's 2025 Small Business Credit Survey found that low credit scores linked to credit history contributed to 27% of loan denials. Most traditional business lenders look for a personal FICO score of 680 or higher, though the credit score needed for a business loan depends on the loan type and lender. A thin credit history (few accounts, short account age) can be just as problematic as a low score because it gives lenders less data to assess your creditworthiness.

Insufficient Revenue or Short Business History

Lenders want to see steady revenue and a track record of operations (often two or more years). Startups and newer businesses face steeper odds because lenders have less data to assess risk. If your monthly income fluctuates significantly or your business hasn't turned a consistent profit, some lenders may not move forward regardless of your credit score.

Weak Collateral or Incomplete Documentation

Insufficient collateral was cited in 29% of business loan denials. Lenders may require assets like equipment, property, or inventory to secure the loan, and if your business doesn't have enough to back the loan amount, that's a red flag. Missing or disorganized documentation (tax returns, financial statements, a business plan) can also trigger a denial. Understanding your lender's small business loan requirements before you apply helps you avoid this.

For a deeper look at how collateral works in business lending, see our guide to secured business loans.

What Your Denial Letter Should Tell You

Federal law requires lenders to send an adverse action notice within 30 days of a completed loan application when they deny it. This isn't just a form letter: it contains specific disclosures you're legally entitled to. Your notice must include:

Statement of the action taken. A clear acknowledgment that your application was denied (or that a counteroffer was made).

Principal reason(s) for the denial. The lender must provide the specific factors behind the decision, or a statement that you can request those reasons within 60 days.

Lender's name and address. Contact information so you can follow up with questions.

ECOA rights statement. A notice that the Equal Credit Opportunity Act prohibits lending discrimination.

Administering federal agency. The name and address of the agency that oversees the lender's compliance.

The Consumer Financial Protection Circular (CFPB) has clarified that generic reasons like "internal lending standards" are not specific enough, even when AI or algorithms are involved in the lending decision. If your denial letter doesn't include specific reasons, you have the right to request them in writing.

How To Fix the Issues Behind Your Denial

The denial letter gives you a roadmap. Each reason it lists is something you can address before reapplying, and most fixes take a few months rather than years. Here's where to start.

Check Your Credit Report for Errors

After a denial, you're entitled to a free copy of your credit report within 60 days of the adverse action notice. The denial letter will identify which credit bureau (Experian, Equifax, or TransUnion) the lender used, and you can request your report directly from that bureau at no cost. AnnualCreditReport.com also provides free weekly reports from all three bureaus.

Review the report for credit report red flags like incorrect balances, accounts that don't belong to you, or outdated negative items. If you find errors, dispute them directly with the bureau. Correcting inaccuracies can improve your credit score and your approval odds on a future application. Keep in mind that nearly 40% of Americans carry a credit utilization rate above 30%, so even small balance errors can make a difference.

Lower Your Debt-to-Income Ratio

Reducing existing debt payments is one of the most effective ways to improve your DTI before reapplying. Pay down revolving balances first (especially credit card debt), avoid taking on new debt, and look into business debt consolidation loans to simplify high-interest payments.

Credit utilization (how much of your available credit you're using) accounts for about 30% of a FICO Score, and people with the highest scores typically keep utilization below 10%. Paying down a credit card from 50% utilization to under 30% can produce a noticeable credit profile improvement within a single billing cycle. The goal is to show lenders that your business and personal finances can handle additional debt payments comfortably.

Strengthen Your Business Financials

Lenders want to see organized, up-to-date documentation that tells a clear financial story. Before reapplying, gather at least two years of business tax returns, a current profit-and-loss statement, and three to six months of bank statements showing steady cash flow. If your revenue has been inconsistent, wait until you have a few months of stronger numbers to include.

A solid business plan also strengthens your application, especially if you're a newer business. It shows lenders you have a clear strategy for generating the revenue needed to repay the loan. Clarify Capital offers free business plan templates that can help you build one quickly.

Can a Loan Denial Be Reversed?

There's no formal reversal process, but many lenders (especially community banks and credit unions) have internal reconsideration channels. Reaching out to your loan officer and asking the right questions can sometimes change the outcome. Here's how to approach it:

Call the lender and ask exactly which factors led to the denial. The adverse action notice may be broad, but a conversation can reveal more detail.

Ask whether additional documentation (stronger financials, a cosigner, or a larger down payment) could change the decision.

If the denial was based on incorrect credit data, provide evidence of the correction and request reconsideration.

Request a written explanation if the notice you received wasn't specific enough.

It's worth noting that approval rates vary significantly by lender type. Small banks fully approve 54% of applications, compared to 45% at large banks and 30% at online lenders, according to the Federal Reserve. If a large bank denied you, a community bank or credit union may be worth trying next. And if you've already been turned down by a traditional lender, it may be possible to get a business loan with bad credit through an alternative lender with more flexible qualification criteria.

Does a Loan Denial Hurt Your Credit?

The denial itself doesn't appear on your credit report, but the hard inquiry from the application does. A single hard inquiry typically costs fewer than five points on a FICO Score, and inquiries only influence scoring for about 12 months (even though they remain on your report for two years). Credit inquiries account for just 10% of what makes up a FICO Score, so one denial won't cause major damage.

If you're planning to apply with multiple lenders, be aware of the rate-shopping window. Newer FICO models treat multiple loan applications within a 45-day window as a single inquiry for mortgage, auto, and student loans, though this deduplication doesn't apply to all business loan types. Spacing out applications or using prequalification (which requires only a soft pull) can help you check eligibility without adding hard inquiries to your report. Prequalification gives you a preliminary read on your approval odds before you commit to a formal application.

Alternative Financing Options After a Denial

A denial from one lender doesn't mean every door is closed. Different lenders and loan products have different eligibility requirements, and some are specifically designed for borrowers who don't meet traditional bank criteria.

| Business Financing Options at a Glance | ||||

|---|---|---|---|---|

| Product | Funding speed | Loan amount | Cost | Repayment term |

| Business line of credit | 24 to 48 hrs | Up to $5M | 6% to 14% APR | Six to 36 months (revolving) |

| Invoice factoring | 24 hrs | 70% to 100% of invoice | 0.5% to 3% per 30 days | 30 to 120 days |

| Merchant cash advance | 24 hrs | Up to $5M | 1.08 to 1.45 factor rate | Six to 24 months |

| Equipment financing | One to two days | 100% equipment value | 4% to 45% APR | 24 to 72 months |

| SBA microloan | Varies | Up to $50,000 | 8% to 13% | Up to seven years |

SBA Microloans

SBA microloans provide up to $50,000 (the average is about $13,000) through nonprofit, community-based intermediaries. Interest rates typically range from 8% to 13%, with repayment terms of up to seven years. Microloans are designed for startups and small businesses that may not qualify for traditional bank loans, and the application process tends to focus more on the borrower's character and business plan than on credit score alone. Funds can be used for working capital, inventory, supplies, and equipment, but not to pay existing debts or purchase real estate.

For borrowers who can't qualify for an SBA loan at all, there are several SBA loan alternatives worth considering.

Community Development Financial Institutions (CDFIs)

CDFIs are mission-driven lenders that serve underserved communities with more flexible underwriting standards. There are over 1,400 certified CDFIs in the U.S., and they include banks, credit unions, and loan funds. CDFIs often consider the full picture of a borrower's financial situation rather than relying solely on credit score cutoffs, which makes them a strong option for business owners who were denied due to a thin credit profile or short business history.

Business Lines of Credit, Invoice Factoring, and Merchant Cash Advances

For business owners who need flexible or fast funding, these products offer different structures than traditional term loans:

Business line of credit. Borrow up to $5M as needed, with APRs from 6% to 14% and revolving terms of six to 36 months. Funding typically arrives within 24 to 48 hours. Unlike a personal loan, a line of credit lets you draw and repay repeatedly without reapplying. For a comparison of how these stack up against other products, see business line of credit vs. business loan.

Invoice factoring. Receive 70% to 100% of your outstanding invoice value, with fees of 0.5% to 3% per 30 days and funding within 24 hours. This option works well for B2B businesses with unpaid invoices. The lender evaluates your customers' creditworthiness, not yours.

Merchant cash advance. Access up to $5M with factor rates of 1.08 to 1.45 and flexible repayment tied to daily sales. Funding arrives within 24 hours. MCAs don't require collateral or a strong credit score, making them accessible to borrowers who've been denied elsewhere.

Know Your Rights as a Borrower

While this article isn't a substitute for legal advice, federal laws protect borrowers during the loan application process and after a denial. Knowing these protections can help you hold lenders accountable and make sure you're being treated fairly.

The Equal Credit Opportunity Act (ECOA)

ECOA prohibits lenders from discriminating based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Warning signs of discrimination include being treated differently in person than on the phone, being steered toward less favorable products, or being offered higher interest rates despite meeting stated qualifications. If you suspect discrimination played a role in your denial, you can file a complaint with the CFPB at consumerfinance.gov/complaint or by calling (855) 411-2372.

The Fair Credit Reporting Act (FCRA)

Under the FCRA, when a lender denies your application based on information in your credit report, they must tell you which credit bureau provided the data. You then have 60 days to request a free credit report from that bureau. If credit scores were used in the decision, the lender must share the score and the key factors that negatively affected it. These disclosures give you a clear picture of what to fix before your next application.

When (and How) To Reapply for a Business Loan

You can apply for a new loan immediately after a denial, but reapplying without addressing the underlying issues will likely result in the same outcome (and another hard inquiry on your credit report). Take these steps before submitting a new application:

Address issues that caused the denial. These should be cited in your adverse action notice (credit score improvements, debt paydown, stronger documentation).

Check your credit report. Confirm that corrections and paydowns have been reported to the credit bureaus.

Consider applying with a different lender type. Full approval rates are 54% at small banks, 45% at large banks, and 30% at online lenders. Note: Online lenders often accept lower credit scores, require less documentation, and fund faster than traditional banks.

Use prequalification tools. Do a soft pull (it won't affect your credit score) to check eligibility before submitting a formal application. This step is built into your application process when you apply through Clarify Capital.

Prepare a complete application package. Depending on the loan requirements, you may need two years of tax returns, current financial statements, a business plan, and any collateral documentation.

For a step-by-step walkthrough, see our guide on how to apply for a business loan.

Your Next Funding Opportunity Starts Here

A loan denial doesn't have to define your business's future. The information in your adverse action notice, combined with the steps outlined above, gives you a clear path toward a stronger application and better financing options. When you're ready to move forward, apply with Clarify Capital to see what you qualify for, with funding available in as little as 24 hours.

Frequently Asked Questions About Loan Denial

What is a loan denial?

A loan denial is a lender's decision to reject a financing application based on factors like creditworthiness, business financials, or documentation issues. Lenders are legally required to provide an adverse action notice within 30 days explaining the specific reasons for the denial.

Can a loan denial be reversed?

There's no formal reversal process, but applicants can contact the loan officer to discuss the denial, provide additional documentation, or ask for reconsideration. Adding a cosigner or correcting inaccurate credit data may also change the outcome.

Is it bad to be denied a loan?

The denial itself doesn't appear on your credit report. The hard inquiry from the application does, but a single inquiry typically costs fewer than five points and only affects scoring for about 12 months. It's not ideal, but it's far from catastrophic.

Can you apply for a loan after being denied?

Yes. There's no mandatory waiting period, but reapplying immediately without fixing the underlying issues will likely result in another denial. Address the reasons listed in your adverse action notice first, then consider applying with a different lender or loan type to improve your approval odds.

Michael Baynes

Co-founder, Clarify

Michael has over 15 years of experience in the business finance industry working directly with entrepreneurs. He co-founded Clarify Capital with the mission to cut through the noise in the finance industry by providing fast funding and clear answers. He holds dual degrees in Accounting and Finance from the Kelley School of Business at Indiana University. More about the Clarify team →

Related Posts